Himachal Futuristic Communication

BSE: 500183 | NSE: HFCL | ISIN: INE548A01028 |

CMP- 26

Market Cap- 3272

Debt – 493.97

HFCL is ranked 3rd in this year’s BW Businessworld’s Fastest Growing Companies in the Rs 1,000 crore-4,999 crore (revenue) category.

Introduction

HFCL one of the largest Telecom equipment suppliers of Transmission equipment, Terminal equipment, Access equipment and Fibre Optic Cable in India. The company is also providing Turnkey services to various operators and large multinationals operating in the country. Their manufacturing facilities are located at Solan in Himachal Pradesh, Salcete in Goa and New Delhi.

Himachal Futuristic Communications Ltd was incorporated on May 11, 1987. The company started with manufacturing transmission Equipment and soon they expanded their product portfolio to manufacture Access Equipment, Optical Fibre Cable, Accessories and Terminal Equipment. The company is geared up for meeting the new generation access network demand in future.

The company was incorporated in the State of Himachal Pradesh and was promoted by Deepak Malhotra, Mahendra Nahata and Vinay Maloo. The company entered into a technical collaboration agreement with Seiscor Technologies Inc, USA, for the manufacture of 1+1 and 1+7 Analog Subscriber Carrier Systems and also signed a Memorandum of Undertaking with Philips Kommunikation Industries AG of Germany for the manufacture of the Digital Subscriber Carrier System.

In the year 1991, the company promoted two new companies namely, Himachal Telematics Ltd, at Solan for the manufacture of digital microwave radio transmission equipments and fax machines and Microwave Communication Ltd, for establishing radio paging network in certain important cities of the country.

During the year 1993-94, the company acquired existing investment companies know as Kaldev Trader & Investment Ltd, which was changed to HFCL-Trade-Invest Ltd and Coubndge Construction (Delhi) Ltd. Also, they entered into agreements with telecom giants namely, Kong Song Communication & Electronics Co Ltd, Korea to manufacture radio pagers and satellite video receivers, Dalcons Corporation of Korea for managing credit card information services and Wireless Telecom Ltd of USA to implement V-sat services.

During the year 1995-96, Himachal Telematics Ltd was merged with the company. In the year 1997, the company bagged a contract to set up an information super highway for the basic telephone project of Essar Commvision Ltd in Punjab circle. During the year 1996-97, the companys Optical Fibre Cable Plant in Goa commenced their commercial production. In the year 1998, the company entered the information technology business by offering software solutions to the telecom industry.

During the year 1998-99, the company has received Purchase Orders worth Rs 22 crore for the supply of STM-1 Optical Line Terminal Equipment and advance Purchase Order of another Rs 100 crore for STM-16 Systems. In the year 1999, the company forayed into software exports and developed a state-of-the-art facility at Delhi for that purpose. They bagged a contract from Reliance WorldTel for setting up Internet backbone in Tamil Nadu.

During the year 1999-2000, the company entered a strategic tie-up with the Kerry Packer Group of Australia and formed two joint venture namely, Consolidated Futuristic Solutions Ltd and Excel Netcommerce Ltd in the field of Software and B2B E-commerce respectively. HFCL Infotel Ltd and Consolidated Futuristic Solutions Ltd became the subsidiaries of the company during the year 2000-01.

During the year 2001-02, the company acquired 74% of equity of HTL Ltd, a public sector undertaking, which is the largest switching equipment makers in the country for Rs 55 crore. HTL Ltd became the subsidiary of the company with effect form October 16, 2001. Also, the company divested part of their shareholdings in Consolidated Futuristic Solutions Ltd, consequently Consolidated Futuristic Solutions Ltd ceased to be subsidiary of the company with effect from December 6, 2001.

During the year 200203, the wholly owned subsidiary company, namely HFCL Trade-Invest Ltd merged with the company with effect from March 31, 2003. HFCL Infotel Ltd merged with the Investment Trust of India Ltd, a Chennai based company and was renamed as HFCL Infotel Ltd with effect from September 1, 2002. Also, Rajam Finance and Investments (India) Ltd, which was renamed, as The Investment Trust of India Ltd became the subsidiary of the company by virtue of their subsidiary relationship with HFCL Infotel Ltd. The Investment Trust of India Ltd ceased to be the subsidiary of the Company with effect form September 30, 2003.

During the year 2003-04, the cable division of the company entered into Cable TV market and they emerged as a dominant player in that segment. Also, they received the order valuing of about Rs 220 from MTNL. During the year 2004-05, the company completed the biggest ever order of 200 K Lines of WLL CorDect and 60% of CDMA Infrastructure order of MTNL.

Moneta Finance (P) Ltd has become the wholly owned subsidiary of the company with effect from July 11, 2006.

Recently company acquired Polixel Security Systems Private Limited, this company deals into electronic security and surveillance segment. The move enables HFCL to provide integrated security and surveillance solutions/ systems and optimise from unfolding opportunities in Homeland Security, Smart Cities and other urban rejuvenation initiatives.

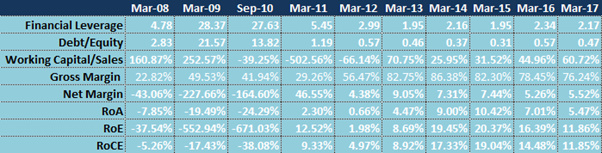

Numbers

Recent News

HFCL focus on Defence segment under Make in India programme of the Government, the Company has been awarded seven Licences by the government for Manufacturing Defence Equipment including Radars, Communication Systems, Weapons, Night Vision Systems, Fuses etc.

Rumours that Reliance Jio, Mukesh Ambani’s telecom arm, and HFCL may announce a merger.

HFCL came on traders radar last month when it allotted warrants to Shankar Sharma of research house First Global at ₹16 each.

Boston-based fund manager GMO bought 1.5 per cent stake in it this month. GMO too has derived good returns from a few small-cap stocks.

Discloser – Pickr members to comment on this opportunity

Not invested , however planning to make small investment to start with