Hello,

I have been an avid follower of ValuePickr forum and it has helped me shape my investing decisions. I have a 6 months - 2 years view on all these stocks, which can be further increased based upon performance.

I have basic finance background, have done a fundamental analysis course from BSE(which was actually helpful with loads of practical knowledge). Have bookmarked the investing books from valuepickr article on investing books and will be starting them soon. Also pursuing CFA Level 1. I am currently working with an experienced investor who has taken me under his wing to mentor and I am trying to learn and grasp as much as possible from him and would love to be mentored by fellow experienced investors. Have been an active investor only for the past 7 months.

Now, coming to the stocks, my main lookout is for triggers such as expansion(especially massive capex already done in last FY or getting done in next 1-2 quarters), import substitutes, demand-supply mismatch(such as current container shortage). I am looking for growth in bottomline and topline within 1 year. Also, I like stocks with low free float, which gives scope for colossal returns, when management has skin and competence. Also, I like to check P/E(alongwith industry P/E), P/B, OPM, ROCE, ROE, D/E, Earnings yield and few other metrics before deciding to dig deeper into ARs.

Coming to my picks(Heavy allocation) :

1) Pokarna - Massive Quartz expansion taking place in December 2020. Best in quality(based on scuttlebutt) and No 1 in terms of value as well. Home interiors will get a boost even after covid and with high ADD on Chinese products + reduced ADD on Pokarna are a plus. Waiting for a small correction to enter big. Preferably @140 levels. Expecting a 2x return in 2 years.

2) Lancer Container - Shortage of containers in India. Lancer having very low free float was a juicy call @60 considering there was no great upmove or downmove for a long time. With vaccines coming into play + Make in India leading to improved exports and decent metrics, decided to take the plunge. I feel container demand will be on the higher side over at least next 2 quarters if not more.

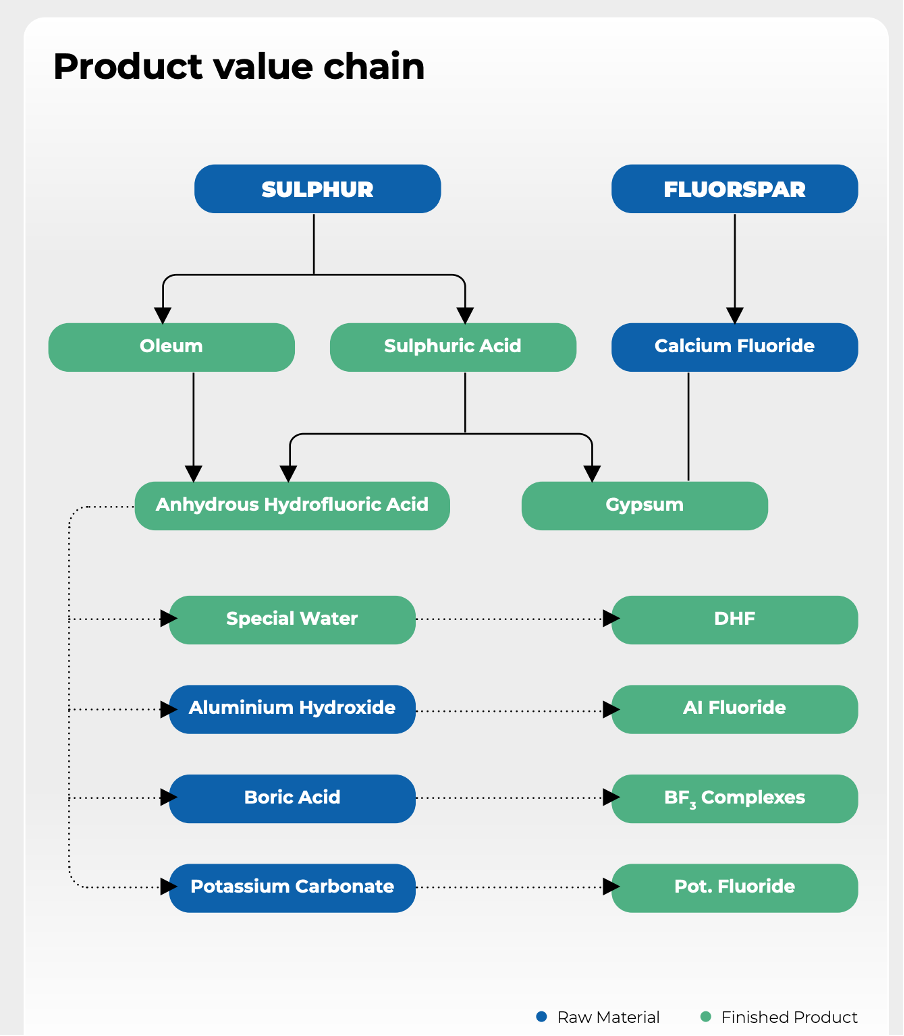

3) Alufluoride - Needed for aluminium smelting. Massive capex done and moved into new factory in December. Entered with half of desired allocation as Q3 nos will be pathetic(old factory was shut in order to transition to the new factory). Entered @175

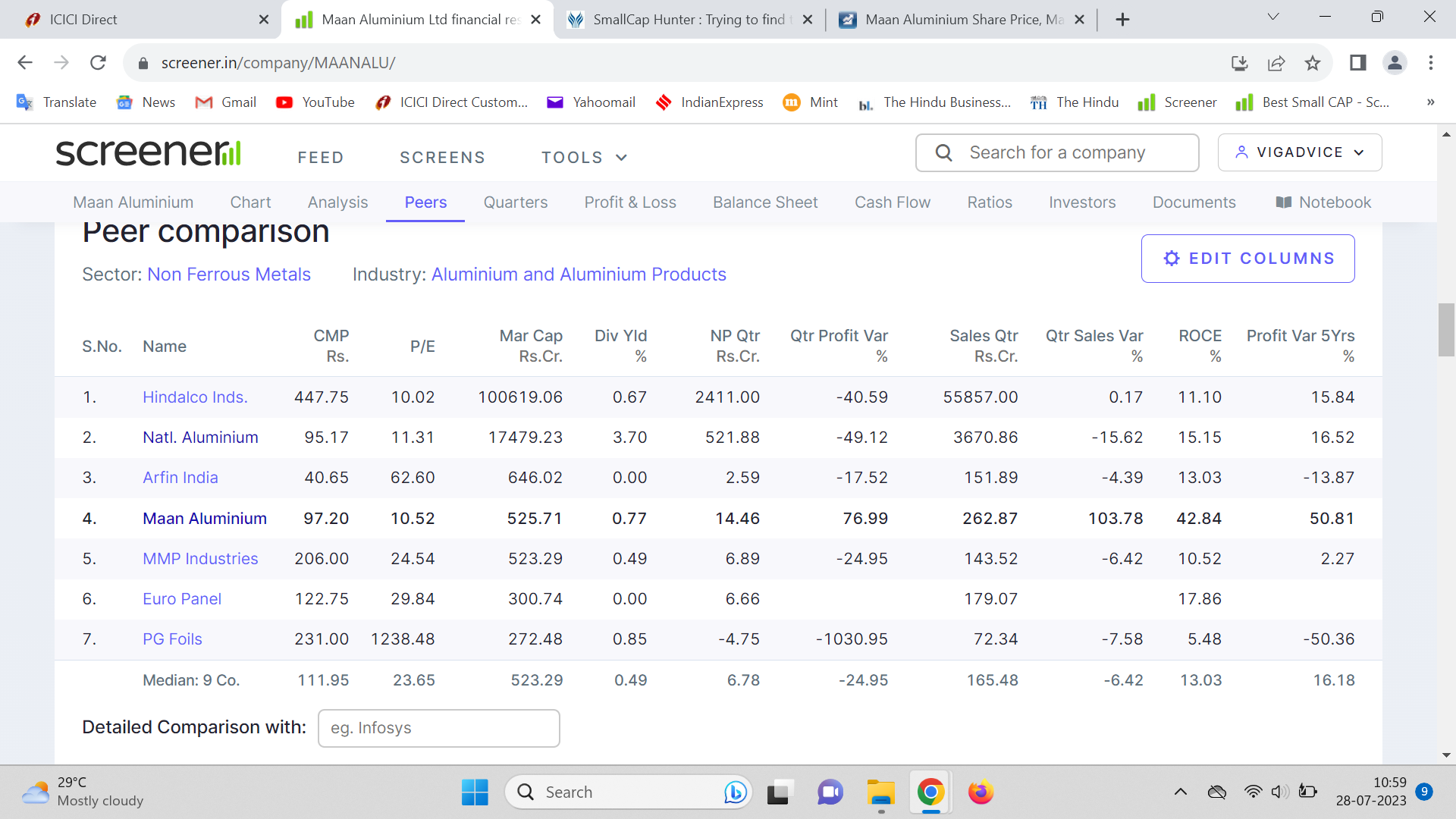

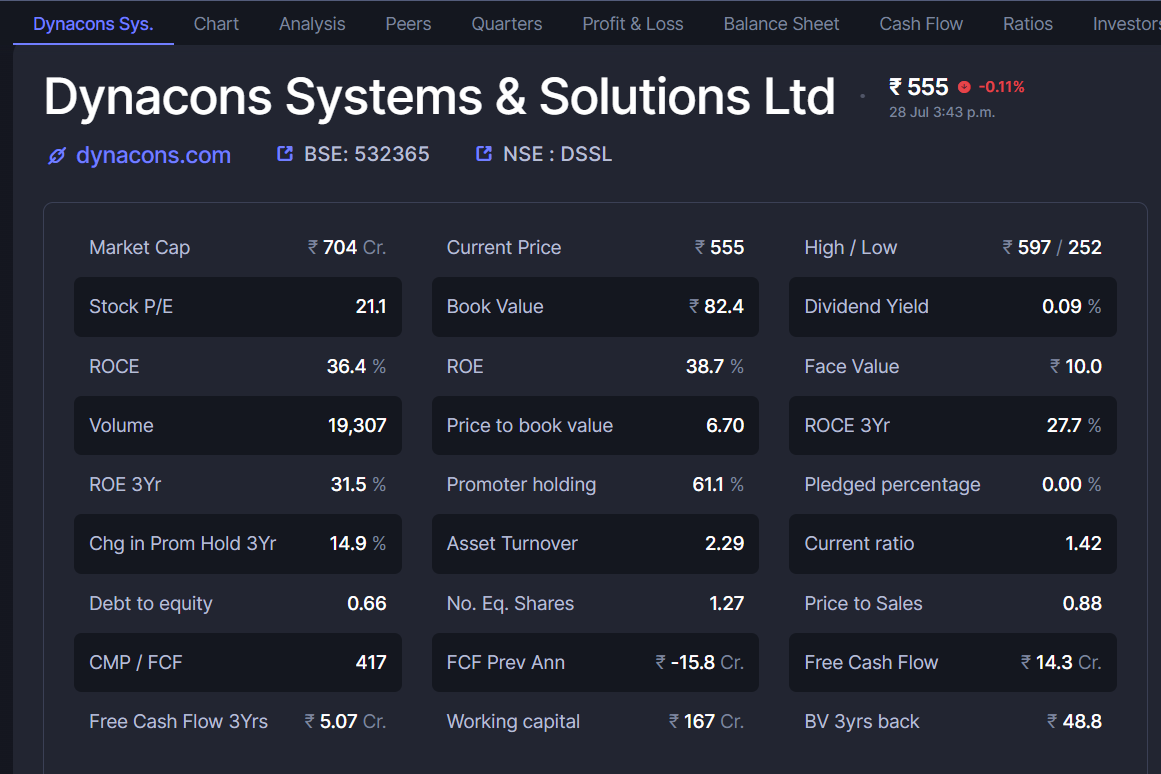

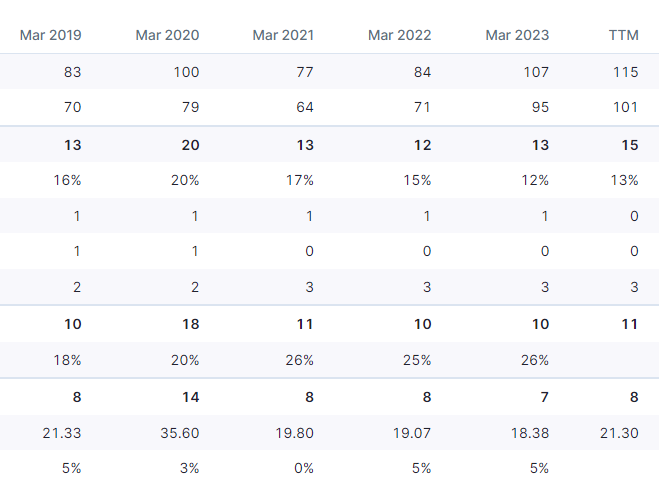

4) MMP Industries -

FUTURE PLANS / PROSPECTS:-

"(A) ATOMISED AND PYRO & FLAKE POWDERS

After the start of operations in end of April 2020. Unit I (Bhandara) reached full capacity utilization during the month of May 2020 and is expected to operate at full capacity for the rest of the year.

Commercial operations of the Umred powder plant facility began in October’2019. Due to prevailing COVID-19 situation Unit II (Umred) was temporarily shut down in March 2020.

Looking at the present market condition and positive signs of demand pickup, Company estimates that the Unit II may restart its operation by the beginning of August, 2020 (subject to COV1D issue not further deteriorating). We expect that this capacity will also be fully utilized by Q-4 of FY 2020-21.

(B) ALUMINIUM FOILS

The Aluminium Foil project is at an advance stage of implementation inspite of the difficulties of the current adverse situation. Your Company expects to begin production of both bare foil and converted foil during Q-4 FY 2020-21 or earlier. In view of many audits and approvals before bulk supplies can begin, your Company will utilize a small % of capacity during FY 2020-21 and 50-60% during FY 2021-22. This can be scaled-up faster, subject to pharma customers speeding up approvals keeping in view the very buoyant market conditions prevailing today (Chinese and ASEAN region imports are reducing).

© ALUMINIUM CONDUCTORS

As reported last year, Aerial Bunched Cables (ABC) project is nearing completion. The Company envisages a moderate continuing growth in the aluminium conductor and cable sector. Trial production is expected to commence during August-September 2020. This will enable improved capacity utilisation, enhance value addition and diversify the product portfolio."

Self explanatory excerpt from AR which was the investment rationale + the fact of having it below it’s Feb 2020 prices and not overvalued even at current prices.

Entered @90

5) Kanchi Karpooram - Capex completing in December 2020 which will increase capacity substantially leading to improved topline and bottomline over a 1-2 year period. Camphor is currently in demand and I expect it to remain so in the medium term. Entered @425

6) Kitex Garments - No 1 from India for kidswear export. Decent capex done and ongoing. New textile policy is one of the triggers for the same, along with opening of economy. Entered @122

7) Vardhman Acrylics - New textile policy play which will likely favour Man Made Fibre oriented companies. Vardhman seems to be decently valued in it’s pack and again with low free float presents an opportunity for massive jumps in prices. Entered @34

8) Apex Frozen Foods - Huge Capex completed in FY20, wherein they moved to a new facility from their leased facility, They have also entered the ready to eat market which is expected to grow hereon. Again waiting to enter more below 300 for a 2 year period. Entered @270

Most of these stocks have low P/E and seem fairly valued. Considering how the market has run up, it is becoming tough to find quality companies at decent valuations.

Currently tracking(Zero/Tracking positions in some) :

- Sirca Paints

- Varroc

- Vikram Thermo

- Transpek

- Electrosteel Casting

- Safari Ind

- Shivalik Rasayan

- Ice Make Refrigeration

- Mangalam Organics

- HBL Power

- Greaves Cotton

- HFCL

- OCCL

- Rajratan Global

- Phillips Carbon

- Shree Pushkar

- Maithan Alloys

- Genus Power

- Amines & Plasticizers

- Hikal

- Mayur Uniquoters

- Gujarat Fluorochemicals

- Sarla Performance

- Borosil

Low confidence due to lack to data(or management quality) but mouth watering valuations/triggers

- Chemfab Alkalis

- Rama Phosphates

- TGV Sraac

- Sandur Manganese

- BCL Industries

I will provide rationale for each stock in coming days. I have given a basic viewpoint as to what I look for while investing. Many companies have detailed explanations on ValuePickr itself, but would be more than happy to provide more information, wherever possible. Looking forward to constructive feedback and/or more info on the companies mentioned above from esteemed members of this amazing portal.

Disclaimer : Not a SEBI Registered Investment Advisor. These are not buy or sell recommendations.

.

.

")