Here are my notes from their FY22 annual report.

Miscellaneous

- Target to reach 500 cr. in revenues by FY25

- Ventured into parts for Chassis, Suspension and Steering Components and sub-assemblies for Passenger vehicles & Engine Gears for electrical switch gears and circuit breakers, winches and cranes

- Got major orders for gearing solutions for E-Mobility to local and global customers, all capex investments for parts that go into ICE and EVs

- Bankers: Bank of India, RBL, Citi, IndusInd, Standard Chartered, Yes

- CSR: Spent 40.52 lakhs (out of obligations of 48.66 lakhs)

- Share price: 754 (high), 216 (low)

- Gursharan Singh shareholding went up slightly from 36.54% to 36.57%

- Gursharan Singh attended both meetings of Nomination and Remuneration committee. Ceased to be a member from 12th November 2021

- Advances/loans given to suppliers: 2.13 cr. (vs 1.96 cr. in FY21)

- All loans secured by personal guarantee of whole time directors

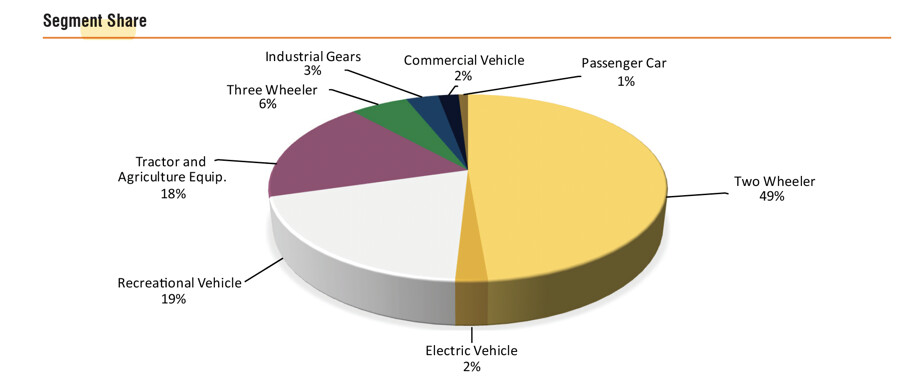

Segment share

Geographical breakup

Imported technology

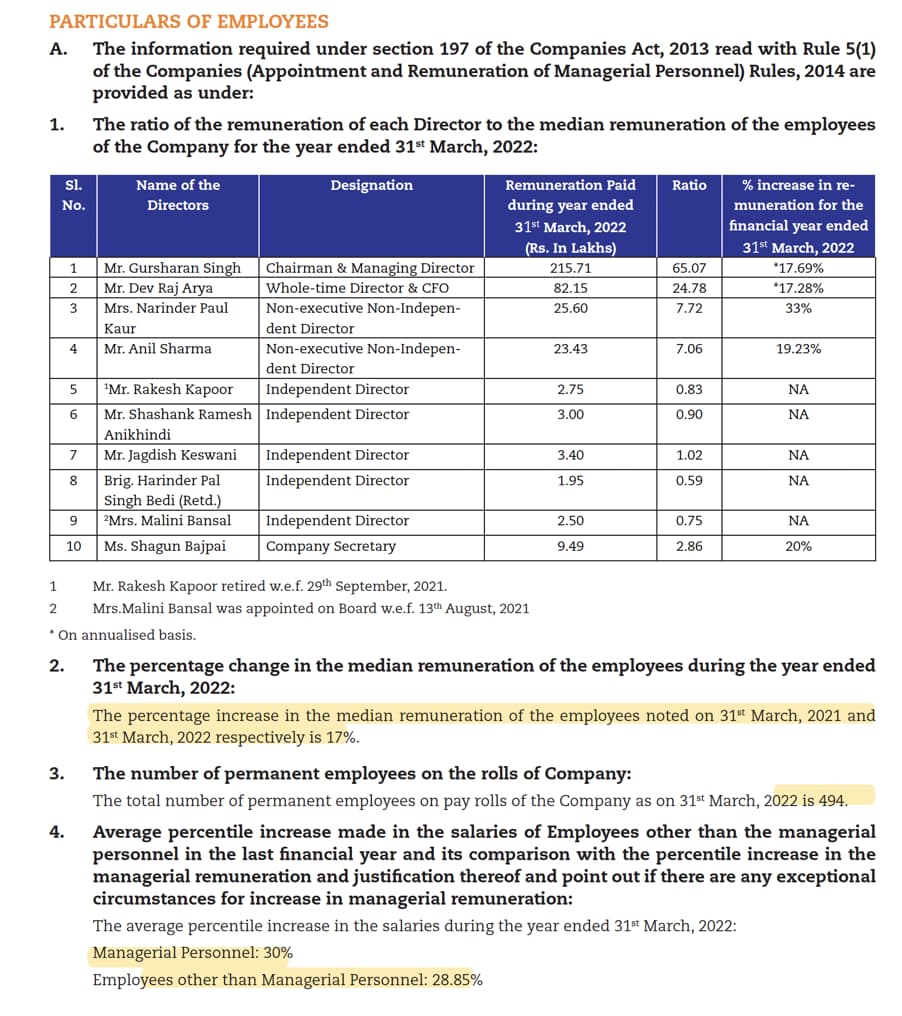

Employee remuneration

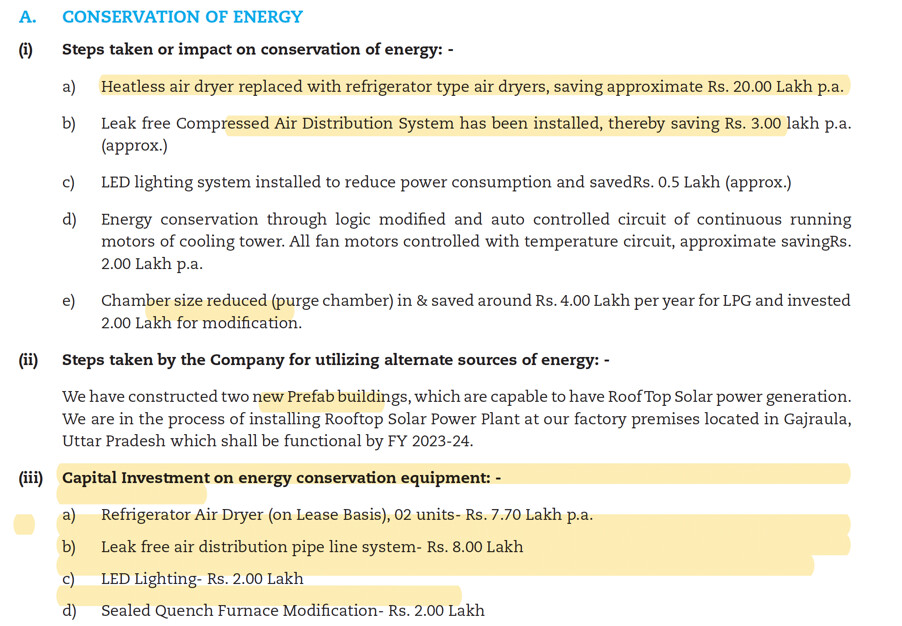

Energy conservation

Disclosure: Invested (position size here, no transactions in last-30 days)