Hi,

I am new to investing field , this is my first attempt to analyze a company in detailed manner.

Company Name: Auro Laboratories Limited

Business: Manufacturing of API especially anti diabetic drugs Like Metaformin HCL etc.

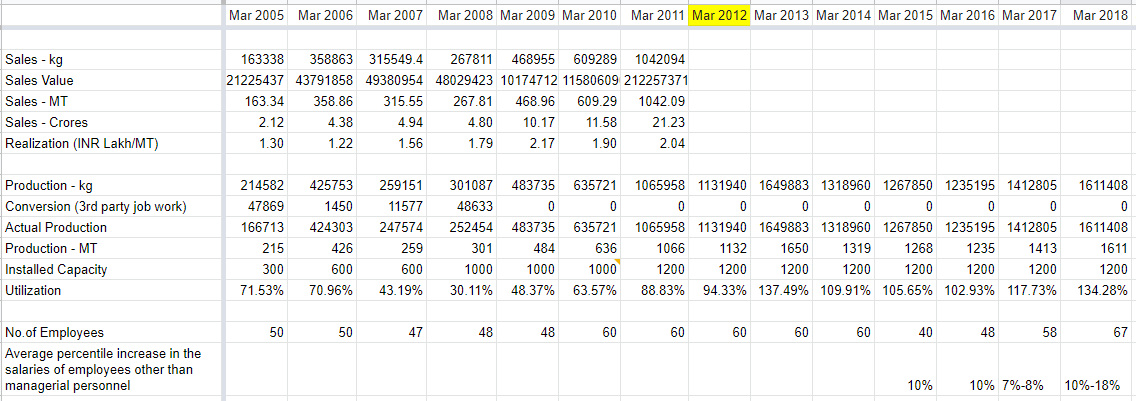

Capacity: On their website it is mentioned that installed capacity is more than 500 MTPA

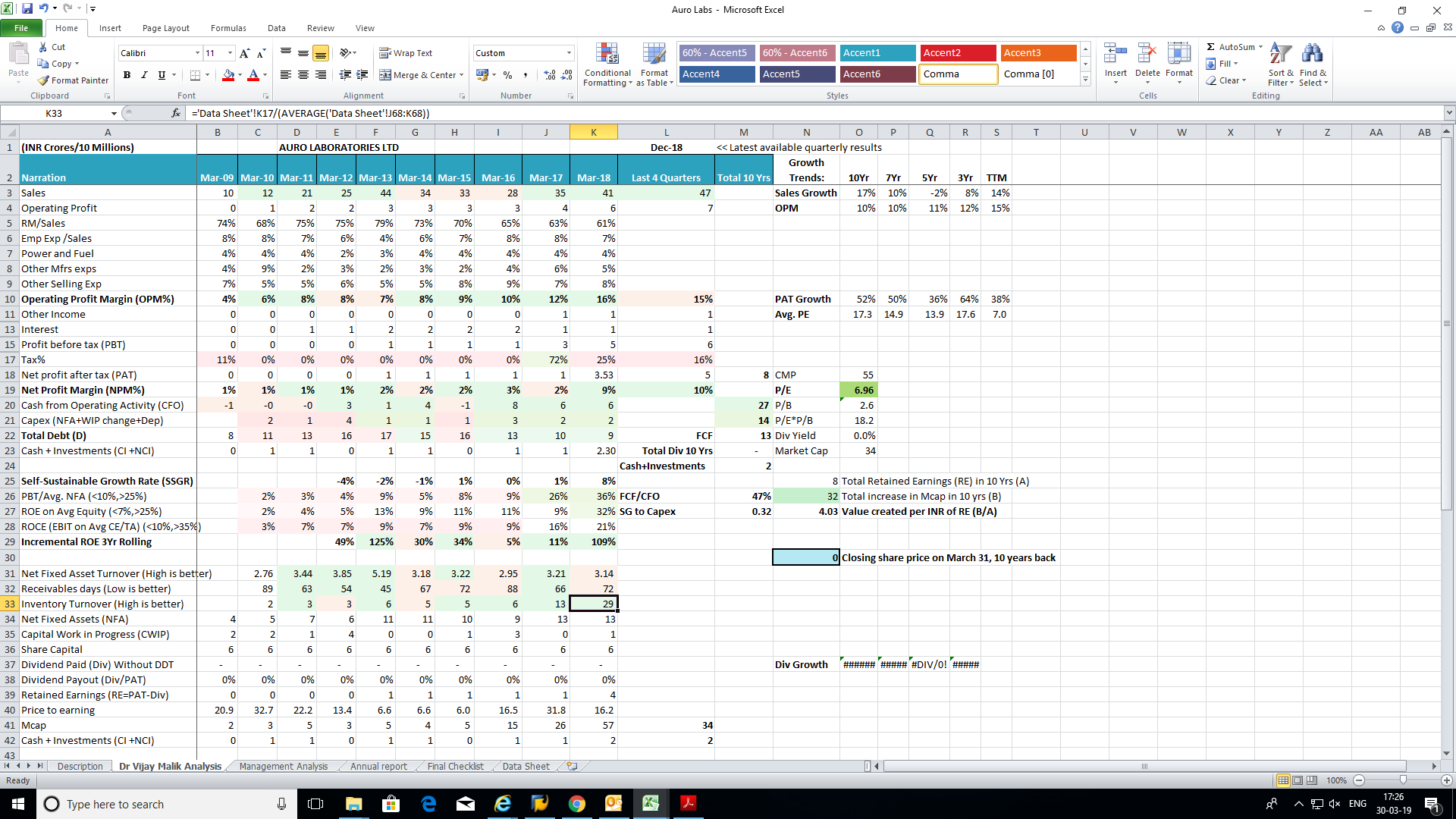

A. Sales Growth :

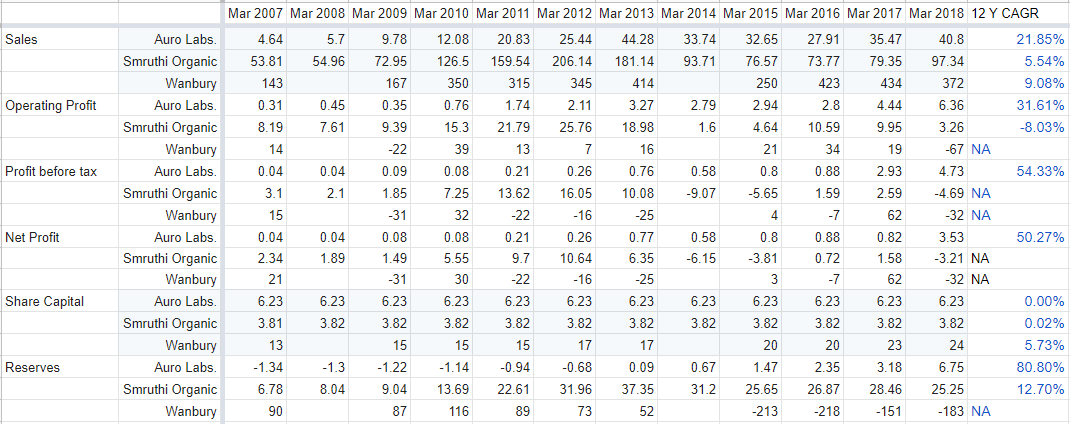

10 Years growth is around 17 %

From 2014 to 2016 there was de growth in sales for consecutive three years, In annual report they stated that it was due to reasons like competition, Low global demand etc.

2017 onwards sales is again on track and growing.

B. Profit Growth :

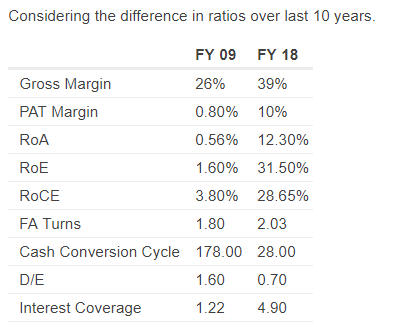

OPM is consistent and growing with a good pace, main reason behind continuous increment in growth is low Raw material cost, may be this is due to pricing power of Auro Labs or due to shortage of API in global market .

PAT growth of last 10 years is 52% against sales growth of 17 %. NPM is also improving due to decrease in Intt cost and higher operating profit margin

C. Financial :

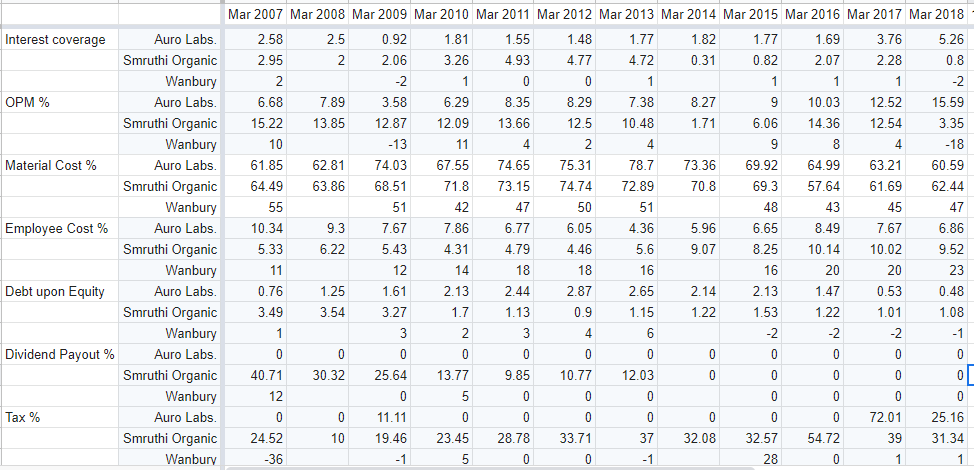

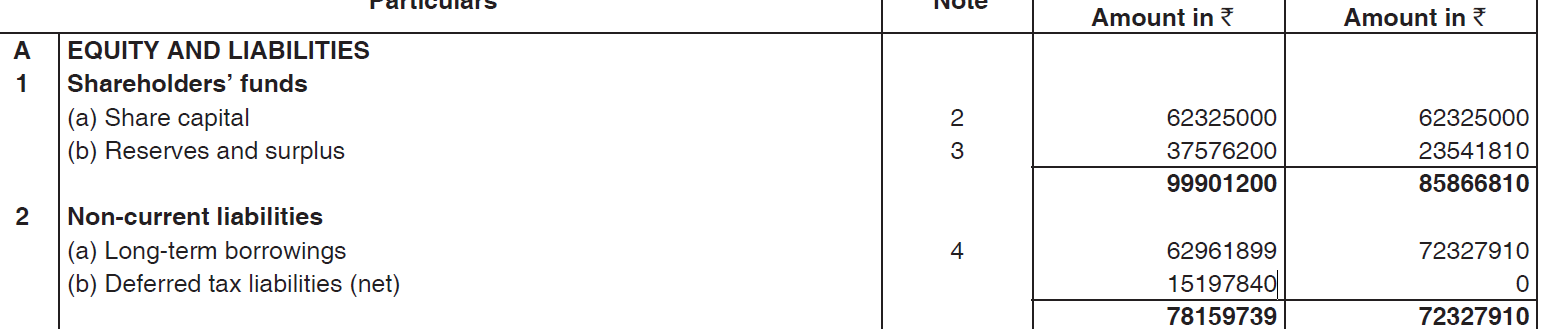

a. Debt equity ratio is 0.7, improving due to repayment of loan from the year 2016. Total repayment from 2016 to 2018 is 7.21 crs. As on 31.03.2018 Debt outstanding is 9 Crs

Debt level is still on higher side and needs to improve further. Intt coverage ratio is 5.6

b. Tax Rate: Tax rate is fluctuating due to DTL and low profitability, in future if company continue to grow its turnover than they need to pay Tax in a range of 30-35%.

c. CFO comparison with PAT and FCF: Cumulative PAT of 10 years is 8 crs on the other hand cumulative CFO is 27. Total capex during last 10 years is 14 crs, healthy Free cash flow is there.

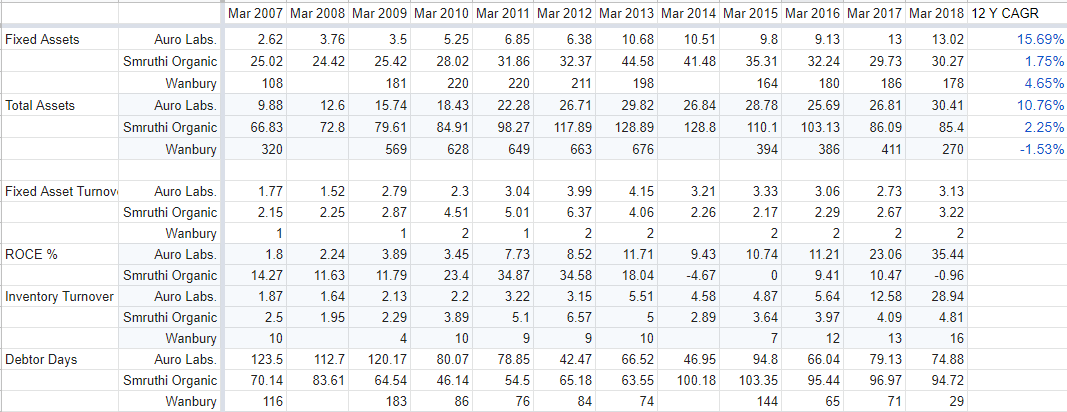

d. Fixed Assets Turnover ratio: From 2010 it is in range of 2.8 to 4, company is regularly doing capex to increase capacity still NFAT is constantly above 3.

e. Inventory Turnover ratio: Is in up trend, which shows efficient working capital management, but in 2018 it was around 29 which will not be easy to maintain.

f. Receivables Level: Debtor’s turnover ratio is constant, if you see cash flow statement of last 3 years they recovered increase in receivables in next year. As on 31.03.2018 more than 6 months outstanding is around 20 lakhs.

g. SSGR vs Sales Growth: Last 10 years sales growth is 17 % and last 3 years SSGR is 8 % still Auro Lab manage to reduce the debt level in last 3 years this is mainly due to efficient working capital management. This is the area where an investor needs to focus because if they do capex in future they need more debt.

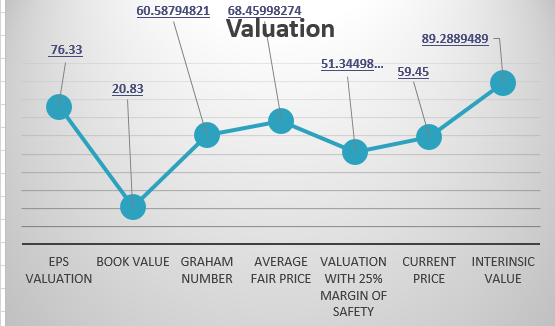

D. Valuation

Valuation wise stock is available at PE level of 7, which provide sufficient margin of safety to an investor.

E. Management Analysis :

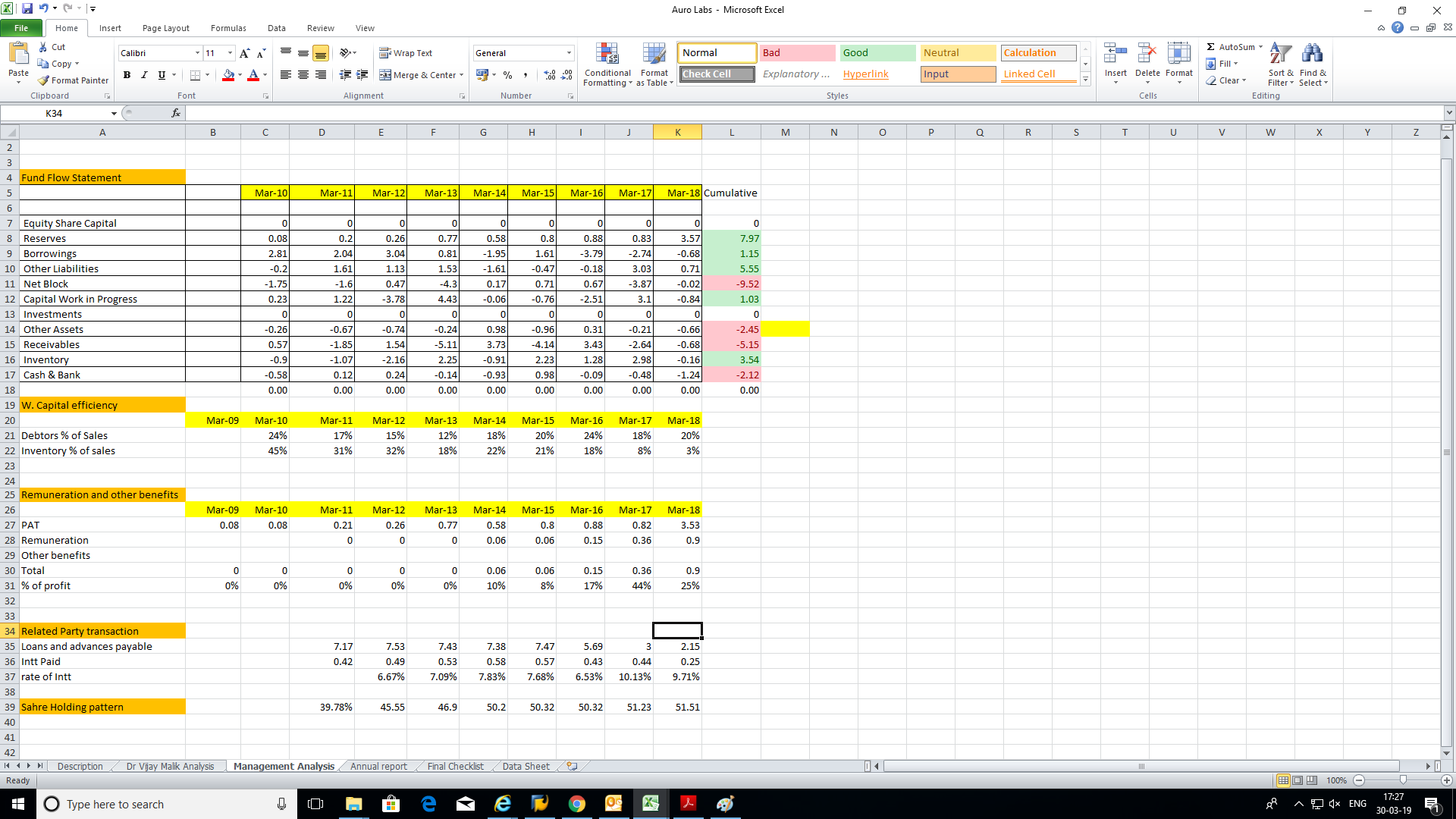

a. Remuneration: From 2014 onwards promoters start withdrawing remuneration, if you see it in % terms may be it is on higher side but in absolute terms it looks moderate. (Please refer management analysis sheet).

b. Share holding pattern: In 2011 promoters hold nearly 40 % stake in company, in last 7 years they bought stock from open market and as on 31.03.2018 promoters hold nearly 52%, which shows their interest in the business. Other than that Ms Shikha lohia who is daughter of Mr Sharat Deorah is also holding more than 1% stake in company, her holding is part of public category.

c. Succession Plan: Mr Siddhant Deorah who is the son of promoter director Mr Sharat Deorah is already in board as whole time director. He is an MBA.

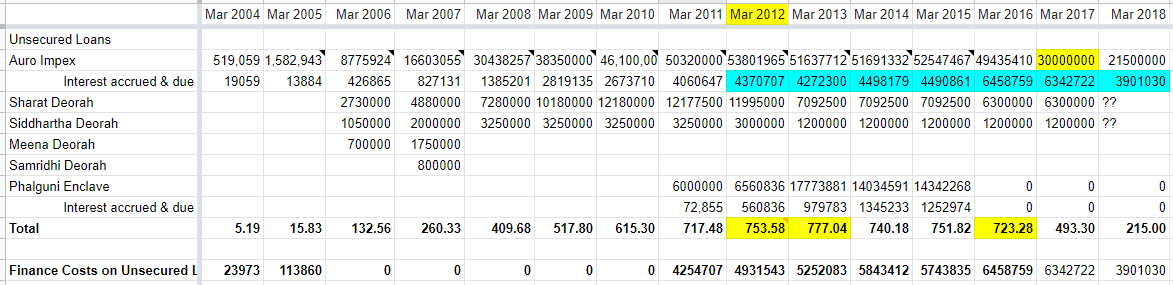

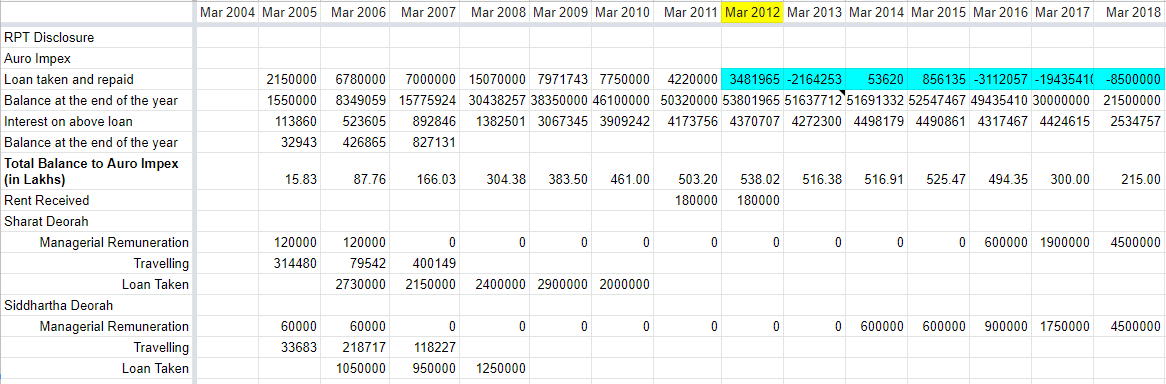

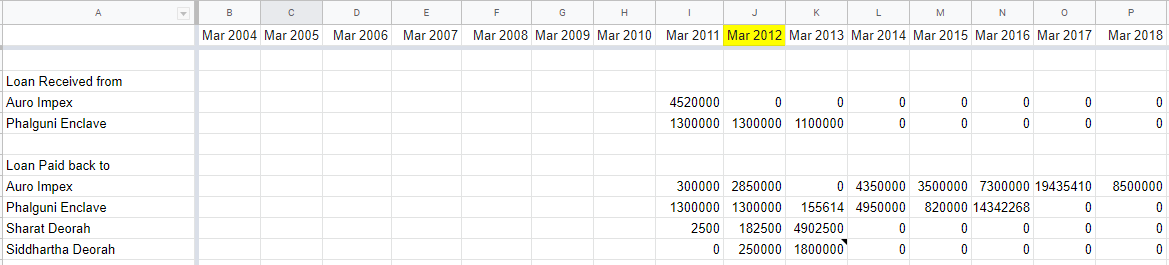

d. Related Party Transactions :Over the years Promoters and associated firms of promoters provided unsecured loan to Auro Lab at a moderate interest rate ranging between 6.7 to 10 % ( Please refer management analysis sheet)

F. Red Flags :

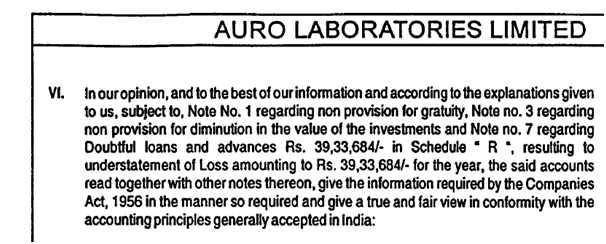

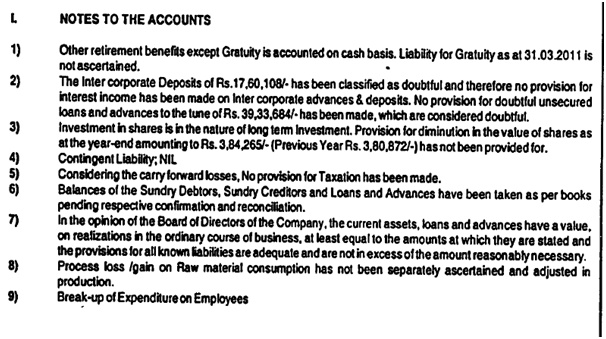

a. Auditor’s Observation : In Annual report of 2010-11 , auditor qualified the report for overstatement of profit due to following reasons :

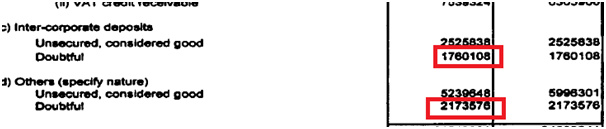

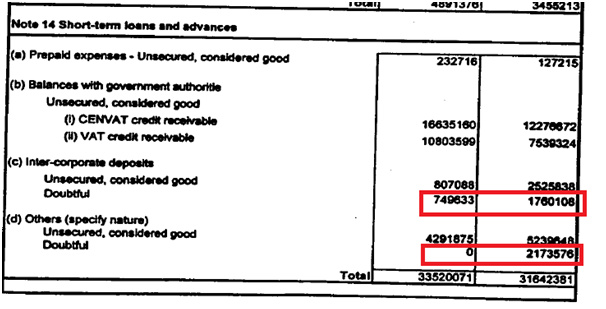

- Non provision for doubtful advances amounting to Rs 39 lakhs. In 2013 AR that amount was reduced to less than 8 lakhs.

Management’s comment on above observation :

In 2013 Amount reduced to 7.49 lakhs and same is still exist on 31.03.2018

- Company was not following Accounting standard 10 of Fixed assets ( 2011 to 2013)

- Gratuity provision was made on cash basis which was not as per AS 15. (2011 to 2016) and same was acknowledged by management in notes to accounts in 2011

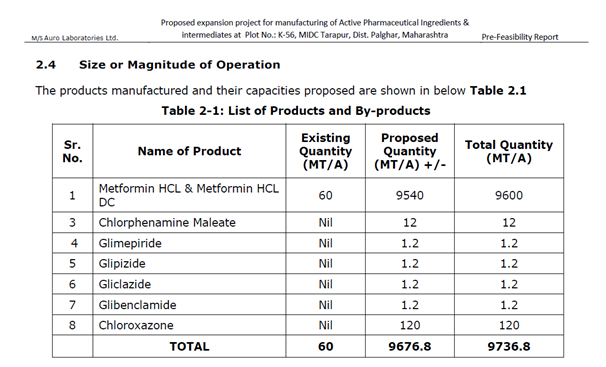

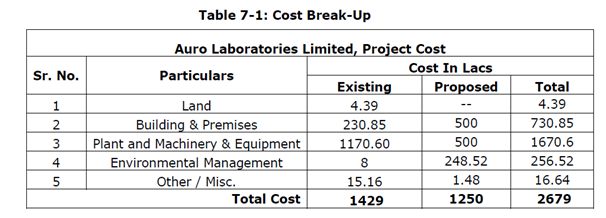

b. Expansion plan: As per Pre feasibility report dated 28.11.2018 available on internet Auro labs is looking for expansion. In that report they mentioned that existing capacity is 60 MTPA. If you look at their web site it is mentioned that installed capacity is more than 500 MTPA and in energy conservation data of each year in AR annual production is in range of 120 to 160 MTPA. A clarification is required from management for more clarity . They want to expand it to more than 9700 MTPA that too in 12.5 crs.

c. Contingent Liability: From 2014 onwards they are showing contingent liability as a foot note and it is in a range of 2.25 to 3 cr. Nature of contingent liability is not clear.

d. Foreign exchange fluctuation: Export sales is major portion of total sales (34 to 60 % ) , the company do not have any hedging policy in place.

e. SEBI complaint: In 2018 company received 2 compliant from SEBI and same was resolved in 2018, nature of complaint did not mentioned in AR.

A mail was sent to company’s investor relation mail ID to clarify expansion plan, exsiting capacity, contingent liability and SEBI complaint. Reply is still awaited.

Basic Data Analysis and Fund Flow Analysis statement

Please provide your feedback/ suggestion for improvement.