Techknowgreen Solutions (TSL) is an environmental consulting company with 20+ years of experience headquartered in Pune, India. Key offerings are:

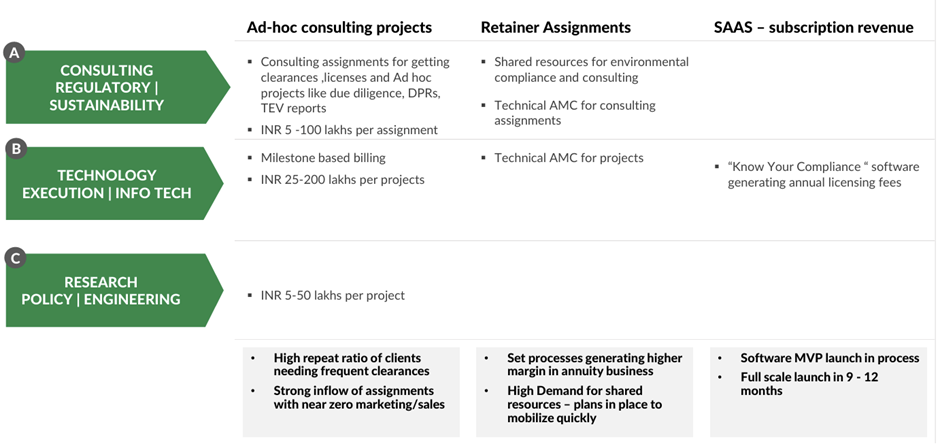

Consulting (Regulatory/Sustainability) – 65% of FY23 revenues

Environment Impact assessment: 5 sectors NABET approval. Life cycle assessment, carbon neutrality, ECBC (Energy conservation Building Code), traffic study, Hydrology study, Post Environmental Clearance, Central Control room

ESG and climate change: Includes sustainability reporting, climatology

Environmental compliance: Consent, Petroleum and Explosives Safety Organization, Fire factory, Central Ground Water Authority, EPR, Hazardous and Biomedical Waste

Environmental Due Diligence: Includes different phases Site assessment, Chemical Analysis and Remediation

DPR and designing includes STP, ETP, WTP, SWM, remediation, Air pollution control (Urban), HWM, EPR, renewables

Training and sensitization

Environmental crime investigation

Technology (execution/Infotech): 35% of FY23 revenues

Wastewater: STP, ETP, Zero liquid discharge (ZLD)

Air: Deveoped products such as YUKa yantra for Indoor air and virtual chimney for ambient air purification

Solid waste: Biogas, organic composter

Remediation: Soil, contamination, hazardous waste

Software: Developed Know your compliance app, Intellignet decision support system

Applications: Developed ROCO footprint app, e-catalyst and mass plantation apps for Maharashtra Pollution control board

IoT: Data communication interface for applications and software

Research (Policy/Engineering):

Climate change: Carbon capture, storage and utilization (CCVS), modelling Blue carbon, carbon sink, carbon and methane – neutrality and climate resilience

TSL is in business which has lot of sectorial tailwinds due to emerging environmental challenges – climate change, pollution, etc. In India alone environmental consulting addressable market is 1.2 Bn $ and environmental technology market is 6.7 Bn $. Additionally, environmental technology market for GCC countries if 5.9 bn $.

TSL has strong parentage of 20+ years in environmental consulting. Due to this, they have great existing customer relationships and execution capabilities. They have gained ‘first mover’ advantage in lot of environmental areas due to their promoters educational backgrounds (PhD) and subsequent work ex.

Being a consulting business, human resources are critical. TSL has 70+ employees as on date and significant amount of those are working for TSL for more than 10 years. Also, there are lot of past employees who are keen to come back which indicates employee friendly operations (reviews on various online platforms also paint the same).

TSL has growth strategy focused on:

big ticket projects through cross selling, bidding for large projects, newer opportunities like data centers

Upgrade to state of the art R&D through resource addition and infra addition, tie-ups with major IITs and internationally acclaimed universities, empanelments of environmental professors and experts on board

Focus on annuity business through new annuity offerings, strengthen ESG division, Shared resource model, launch of environmental apps.

Geographical expansion in GCC and US

TSL’s KMP’s salaries are significantly lower; a rarity in microcap space. Also, there are insignificant related party transactions. Board as well as various committees have right representations.

Business is asset light which is visible in terms of various metrics – OM, ROE, ROCE, etc.

TSL has paid all its outstanding debts through IPO proceeds

Inspite of being microcap there are hardly any negatives through online searches – frauds, missed project completions, etc.

MD, Dr. Ajay Ojha, is very visible speaker at various conferences, conducting awareness sessions, awards. Seems a respected technocrat.

TSL is focusing on customers who are cost conscious as that reduces competition. Also, govt. business is 50% as that reduces receivables risks.

Risks/Future steps to track:

Competition in various areas are Big 4 consulting firms (specifically in ESG) who have muscle to win business. However, TSL’s offerings are more extensive. IITs also operate as a competition.

Lot of business is with govt. (50%) and semi govt entities. Receivables need to be tracked closely.

Plan to invest in R&D, people, infra, etc. Should not be through equity dilution.

Need lot of certifications to operate. These prerequisites need to be managed well.

Significant opportunity for scale up in India and abroad; partnerships they strike needs to be monitored for the same

IPs in these businesses can be a gamechanger. For now it has 2 approved patents. Keep tab on new patent additions.

Annuity business can be great for this business. Keep tab on annuity as well as consulting business share which are high margin businesses.

Since TSL is recent IPO, there is not much in terms of financial analysis as well as forensics possible.

For now CFO is more of a technocrat and auditor is not a very well known name. Need to keep tab on any changes of the same which would be good.

Disclosure: Invested. Please do your own due diligence

Hey!

That’s an excellent thread. Though you have covered most of the points in it, I have some questions.

Is the company also involved in end to end Valuation and Trading services of Carbon and Plastic Credits along with consultancy for Net Zero?

As 50% of receivables is from Govt, though it reduces default risk, can you tell is what is the Cash conversion cycle, as in case of most companies supplying to Govt the period is >270 days.

You can also check out another unlisted competitor CREDUCE which is based out of Ahemdabad for this.

Hey great to see someone put-up a post on this. The earlier post had been locked by the moderator. I am tracking this one and did not see these numbers for the 3 verticals posted anywhere. Great work.

Here are my views on this one:

1 - Our company is related to Environment and sustainability activity - Awesome space to be in today and in future - my #1 reason for investment in this sector.

2 - Our Management looks sound, genuine and genius - my #2 to be interested in this company.

3 - Currently TSL is a microcap - So there is huge potential from here on based on just the size of company - my #3 reason to track and invest now.

4 - Looks like they have Mutiple triggers- scalability may not be an issue - my #4 reason to stay invested longer.

5 - - Looks like this one is still not “discovered” - my #5 reason for the interest.

6 - I feel their knowledge is their biggest MOAT. - my #6 reason for staying put.

Please do note that i am not an avid investor and my views could be biased because i have taken a position on this. and i do not really understand financial numbers and jargons.

Recent i had attended TSL investor meet (1st ever of my life ) so dont know if i can give any significant heads up but here is what i could gather most out of the meeting other than the positives listed above (of course the positives got cemented after the investor meet)

1 - The management is open to discussions and questions.

2 - The company is knowledge oriented and is focused to build on that.

3 - Though they said they have a big vision - they did not mention the size and mentioned that there may be some news coming pretty soon on some of the developments.

4 - They are coming up with a saas product which may become a game changer in the business of Enironmental clearances. they spoke of about 40k industries (orange and red category) in Maharashtra which could be potential targets for this product.

5 - Air cleaning gadget at urban level - this also could be a game changer if adapted by the government. (you can see some of them in chembur mumbai)

6 - They are tapping UAE market and have already achieved some success in implementing few things.

7 - They seem to be flooded with work and are actually being picky in selecting clients!

Some concerns:

1 - The management seemed to be taking their own time to scale up, as if they dont want to scale up fast and want things to be more organic, so its possible we may not get flashy numbers or worst a much slower pace of growth - which could mean holding gold for a longer period to get good returns and the equqity market may not value it richly.

2 - It a microcap so the associated risk.

3 - For a small time investor like me who mostly invest only in the likes of tcs and sbi - a company having a minimum lot size of 800 is definitely a concern as i am unable to build positions sequentially.

4 - They still have to prove their scalability and market penetration.

5 - They have to depend on people/ human resource for their implementation - i think this is the biggest concern - can they scale up and keep up the knowledge human resource or do they end up being sole proprietors of growth visibility?

My question you Santosh or someone in the forum is - Can you decipher the financial numbers in simple language for me? Because though i do understand the story and vision but not the mathematical derivation of this and probably that’s why i may be underinvested for now.

To answer your 2nd point - as per management government are excellent pay masters, in-fact if they have to be concerned it would be pvt companies paying on time. This is the primary reason they shifted their module from taking up epc kind of contracts to exclusively knowledge-based consultations. This was a question in investor meet.

The company is right now not in carbon credit trading. However, they have plans of. For now in consulting they take projects wherein a data centre or real estate or something similar is being planned. They undertake study of the same to ensure that they secure environment clearance and other compliances needed to deliver these projects. Also, assignments are undertaken for reducing carbon emissions or Zero Discharge from such setups. Other types of consulting assignment are more of annuity nature where a company (say a chemical factory or hotel, etc.) want to stay compliant wherein TSL governs it for the same and provides improvement roadmaps.

Any need for implementation from above type of consulting assignments would be a project under their Technology division.

Their research is basically to support both Consulting and Technology projects.

Till date they never had receivables writeoffs. There are couple of ligitations ongoing for receivables. However, they have recovered all their receivables in the past. Also, these being small ticket items there is not much delay from government. However, when they scale up to big ticket projects specifically in Technology segment where they do carry some inventory too, there might be risks of receivables in the future. Due to this company wants consulting to be a large part of their revenues; it is 65% already. Also, as they diversify to GCC and US, it would further mitigate these local government related risks.

Disclosure: Invested. Please do your own due diligence.

As mentioned in my writeup, we will need to wait for FY24 annual report to decipher the numbers in detail. Also, in microcap numbers might not make much sense as they would be investing for future for eg., you would see significant build-up in their fixed assets in FY24 which are towards computers, office space, etc. At this stage of micrcap you need to check on Management quality. If that is comfortable for you, you can invest and monitor their strategy and execution.

Disclosure: Invested. Please do your own due diligence.

I did attend the roadshow, There was no presentation but was in Q&A format where the host was asking questions (not sure where those questions came from as I joined bit late) and CEO and CFO were answering those questions. I did not take any notes but they were sounding very positive about the potential of the company. But since it is knowledge based work, their expansion would be function of how quickly they hire right people. Lots of questions about when they can reach 100 Cr revenue

on result declaration of March 2024, the stock crashed 20% because in Red heiring prospect company mentioned certain profit for FY 2023 , but in result of March 2024 they mentioned last year’s profit half of the declared in Red heiring prospect to show investor that company growing with high speed. Thus promoter is liar