Newgen Software Technologies Ltd (NS) is a software products company. They operate in the following product areas:

Enterprise Content Management (ECM)

ECM systems provide for the management of unstructured content – that is everything that is not transactional and therefore managed in databases. Content types have increased greatly over the past few years and now include documents, images, audio files, drawings, social media content, email, and faxes. ECM is an umbrella term for the large number of complementary technologies (and often separate products) that are tightly integrated to provide a platform that, in some cases, provides the end-to-end management of content from creation to deletion or transfer to a permanent archive.

Case Management

Case management is a subset of ECM technologies, which combines content, people, and process. Case management refers to the technologies, features, and functions required to address a particular “case” or task. These tasks are process-driven and generally require a combination of transactional data and content.

Business Process Management (BPM)

A simplistic view of BPM is to define it as a discipline involving a combination of modelling, automation, execution, control, monitoring, and optimization of business activity and workflows to support enterprise objectives encompassing different IT systems and participants (e.g. employees, customers, and partners) within and beyond the boundaries of an enterprise. A BPMS is a software product used for driving process improvements and supports the entire process lifecycle, including process discovery, definition and modeling, implementation, monitoring, and analysis and continuous improvement.

Customer Communication Management (CCM)

There are two elements to customer communications: the first is content creation and the second is the management of the output process, whether this is via print or electronic format. The most common use case of CCM is the batch production of monthly, quarterly, or annual bills or statements in a wide variety of formats for delivery through multiple channels. CCM is also used for ad hoc communications, which may be automatically produced as part of a process. Customer communications is an area served by some, but not all, ECM vendors as well as by specialist niche vendors.

Revenue Streams

The Company’s business has multiple revenue streams including from:

-

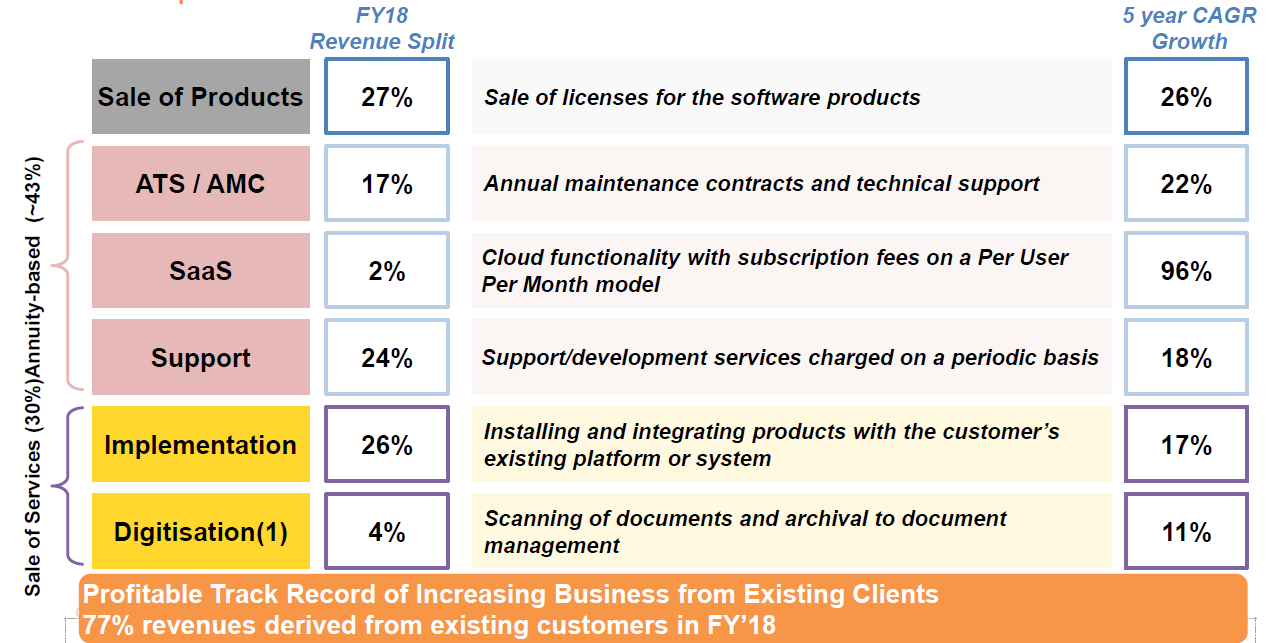

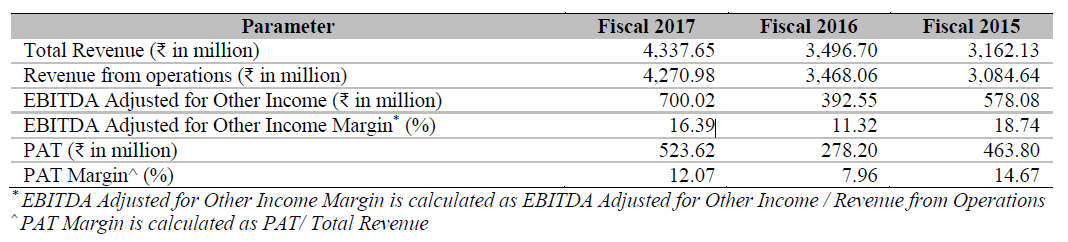

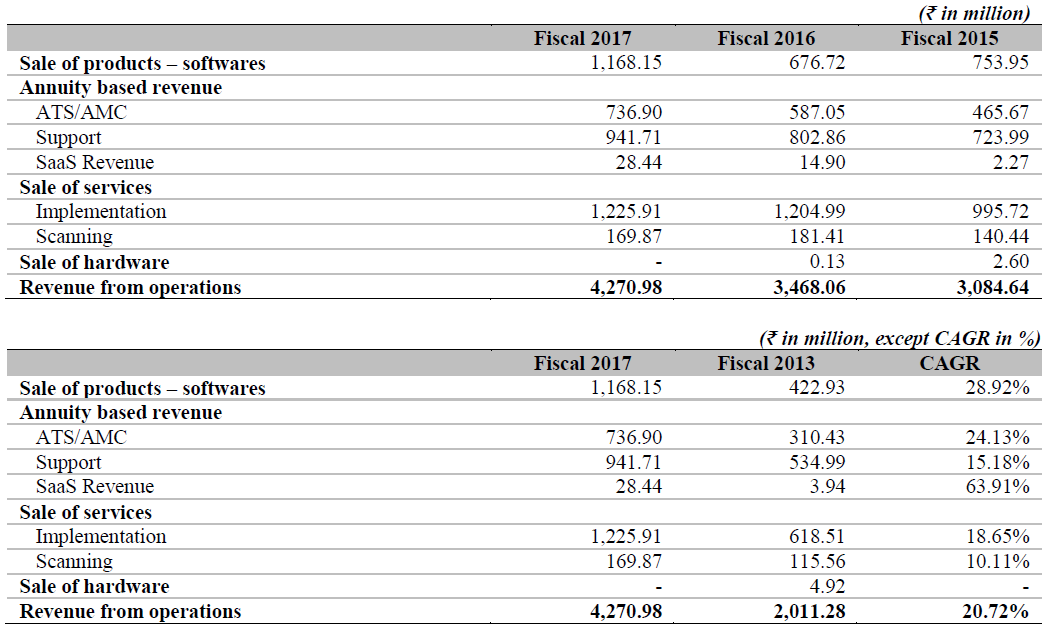

Sale of software products: one-time upfront license fees in relation to the platform deployed on-premise. 137 cr, grew 17% yoy

-

Annuity based revenue: recurring fees/charges from the following: (grew 25% yoy)

- SaaS: subscription fees for licenses in relation to platform deployed on cloud

- ATS/AMC: charges for annual technical support and maintenance (including updates) of licenses, and installation

- Support: charges for support and development services

-

Sale of services: milestone-based charges for implementation and development, and charges for scanning services

-

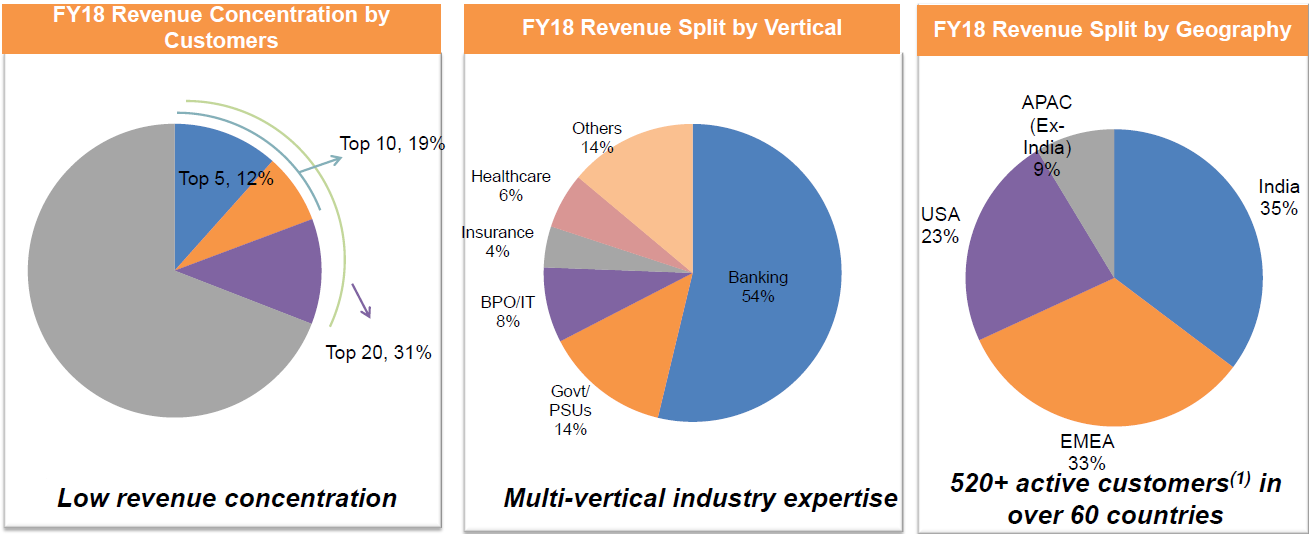

Revenue split geographically - India comprises of 35% of revenues, EMEA 33%, USA 23% and APAC (excluding India) 9% of revenues.

-

Active customer base of 520+ clients running their businesses and critical operations on our platforms in 60+ countries. Added 120 new customers including some Fortune 500 companies.

-

R&D expenditure comprised approximately 7% of revenues

-

Generally this business is very sticky because the profile of customers they are either banks, insurance companies, large governments, so once they make an IT initiative it is a very integrated product doing their mission critical job.

-

The co derives a significant portion of revenue from customers in the Banking, government/PSUs, BPO/IT, insurance and healthcare verticals. In 2017, 2016 and 2015, total revenue from customers in these verticals was 85.87%, 83.21% and 78.76%.

-

Company has declared and paid dividends for the fiscals 2017, 2016, 2015, 2014 and 2013 on the Equity Shares at the rate of 10.00%, 15.00%, 75.00%, 50.00% and 20.00%, respectively.

-

Some of the key active customers include Trust Company of America, Mercantil Bank, ICICI Bank, Trafigura, Bajaj Electricals, United Arab Bank, National Commercial Bank Jamaica, Axis Bank, Yes Bank, Kotak Mahindra Bank, Bank Islam Brunei Darussalam, Philippines Resource Saving Bank, ICICI Prudential Life Insurance, Reliance General Insurance, Max Life Insurance, Strides Shasun and Shriram Transport Finance.

-

Gartner ratings:

- A “Challenger” in Magic Quadrant for BPM-Platform-Based Case Management Frameworks

- A “Niche Player” in Magic Quadrant for Enterprise Content Management, 2016

- A “Niche Player” in Magic Quadrant for Intelligent Business Process Management Suites, 2016

- A “Niche Player” in Magic Quadrant for Customer Communications Management Software -

Solution Frameworks across verticals

- Banking - Account Opening, Retail Lending, Commercial lending, Corporate Lending, FATCA compliance, Trade Finance, Collections and Payment Systems

- Government/PSUs Correspondence Management, Agenda Management, Citizen Centric Services, Office Automation and Grants Management

- BPO/IT - Accounts Payable, Accounts Receivable, Invoice Processing and Vendor Portal

- Healthcare Provider Contract Management, Complaints, Appeals and Grievances Management, Mobile Member Enrolment and Claims Repair

WHAT IS INTERESTING

- Software products have a non-linear business model. The revenues can rise with significant margin expansion with addition of new clients.

- Increasing use of SaaS (software-as-a-service on the cloud) canbring in long term annuity kind of revenues.

- Diversified customers including a large part coming through annual maintennance / support contracts providing earnings visibility

- Very sticky business. Long term customers usually do not leave once they have been using the products for some time.

RISKS

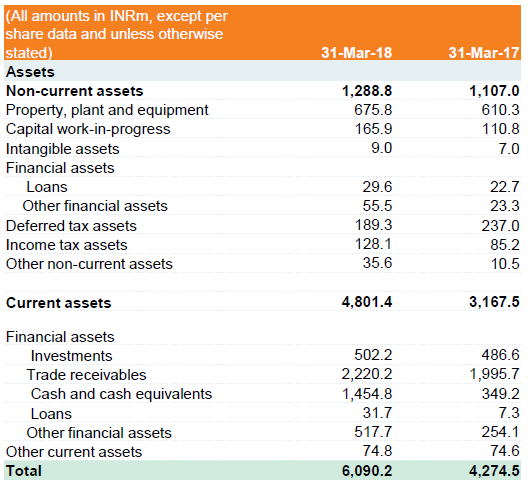

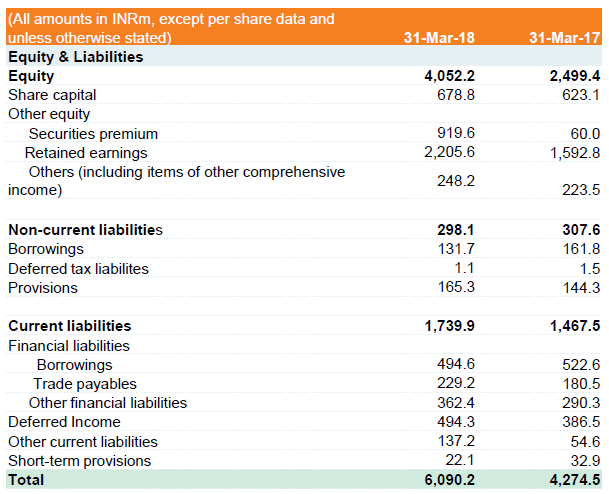

- Receivables is quite high at 222 cr on Mar31, 2018. Debtor days are above 150 days. The co acknowledges that this is an issue and is looking for active measures to reduce this. However, due to the long term nature of contracts, it will not come down drastically.

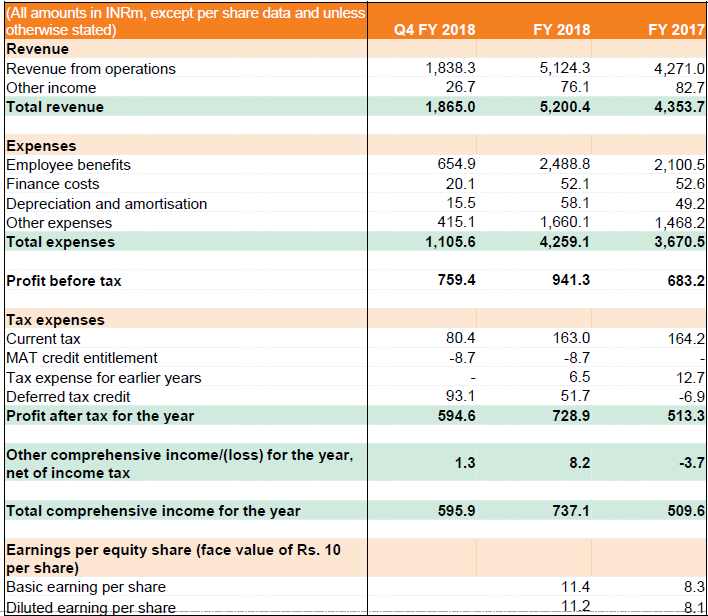

- There is seasonality in revenue generation. Most of revenues come in Q4.

- Product business is lumpy and there is usually needs an upfront investment in terms of sales and marketing expenses. New customer acquistion is expensive and time consuming.

- Very competitive field with large global majors in each of the product areas that the company operates in

- Technology change and obsolense is fast. Company needs to continuously upgrade their product to be in the reckoning.

DISCLOSURE:

I do not have a position currently in the stock. I am studying the business and may or may not decide to take a position in the future. Please do your own due diligence before investing.