Hi Harsh ,

I see that you are holding ITC as largest position in your portfolio. Can you share your investing style - are you doing sip or buying in dips in general and also in case of ITC?

Thanks!

Hi Harsh ,

I see that you are holding ITC as largest position in your portfolio. Can you share your investing style - are you doing sip or buying in dips in general and also in case of ITC?

Thanks!

I sold my 2% stake in Care Ratings as I don’t have clear visibility on their future growth trajectory. It seems CRISIL has gained significant market share from everyone else as evident in their growth in last few quarters. This leads to buildup of a 2% cash position which I will deploy soon. Updated folio is below.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| RACL Geartech Ltd | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

Hi!

About ITC I have been holding ITC for the last few years, I increased the position size to 8% in 2021 as valuations became very cheap and there was absolute ridicule around the stock. Business wise, they have done reasonably well. This being said, I sold some ITC shares in past few months to bring position size back to 8-10% and rebalance to other positions.

About general investing style I am value focused bottom up investor who likes to incorporate multiples styles within my portfolio. I hope not to make blunders at a portfolio level, and perform reasonably over cycles. Reasonable outperformance over long periods of time makes for unreasonably good track records, thats my attempt!

Hi @harsh.beria93!

I notice that you have a pretty spread out portfolio with the highest allocation being 8%. Can you elaborate how you decide your portfolio allocation strategy/concentration? Do you want to limit the max drawdown in your PF or do you target a particular CAGR over a number of years? Also do you have a core vs satellite portfolio strategy or do you hold everything in a core portfolio?

Its always a trade-off between concentration and diversification right? What guides this balance for you?

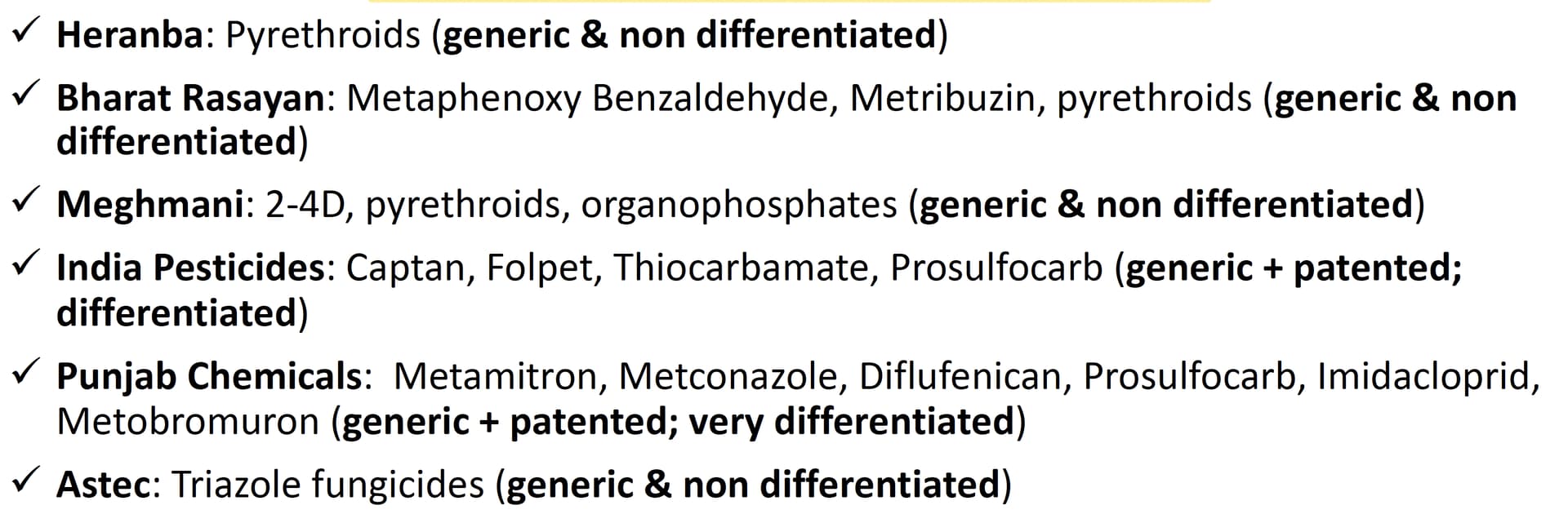

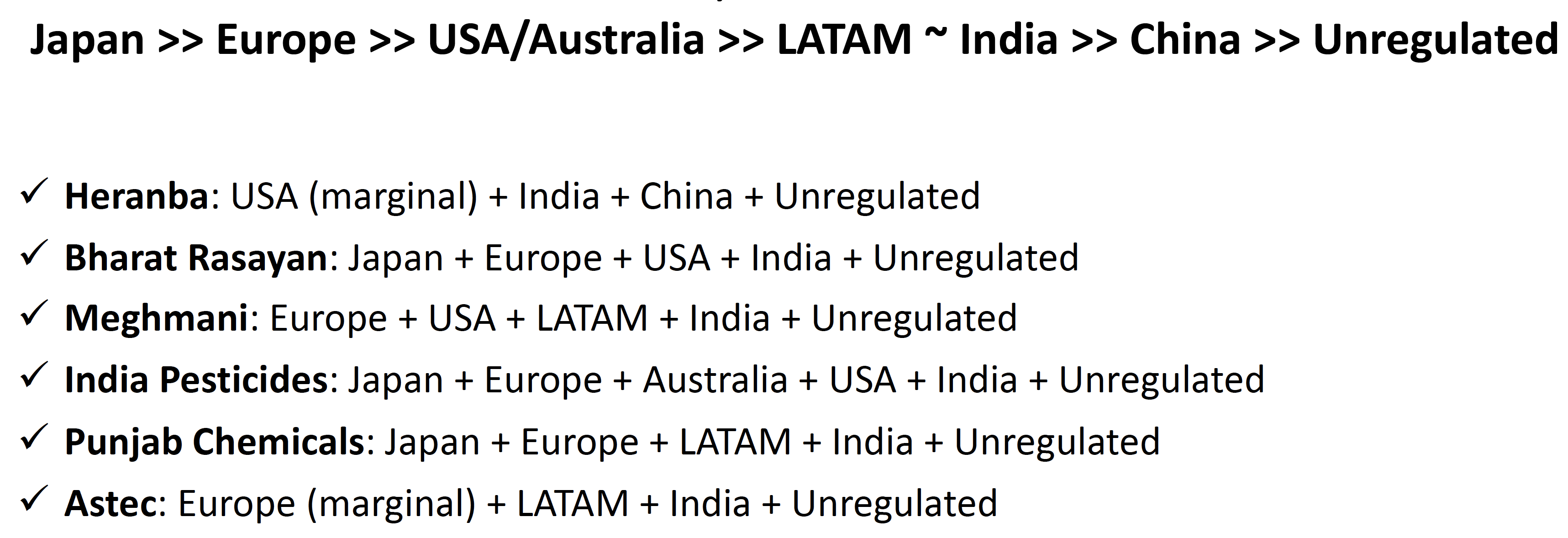

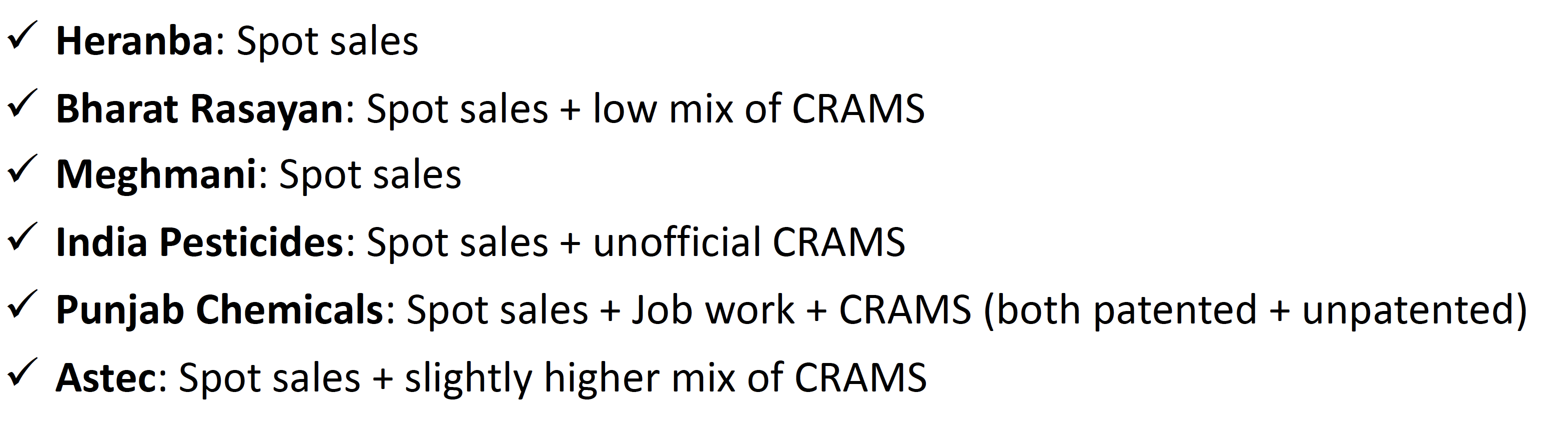

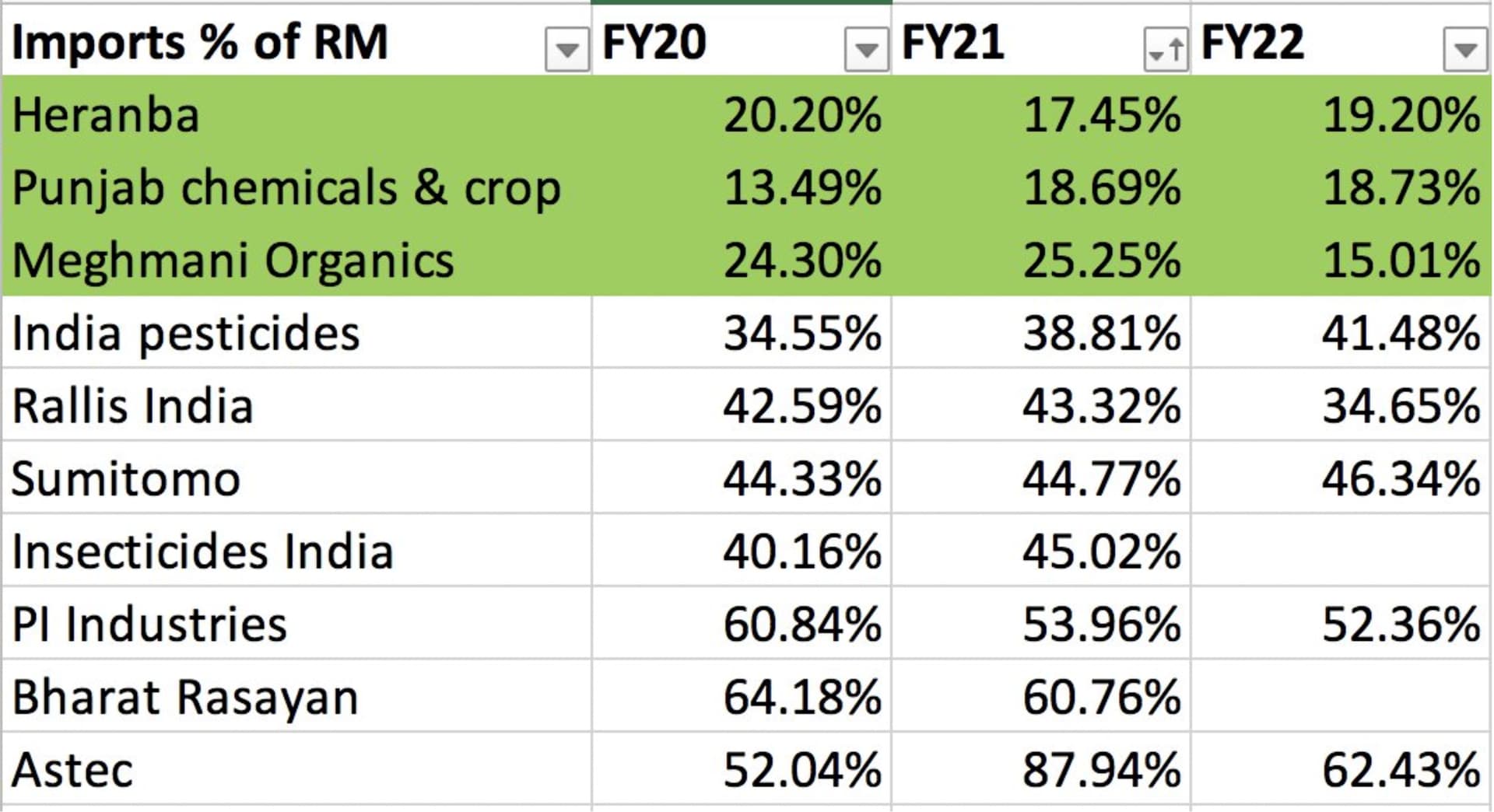

I made a follow up presentation on the agchem space where I categorized cos by different criterias like: complexity of core molecules, end selling markets, business model and level of backward integration. I compared 6 cos in this presentation (Punjab chemicals, India Pesticides, Meghmani Organics, Heranba, Bharat Rasayan, Astec). Key takeaways are summarized below.

Molecule complexity: Punjab Chemicals ~ India Pesticides >> Meghmani ~ Heranba ~ Bharat Rasayan >> Astec

End markets: Punjab Chemicals ~ Meghmani ~ India Pesticides ~ Bharat Rasayan >> Astec >> Heranba

Business model: Punjab Chemicals >> Astec >> India Pesticides >> Bharat Rasayan ~ Meghmani >> Heranba

Backward integration: Heranba ~ Punjab Chemicals ~ Meghmani >> India Pesticides >> Bharat Rasayan >> Astec

The presentation is also available at the link below. I will be happy to discuss further as this space is seeing good growth and valuations are also reasonable.

As of today, I have increased my position size in Punjab Chemicals to 4% from 2% earlier. This brings down cash to zero.

Brief thesis: Most Indian agchem cos are strong in insecticides, particularly in pyrethroids and organophosphates range of molecules. In past few years, a lot of capacity has come up in these molecules and I expect realizations to be impacted going forward. With this context, I find Punjab and IPL as differentiated as they are not reliant on pyrethroids or organophosphates. Instead, they are making niche molecules where they are the only major producers out of India. As a result, both IPL and Punjab have been able to get dominant global market shares in their core molecules.

For context, Punjab’s largest products are Metconazole, Metamitron and Diflufenican. Their exports shares in these products are shown below:

Metconazole: 40%

Metamitron: 65%

Diflufenican: 100%

Recently, Punjab launched prosulfocarb and thiocyclam. In prosulfocarb, the other significant Indian co is IPL and in thiocyclam, there is no one else from India.

If we were to look at margins, IPL’s margins are the highest in this industry, whereas Punjab’s margins are much lower. On a gross margin basis, Punjab’s margins are much higher than industry averages, however the same is not reflected at the EBITDA level. I feel with scale up, Punjab’s margins can go to 18-20% levels in next 3-years. If that happens, Punjab can make 150 cr.+ profits in next 2-3 years which makes for an interesting risk reward situation.

The reason for me choosing Punjab over IPL is both are trading at similar multiples, but there is a larger scope for margin expansion in Punjab vs IPL.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| RACL Geartech Ltd | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

Hi harsh, Can you plz throw some points on future prospects of Amara Raja Batteries. Lead acid batteries is a decaying industry.

I have shared my thought process on allocations before, you can read more here.

Also, this debate about diversification is rather meaningless. Our time should be spent more on improving our understanding about businesses or in formulating new investment strategies. There are people who have built meaningful track records with 5 and 5000 stocks, choose anything which resonates with you.

Also, given that I am running a long only folio, I cannot control absolute drawdowns. If market goes down, my folio will go down with it. However, I can control my own allocations on stocks on the basis of current risk reward and try to minimize mistakes.

Hi Ravi,

I feel its wrong to assume that lead acid batteries is a decaying industry. If we look at underlying industry trends, lead acid batteries are still growing volumes. Any my thesis with Amara Raja is that their margins will improve with lead prices coming down as their competitive positioning is the same (or even stronger) than the case 5-years back. I have shared my thoughts at link below.

With a sharp price drop in RACL Geartech, I have increased its position size from 1% to 2% and changed its basket from being a deep value bet earlier to now being a cyclical bet. As cash position was anyway zero, I have reduced position size in Manappuram Finance from 4% to 2%. Interestingly, I didn’t have to sell shares of Manappuram to reduce the position size, the sharp cut in stock prices did the job ![]()

Last couple of years have been really good for RACL with strong earnings growth coming in on the back of continued sales growth and expanding margins. Market has also recognized the same and stock has moved up a lot and doesn’t trade at very cheap multiples anymore. From a near term perspective, RACL can be adversely impacted due to on-going European energy problems. However, the management seems very confident of achieving 20%+ sales growth while maintaining margins over the next 3-years. If that happens, I expect their PAT to reach 45-50 cr by FY25 (20%+ EPS growth on FY22 base). However, valuations are also fair at 20x earnings. Given the risk reward, I have still not made it a full position and limited exposure to 2%. Updated folio is below and cash remains at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (5%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

As of today, I have utilized the 1% remaining cash position to add Suyog Telematics as a deep value bet, which brings down cash to zero.

In the last couple of years, I have been reasonably successful at implementing a deep value strategy, where the idea is to buy reasonable cos at very good prices & hold for 2 years to see if there is some kind of value unlocking.

Suyog fits in this framework very well as the company has grown well and are available at cheap multiples. Over last 5-years, Suyog has grown sales, operating profit and PAT at 21%, 21% and 19% respectively. They generate 25%+ ROICs and have invested for growth, which is shown in their gross block growth of 32% vs sales growth of only 21% in last 5-years. Company is currently trading at 8.7x p/e and 6.3x EV/EBIT, which is quite reasonable for this kind of growth profile. I think there are 4 major reasons behind such cheap multiples:

My rationale for investing is that despite such low ARRs for the telecom industry and consolidation, Suyog has improved margins and grown sales. The sector has seen a lot of stress, and Suyog has managed to tackle this (maybe because of their niche business strategy). If situation improves, there can be a positive delta as company has already done very well in a downcycle, and a couple of their competitors have gone out of business. Lets see how things play out.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

Cyclical (42%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Slow grower (4%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| Suyog Telematics | 1.00% |

While I like deep value strategy you provided, but some of the stocks aren’t that liquid . Taking Shri Jagdamba , ~1800 was volume today . while the price is just 845. Same goes for some more stocks.

Isn’t this a bit of a concern ?

Hi Harsh…

Any change of view about Symphony? If i remember correctly u had told like it would be good buy around 800 levels…As u are tracking concalls too what’s your opinion now as all worst are behind it at present situation

Hi Harsh, Similar boat here. How are you looking at Manappuram now as competition is increasing and we’ve seen the pricing power also eroded to some extent. How do you see growth going forward.

Would love to hear your views.

Cheers

AJ

I buy in chunks, building up positions in a period of 2-3 months. So far, liquidity hasn’t been a problem for me (also given my low capital base).

Yes levels of 850 is generally attractive, however I have been able to find other opportunities where growth is more clearly visible or I have more conviction. Thats why I haven’t bought the stock. But valuation wise, it looks reasonable at these levels.

I do track the company and really admire their execution over years.

I haven’t done anything on Manappuram over the last 6-months. Current valuations are very cheap and I don’t like selling things that are very cheap. The mistake that I made in Manappuram was of not selling last year, when it reached 2.5x P/B and I upgraded my sell price to 3x P/B as I thought growth will continue.

From near term perspective, it seems that quarterly profit run rate of 260-280 cr. should improve given improvement in MFI performance. If I assume a 280-300 cr. quarterly run rate and a 10x exit multiple, exit price should come around 130-140 (assuming business never really improves). Lets see if business ever revives. I am okay holding it for now as the management has turned around the ship multiple times in the past, from crises which were far severe than the current one. Right now, the only problem is in growth due to higher competitive intensity which at some point should normalize. But to add more, I need some visibility on business improvement or more attractive prices (Manappuram reached 0.4x P/B in 2013 downcycle).

Sir any rationale for sticking around with alembic pharma? A good business seems to be in difficult times, so why lose on opportunity cost?

I have found the concept of opportunity cost to be more useful in cos which are trading at very high valuations rather than all time low valuations. When prices have taken a lot of beating, one needs very few upside triggers as there is pessimism already priced in. Let me give some examples from my own investing journey.

ITC: We could have talked about opportunity cost at every point of time until early 2022. All of a sudden, prices moved up when broader markets are flat and made up for a lot of underperformance. Over my holding period, my IRRs have been around 25% in ITC which is because it looked like a value trap for the longest time, and I kept on buying it as underlying business was always solid.

Nalco: When I first created its thread (see below), share prices were at 15 year lows, aluminum prices were at decadal lows and there was gross skepticism around PSUs. It looked like a value trap, but that was only true in hindsight. It was a 4x in 1.5 years, although I could only ride 3x on it.

More recently, I have had a similar experience in Cochin Shipyard. I created my position at a time when it looked like a value trap. Who would have known at that time that in little more than a year, defense would be the flavor of season and Cochin Shipyard has made up for its underperformance at a time when broader markets have been flat.

I have also had very interesting experiences in highly valued cos and how they become a value trap. The whole HDFC family has lost its market fancy and my own IRRs in HDFC triplet (AMC, bank, parent) has taken a serious beating. During my holding period, there was never a time when anyone has doubted their growth, quality or longevity. Luckily for me, I have been able to sell at higher multiples and then buy back at lower multiples.

So its very hard to have the foresight of what markets will think of a company in the future, and trailing 1,3, 5 or even 15 year returns have no impact on future returns.

Now coming back to Alembic Pharma, its a classic cyclical where one can make money by buying through an industry downcycle. Look at EV/sales chart below to see how cheap Alembic is right now.

For cyclicals, the only thing which I have found working for me is to buy pessimism. And during upcycles, one makes their IRRs in very short periods of time. The only caveat is one has to sell in an upcycle (look at how I got stuck in Manappuram because I didn’t sell during the upcycle).

If you get time, read this thread and see examples of cyclicals like Wonderla, Nalco, Indigo, Inox Leisure, Maithan alloys, Ashiana Housing, etc. and how one should be buying through pessimism.

Hope this is useful.

Hello @harsh.beria93

So are you planning to add Alembic Pharma given how cheap it is currently.

Thanks

Brilliantly written. I had similar experience with Indigo, Cochin Shipyard and ITC. However, I have not set up any process around it. I burnt my hands in PNB, KRBL ( but they taught me a lot about investment)

Hi Harsh,

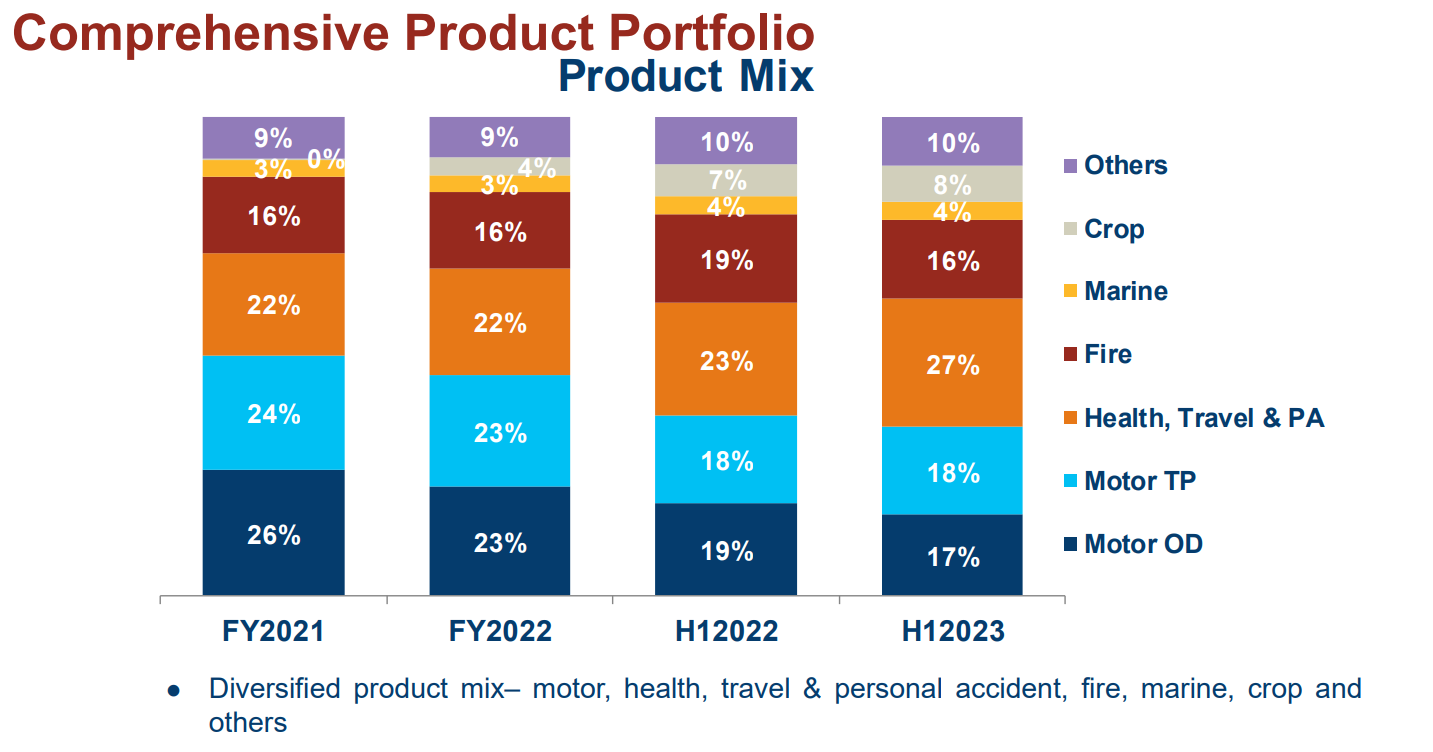

When you exited from ICICI Lombard, you mentioned that IL’s inability to scale Health Insurance segment prompted the call to exit.

As per company’s H1-2023 presentation, Health, travel & PA segment improved to 27% of the product mix vis-à-vis 23% for H1-2022.

GDPI for this segment grew from ₹2015 crore for H1 2022 to ₹2834 crore for H1 2023 (~40% growth). Although, the growth is mainly driven by Health-Corporate segment whereas Health-retail growth is muted and Health-Govt de-grew.

The company is making all the right noises regarding capturing market share in health segment. From the concall-

Within the quarter, we have outgrown the industry and standalone players for the month of September with a growth of 21.1%. This was driven by growth in business sourced through retail health agency vertical of 30.7% in Q2 FY2023.

At the time of writing this post, P/B ratio has further moderated to 5.7.

Given that the interest rates have increased world over and in India, the investment portfolio float is more valuable now than this time last year (ignoring the short term MTM losses).

Does this stock catches your fancy now that the major concern of growth in health segment is resolved, or will be sitting out waiting for P/B to moderate further to 4 as you have mentioned previously?

As you have pointed out, most of health portfolio growth is coming from corporate business which is actually not very difficult to grow (vs growth in retail). However, its still good to see their increasing growth trajectory.

When I had initiated my position in ICICI lombard, it had come down to 6x P/B which based on their past track record was on the lower side. At that time, my rationale was:

A key point of my post was they should maintain 20%+ ROEs for me to pay a premium multiple. After that, in one of the concalls Lombard management had clearly guided they will be investing excess profits to drive growth and wont be maintaining 20%+ ROE in the near to medium term. For a sub-20% ROE business, I was not willing to pay premium multiples especially at a time when HDFC bank was available at 3.5x multiple, and growing at 20%+ rates. I find that logic to be still valid.

When I exited ICICI Lombard, I shifted my money to Sundaram Finance as Sundaram was available at 2x P/B and CV upcycle was clearly visible in monthly nos of CV cos. Below was my rationale:

I find the above logic to be still valid. Since my exit in ICICI Lombard, their price has not done anything while Sundaram has moved up by close to 50%. Now the question is what to do now?

Valuations of Sundaram is still around its longer term means during a CV upcycle. So its fairly valued with potential growth, so I will continue to be invested in Sundaram rather than switching back to Lombard. Lets see how future pans out!

I bought my last chunk in July at 700 and prices are now further down by 20%. One lesson that I learnt from my investments in Lupin was that when things go bad in pharma cos, it takes a lot of time to get resolved.

In some ways, problems faced by Alembic are similar to that of Lupin. Both invested a lot in R&D and capex focused towards US market and then failed FDA inspections. I still have some hope for Alembic as they have failed on inspections towards injectables where they dont have past expertise, so in a way they are learning over time (or that’s what I want to believe). So if they can fix that, there’s a lot of operating leverage possible. Thats why I stay invested, also there is a cyclical recovery play whenever US generics market revive. One thing I like about Alembic is despite all their woes, 70%+ gross margins have been maintained. Lets see how future unfolds.

Very nice analysis…

Just 1 query…

What r your views on Chola invt &Finance vis a vis Sundaram Finance?