Introduction

StuCred -Instant Credit App For College Students in India, is the tagline of the company. FinTech in true sense and a unique business model of lending and empowering students with basic knowledge of Personal Financials.

Parent company Kreon Financial Services is a 25+ year old NBFC decided to start StuCred an App based fully digital loan providing company.

2 UK Graduated Brother and Sister returned to India with an experience of Overdraft facility for students studying in UK universities. New blood has taken over from old, Jaijash Tatia and Henna Jain Tatia are now steering this Fintech startup which is profitable and is a rarity in Fintech world.

About Business

Kreon has a legacy NBFC biz which they are downsizing and focusing more on Digital lending App. I will not go to legacy lending biz as i did not dig deep in to it.

2-1-0 Lending

2- Min Authentication 1- Min Credit Transfer 0- Human Interference

Commercial Lending Division- Interest Income + Dividend Income + FD Interest

Digital Lending Division- Fees & Commission + Penalty Income

Digital lending is possible due to UPI & IMPS & E-Aadhar

About App

One also need to notice that the loan tenure are very short 60-90 days so they have to be on their toes for growth. Have to give loans multiple times to the same students in a single year apart from getting new students onboard. Which a weakness in my view.

Extracts from ARs and Company update

-

Change of management started in year 2018-19, young siblings took over KMP roles.

-

launch of StuCred App on Vijayadashmi. Banking partner YES Bank.

-

Loan during lockdown 20 million, 6000 students and 10000 number of loans

-

Partnered with PayTm as trusted merchant lender.

-

Approved 3.75 lac equity share at 20Rs to Jaijsh against loan.

-

Approved 4.25 CCS at 100Rs later changed it to 3.1 lac share against loan by Jinpad Dev related party.

-

5 Lac Digital transaction till SEP-21 and Tie up with ICICI Bank

-

Considered rights issue but dropped it and issued 95 Lac warrants to promoters at 21 Rs so total 19.95 Cr would come to company in next 18 months updated on 28/10/2021

-

Total share after all the preference, CC and Loan converstion- 2.0246 Cr **So current market is misleading it is double of what it is **

-

Company is investing in developing new app for wider segment that is the Hint of Footprint expansion.

-

Propose to change of name to Kreon Fintech Ltd

-

Launch of New products Cross sell and up-sell to existing good customer.

-

Started Alumni program.

-

Expansion so moved to new office in Chennai.

-

Timeline: Registered Students

6000 Year March 2020

60000 Year June 2021

100000Year Sept 2021

300000 Year June 2022 (Henna Jain Tatia on her Linkedin)

500000 As per my notice around Aug

1000000 As per current status on Play store

-

Credit Rating for Proposed Fund Raising BB/Stable

https://www.brickworkratings.com/Admin/PressRelease/Kreon-Finnancial-Services-15Sep2022.pdf

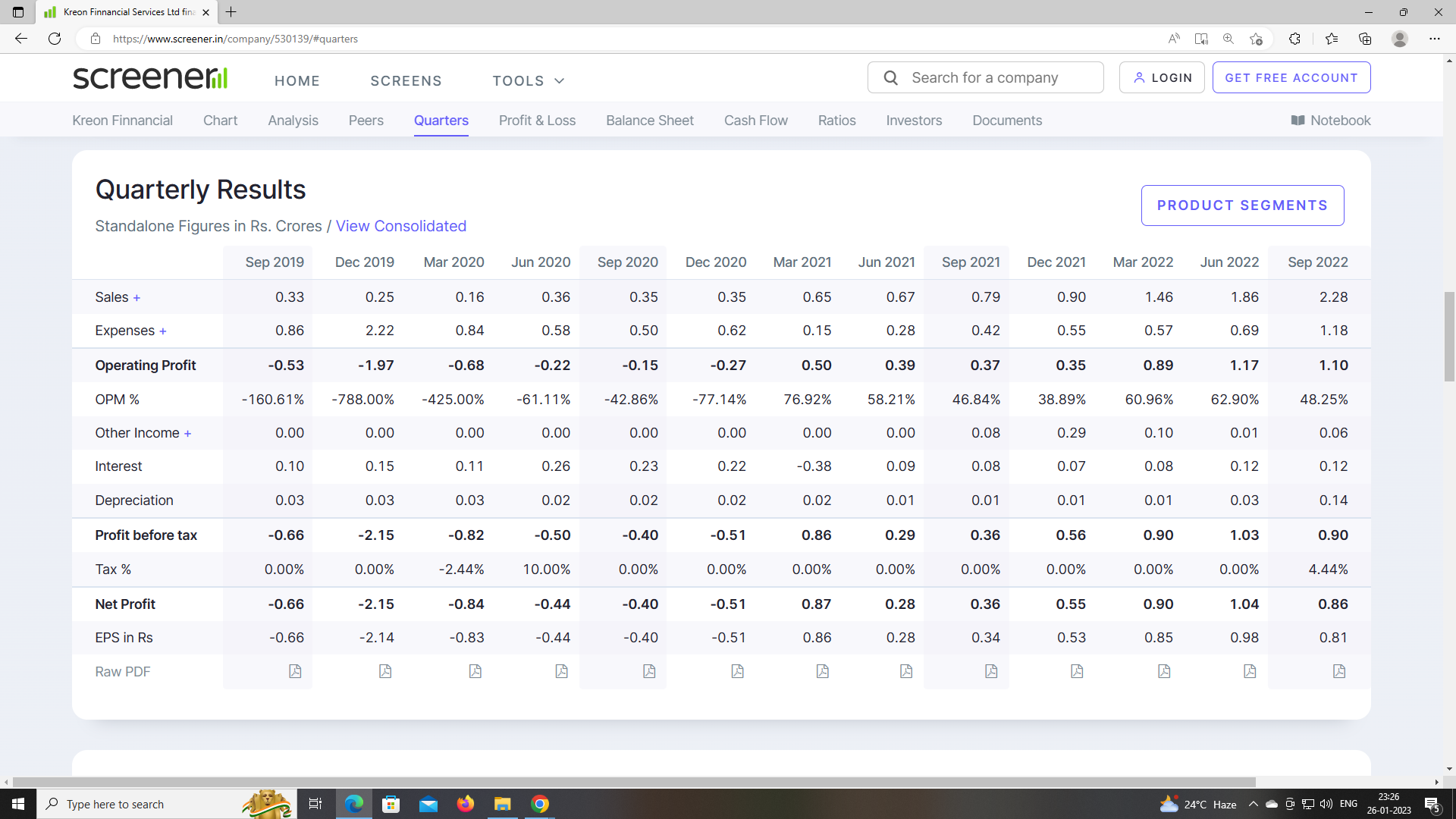

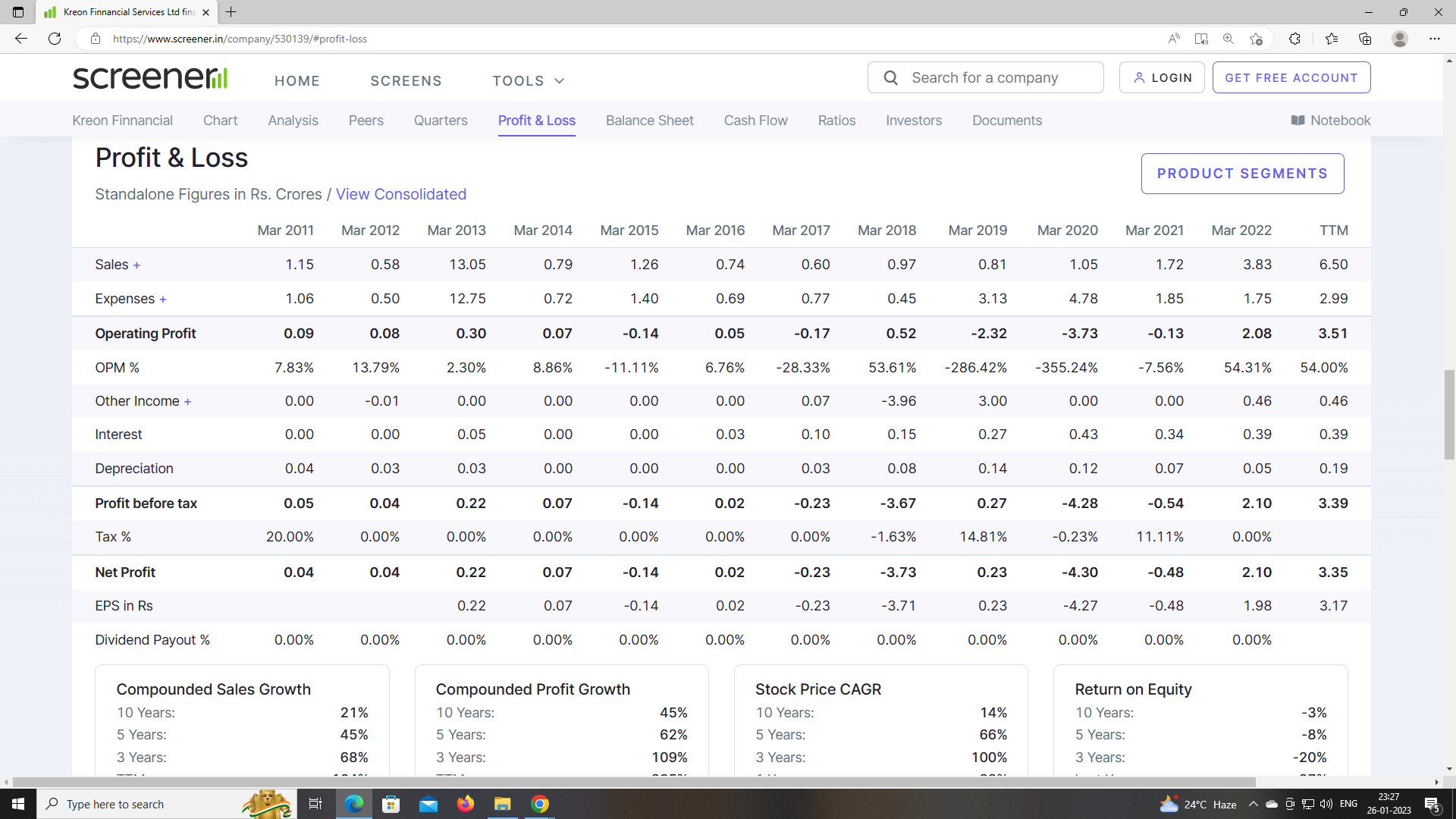

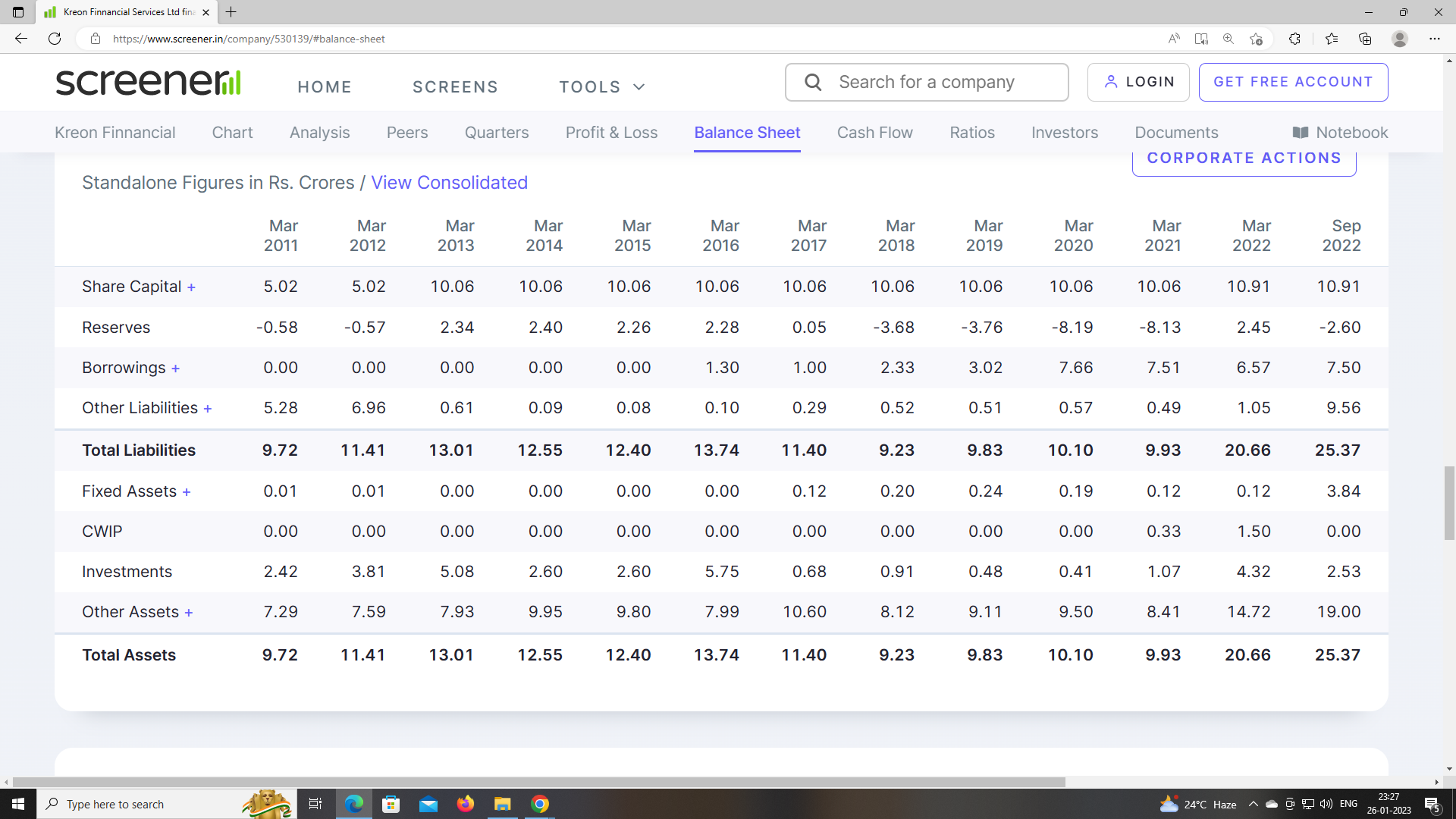

Financials

Hiccup in profit profile during latest Sep-22 Quarter is due to change in accounting for Intangible asset under development ( App development is a ongoing process), increase in salary and increase in Rent (new office space). All these expenses will have lower impact going forward on profit.

What i like in this biz is its profitability and return ratio. They may grow without borrowing which is phenomenal in itself. Also monthly revenue growth rate is in higher single digit which is very encouraging and not going down till now. As per my calculation they are about to cross 1 Cr + revenue/ month in Jan-23. Due to short term nature of this biz one should understand that Loans and Advance in balance sheet is not throwing full light on the disbursed loan during the year or quarter.

Lets see that March-22 balance sheet shows Loans as 13 Cr ( as per my observation StuCred is disbursing more than 16 Cr per month now) but as per credit report

The total income from operations for FY22 has increased to Rs 3.82 Crs from Rs. 1.71 Crs for FY21 due to consistent fresh disbursements made in FY22 of ~Rs.28.23 Crs and total disbursements of Rs. 39.77 Crs. ROA and ROE have improved to 3.43% (FY21:-1.20%) and 6.87% (FY21:-6.23%).

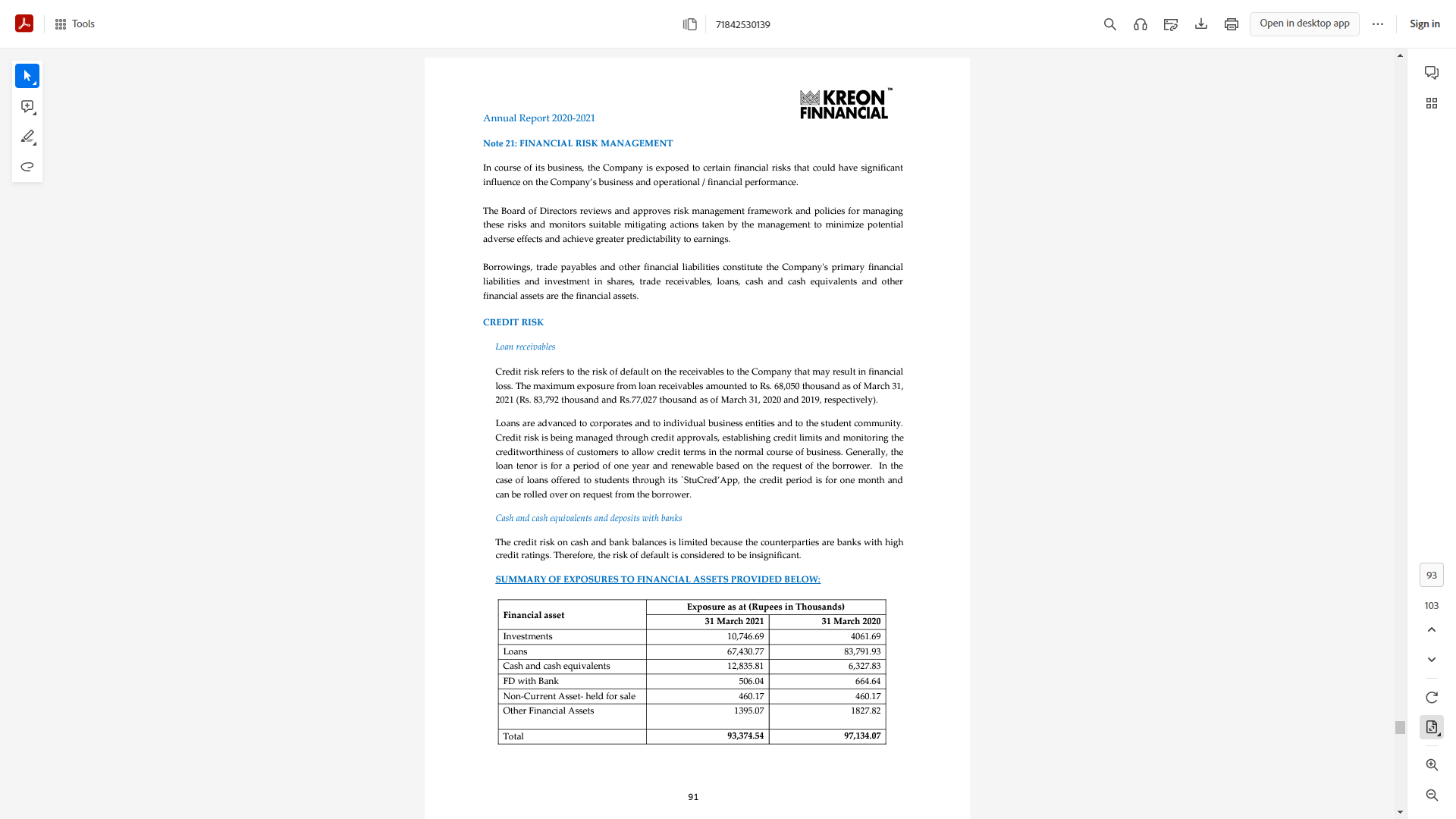

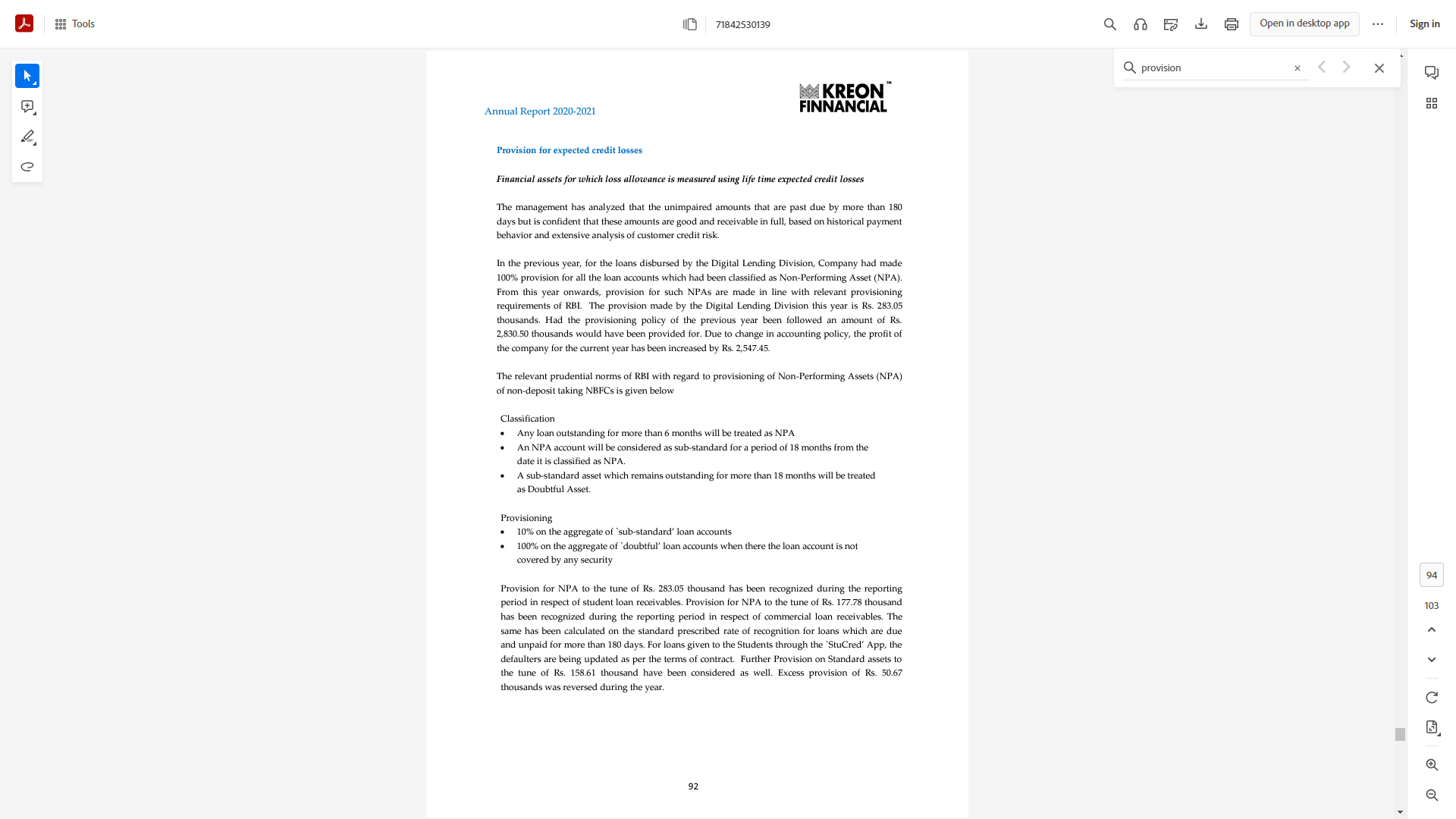

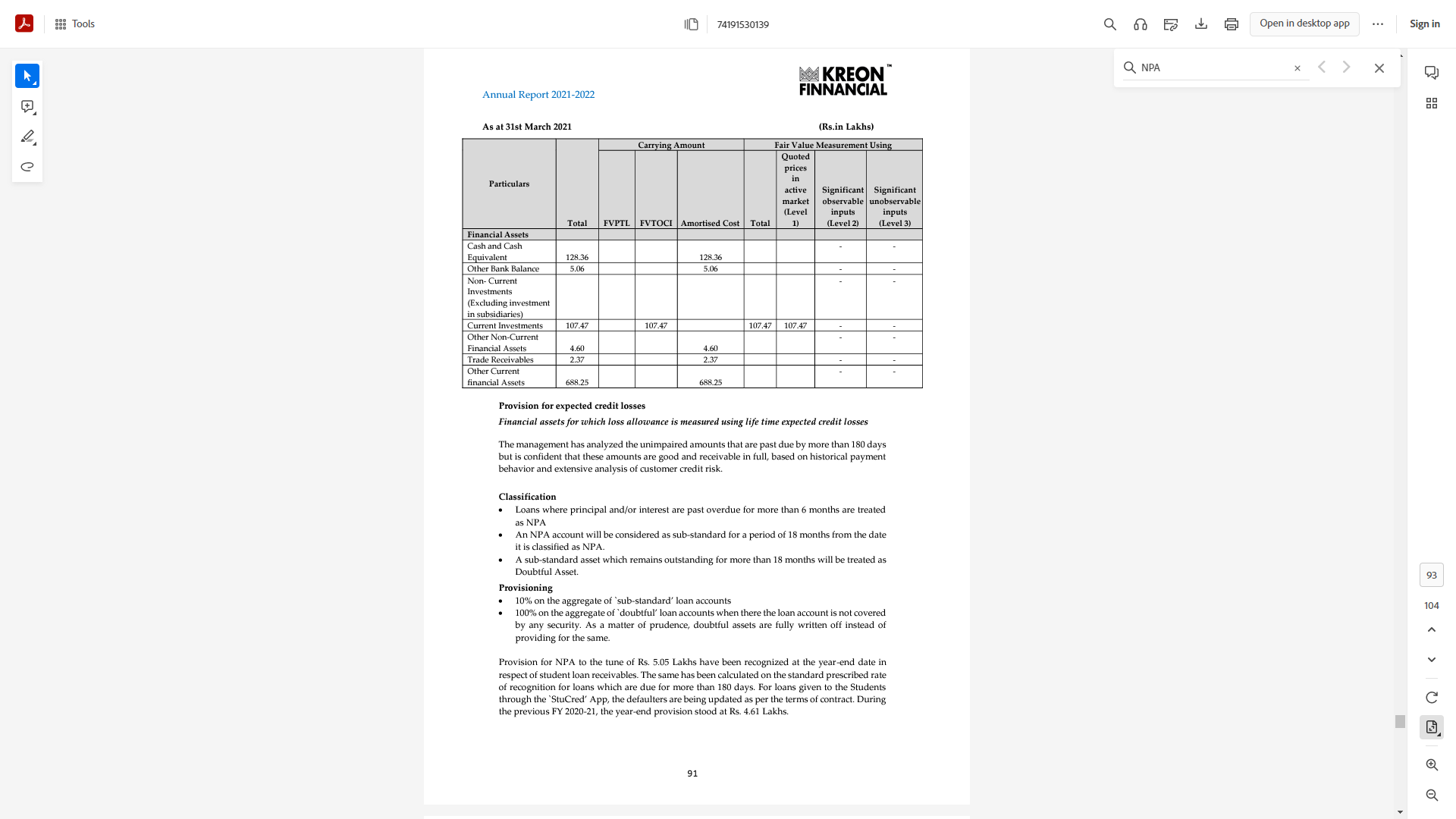

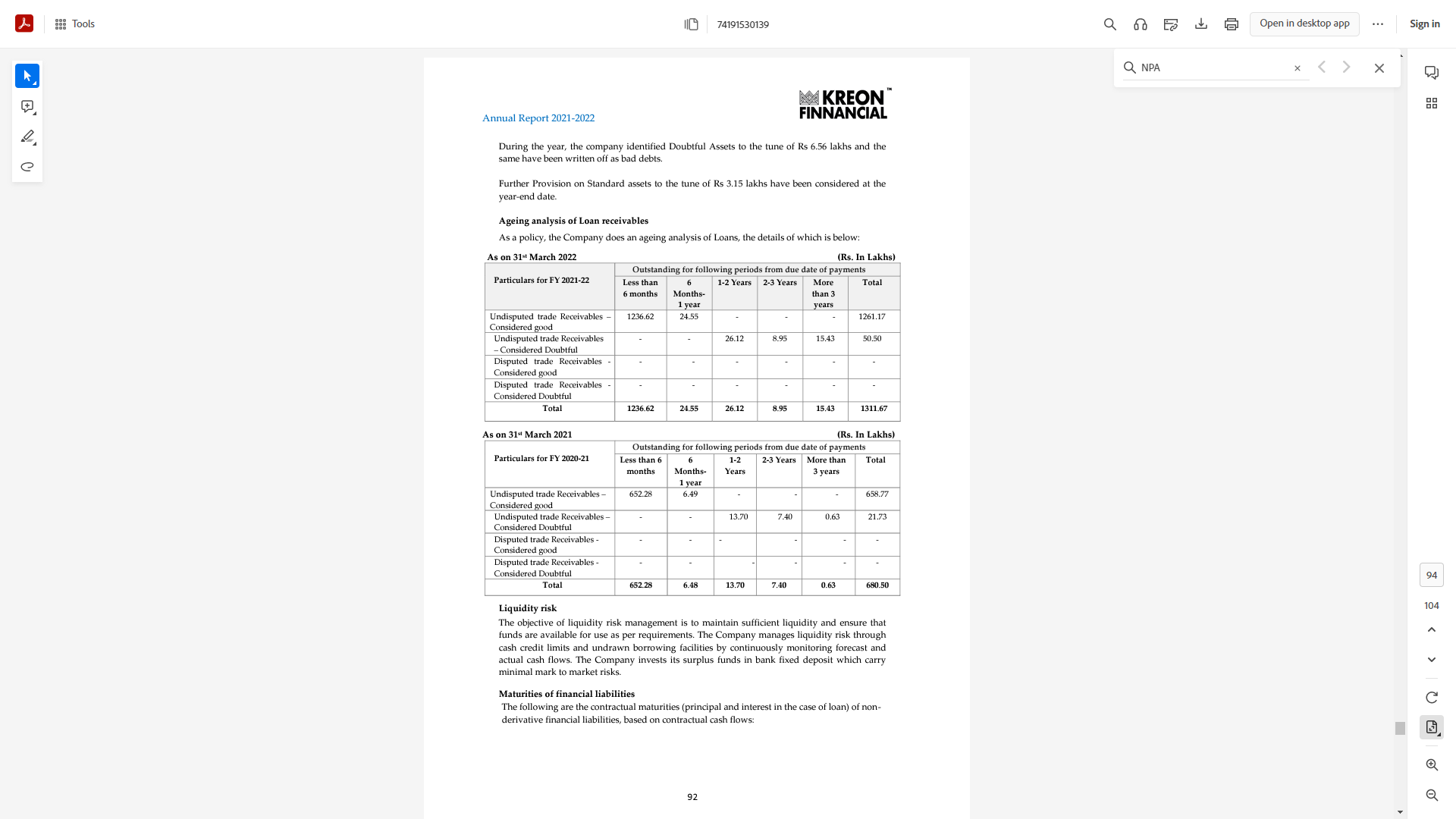

So if we go by credit rating’s analysis of net NPA is 4% so it is only 52 Lac on total disbursement of 40 Cr. More can be analysed after looking at below AR info.

Kreon.pdf (443.6 KB)

Management

While looking at a microcap it is most important thing. Jockey will only decides the success and failure of business. Again i did not study old guard but just googled and referred AR for their qualification.

Mr.JaijashTatia is a business graduate from Regents

University, London, specializing in Financial Economics

and Business Management consisting of various courses

including Asset Management and Risk Management. He

has undergone various additional modules such as,

Managerial and Financial Accounting and Statistics at City

University, London, United Kingdom. The Company is

benefited from the knowledge and expertise of Mr.Jaijash Tatia.

Ms. Henna Jain ,flourishing young entrepreneur, she has been one of the team members at the helm of StuCred since August 2017, and has been positively contributing to the areas of marketing and business operations. She holds an MA (Hons) International Relations and Economics from University of St Andrews, Scotland. In an effort to constantly expand her knowledge and expertise, she has completed 3 advanced level online courses in Marketing, specialising in Social Media Marketing from Northwestern University, USA

When there was tough times during covid this is what management did to cut cost

Salary + Intangible asset under development(App development charges):

- FY19-20- 1.9 cr

- FY20-21- 1.57 cr

- FY21-22- 1.72 cr

- HY22-23- 1.22 cr

Henna is not taking any salary till now and Jaijash salary was 24 lac, 12 Lac and 24 Lac for last three years. New remuneration for Jaijash is 60 Lac PA.

One can see that management at top is competent to run this biz.

Miscellaneous

- I could not find any listed pure App based lender if anyone know please post here.

- There are lot of App based loan company and it has to compete with them likes of mPokket,

- Total addressable market is more than 3.3 Cr students in India (Higher Education).

- Some old article on StuCred

https://yourstory.com/herstory/2020/04/woman-entrepreneur-fintech-college-students-loan

Kreon Finnancial Services launches mobile app - StuCred | Business Standard News

Creditor Queen

No more financial woes for students thanks to Chennai-based startup- The New Indian Express - I tried connecting company but haven’t got any reply yet if anyone can get in touch with the Management then it would be great help for understanding more about their vision.

Valuation

I would like to discuss and know more about the valuation it may command. I could not give it valuation so its open for discussion.

Current Mcap= 100 cr (after taking dilution)

Risk Analysis

- High cost of funds.

- Rising NonPerforming Assets (NPAs).

- Competition from other NBFCs and banks

- RBI is taking very proactive measures and laying rules and regulation for new age Lending biz. Complying those updated regulation is the key to success. Recently RBI have put ban to some App based lending companies citing non-compliances.

- I am not a fan of Related party transactions and kreon has many related party transactions and high cost borrowings from its related party, i see it as a risk.

- In Nov-22 App went offline due to some issues and management was not able to fix in fast it took some days so depending upon IT Tech and robust IT Infra is must for such type of companies. Though it was a first instance.

- Any restriction by Govt on uses of Aadhaar based KYC or digital infra build by Govt will permanently damage the biz. So its also a risk.

- In my limited understanding current growth is self sustainable through internal accruals and dont need external funds to the tune of 25 crore out of which 15 cr will come before july 23(share warrants) and proposed fund of 10 Cr. So unnecessary equity dilution is not good for a borrowing biz. Equity is the most important thing in lending biz selling it cheap will deter me from investing.

Disc: Holding