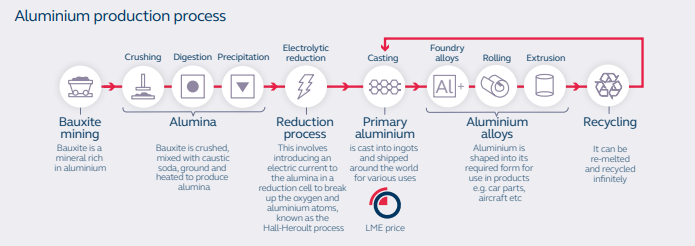

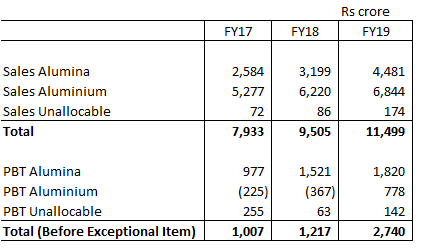

National Aluminium Company Ltd (NALCO) is in the business of manufacturing and selling alumina and aluminum. It is a miniratna company with a government ownership of 51.5% (as of March 2020). NALCO is the lowest cost producer of bauxite and alumina globally. The basic accounting from the last 10 years of financials are shown below.

Accounting:

Over the last 10 years (FY10-19):

- Cumulative CFO ~ 11’948 cr., Cumulative profits ~ 9’821 cr., Cumulative EBITDA ~ 14’227 cr.

- CFO/PAT ~ 122%, CFO/EBITDA ~ 84%

- Cash taxes ~ 4’511 cr., Accrual taxes ~ 4’924 cr.

- Tax as a % of PBT ~ 32%

- CAPEX (maintenance + growth) ~ 6778 cr.

- FCF: 5170 cr. all of which has been paid through dividends ~ 5196 cr.

To summarize, they have been able to convert accounting profits to cash profits. Additionally, the company is net cash positive, generated significant free cash flow which has been paid out to shareholders as dividends (dividend payout ~ 60%). Interestingly, the current market capitalization (5961 cr., 17.04.2020) is only slightly greater than the free cash generated by the business over the last decade. Will we not need aluminum in the future?

Financials

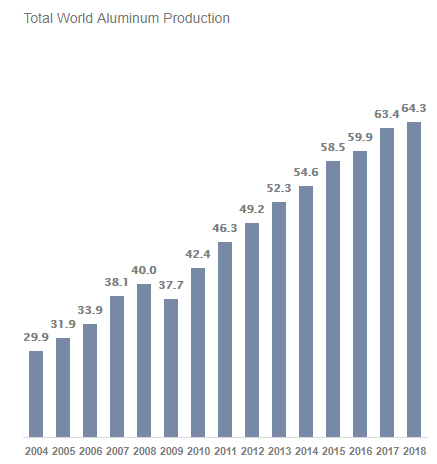

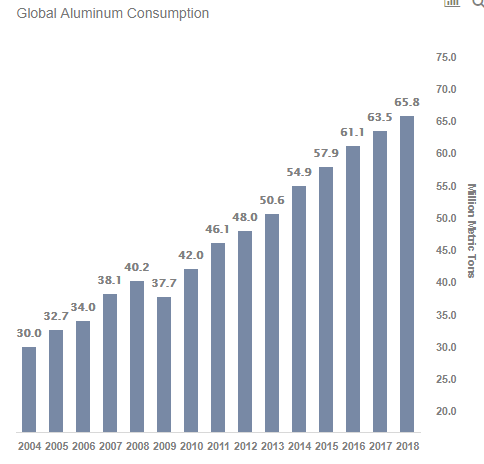

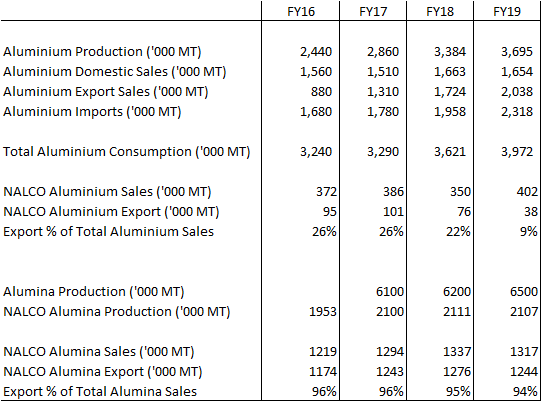

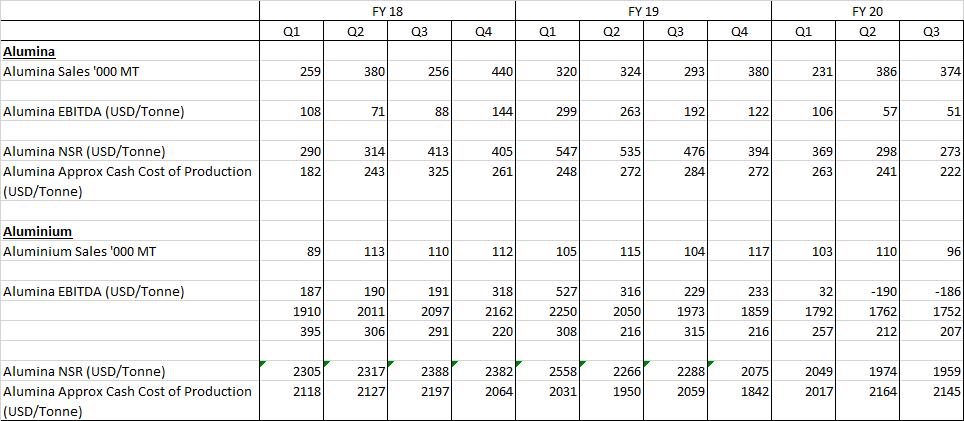

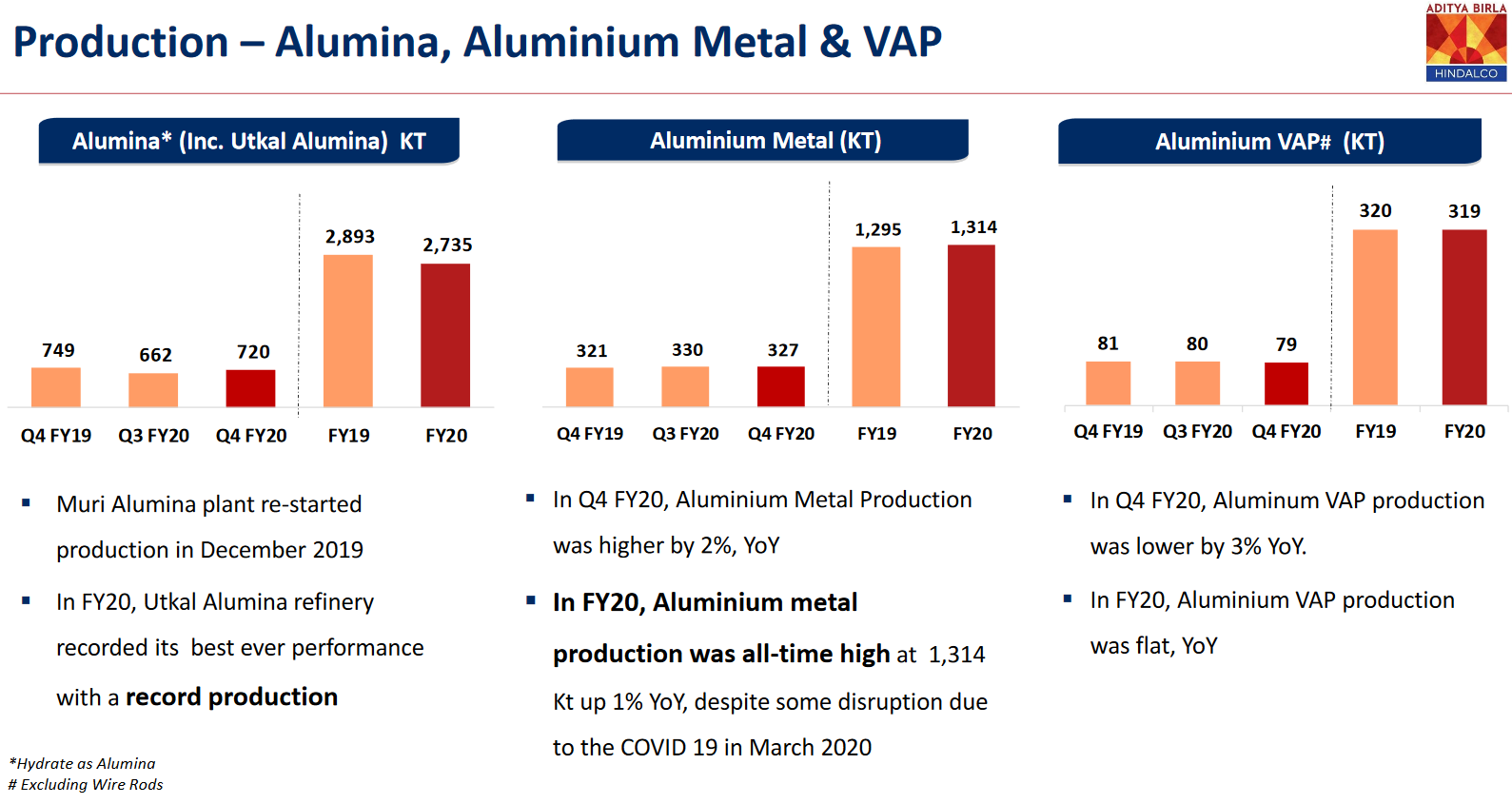

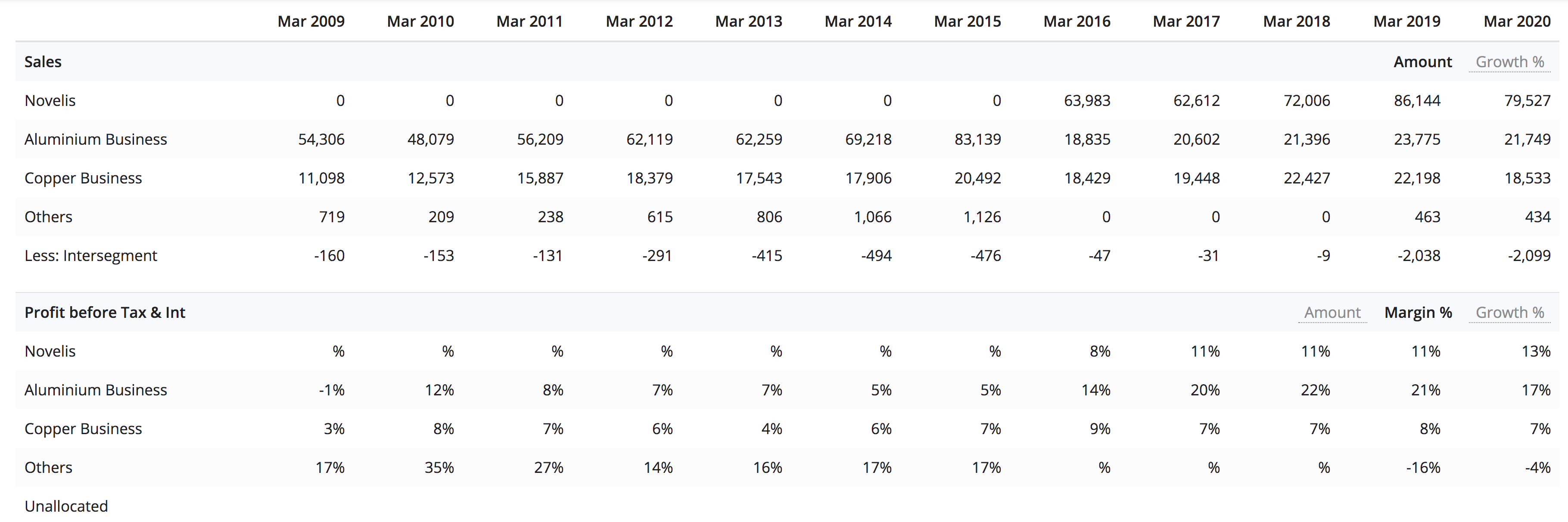

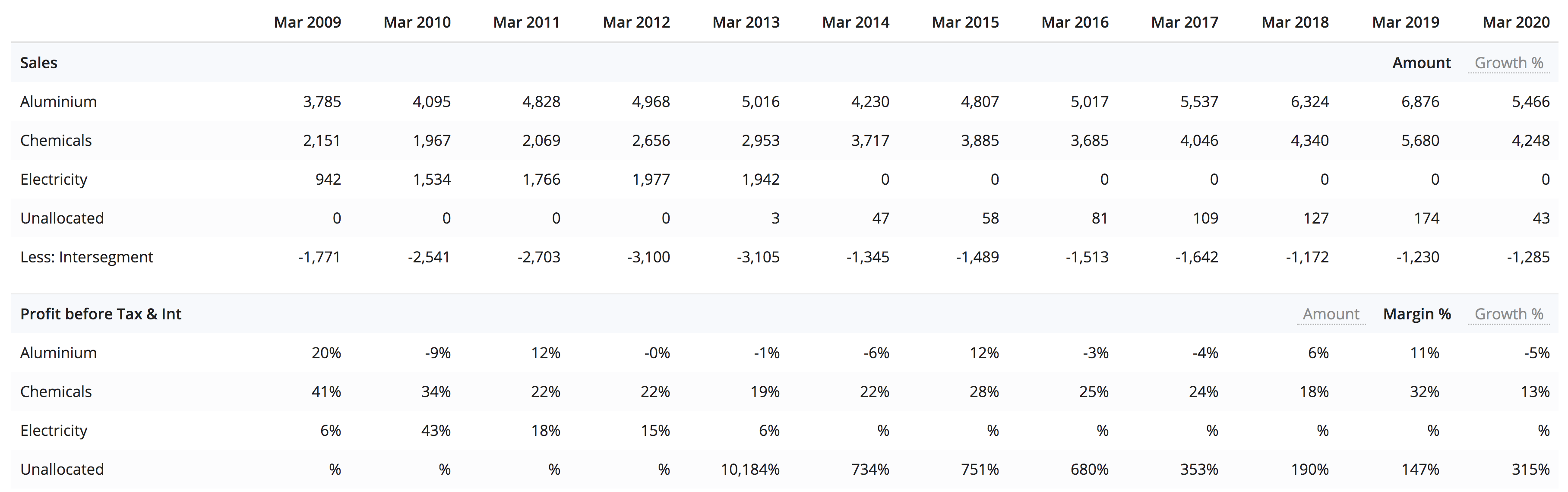

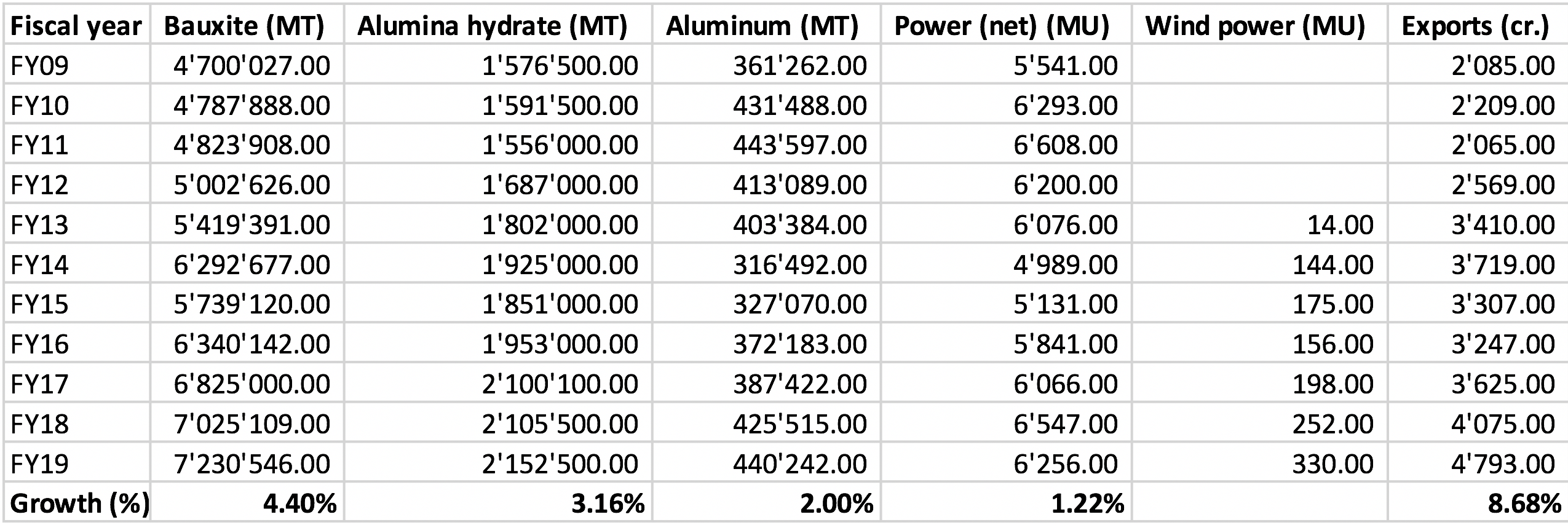

Being a commodity business, their margins are largely dependent on aluminum and alumina prices which are globally determined. In the past, PBT margins have varied between a low of 13% to a high of 28%, with average cyclical margins of 18%. In the past 10 years, the company has faced two major down cycles (FY13-14, FY16-17) followed by upcycles. There is very low bankruptcy risk as the company is net cash positive. Currently, they are in the downcycle with PBT margins going negative in the past two quarters. The bauxite, alumina and aluminum production volumes are shown below. Demand has grown by 3% (by volume) and 8% (by revenue) over the past decade.

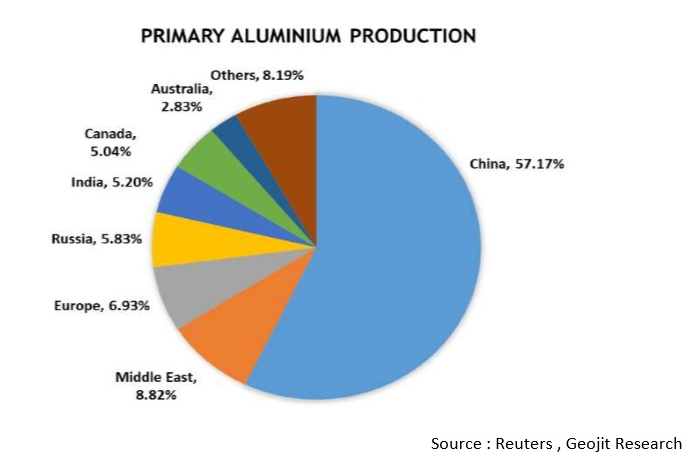

Aluminum demand depends on sectors such as automobile, construction, etc. With the current economic downturn, demand has slowed down significantly. Company also faces threat from cheaper Chinese imports.

Key risks

- Prolonged economic downturn

- Threat of cheaper Chinese imports

- Continuous government selling of shares

- Bidding for mining rights in other countries (example)

- Bribery/scams (example)

- Government capital misallocation

Government has been aggressively bringing down stake in NALCO, bringing their shareholding from 80.93% in FY16 to 51.5% in Q3FY20. As government ownership is down to 51.5%, it leaves very little scope for further selling, as government needs to maintain a 51% stake in order to have ownership control.

Valuations

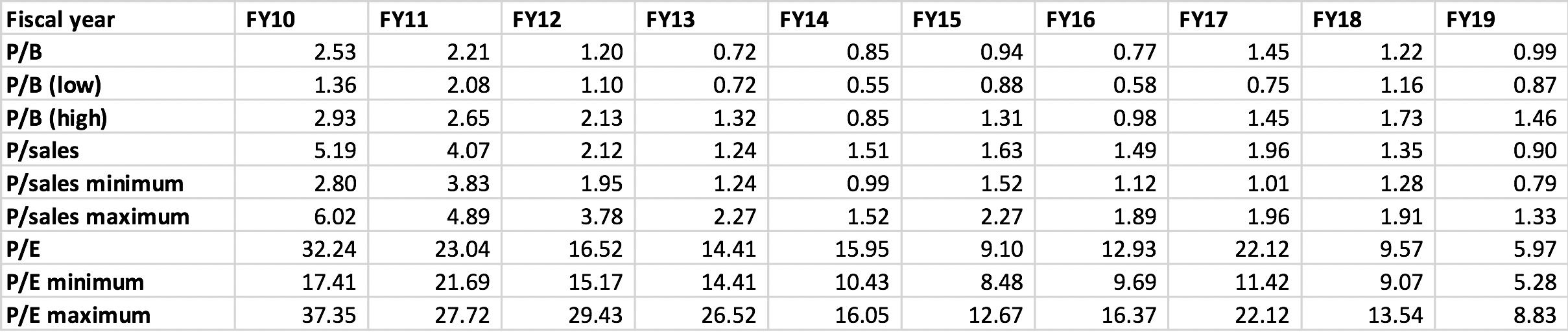

Being a commodity business, margins have to be normalized to adjust for business cyclicality. In order to do this, lets focus on P/sales.

- During the FY13-14 downturn, company traded at a minimum valuation of 1 time P/sales

- During the FY16-17 downturn, company again traded at a minimum valuation of 1 time P/sales

- During the FY10 upturn, company traded at a maximum valuation of 6 times P/sales

- During the FY18 upturn, company traded at a maximum valuation of 1.9 times P/sales

The average P/sales over the last decade is 2.15 times. Currently, the P/sales is ~0.65 which is towards the lower end of its valuations. The company has cash equivalents of ~2800 cr. making the enterprise value ~ 3162 cr. (17-04-2020). The current EV/EBIT ~ 5.78 giving an earnings yield of ~17%. Its definitely undervalued (value trap?).

Crystal gazing

The past aluminum downcycles have lasted ~2 years. Lets assume we get an aluminum upcycle in the next 5 years, the previous upcycle ended in FY19. If the company is able to get back to its peak FY19 sales of 11’500 cr. and average valuations of P/sales ~ 2, market cap will be 23’000 cr., thats a ~285% upside.

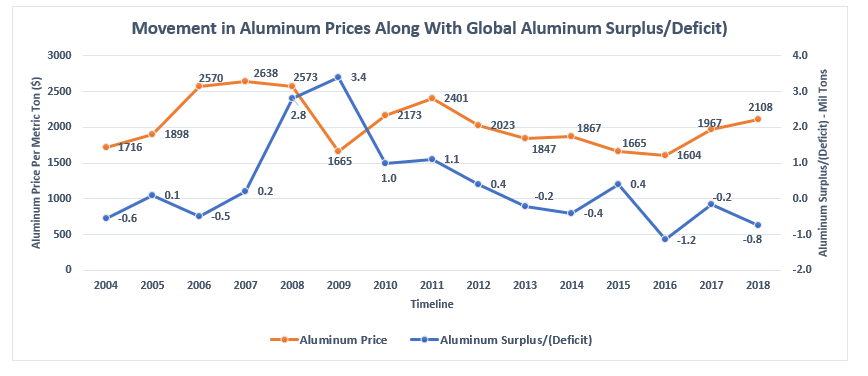

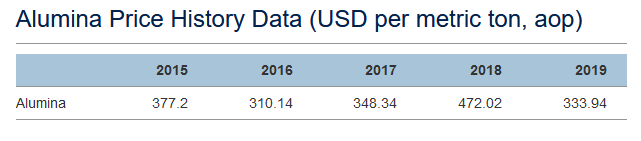

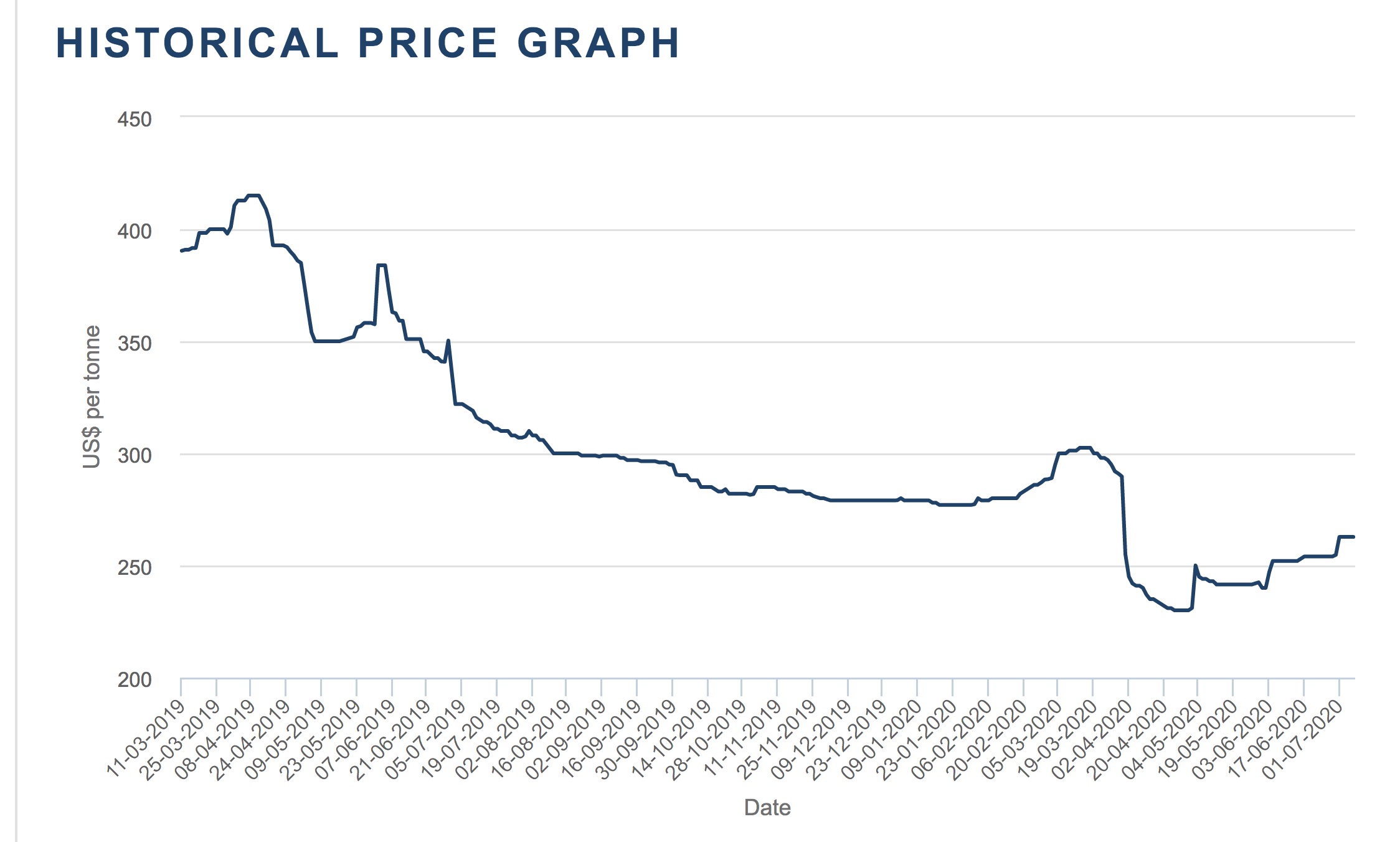

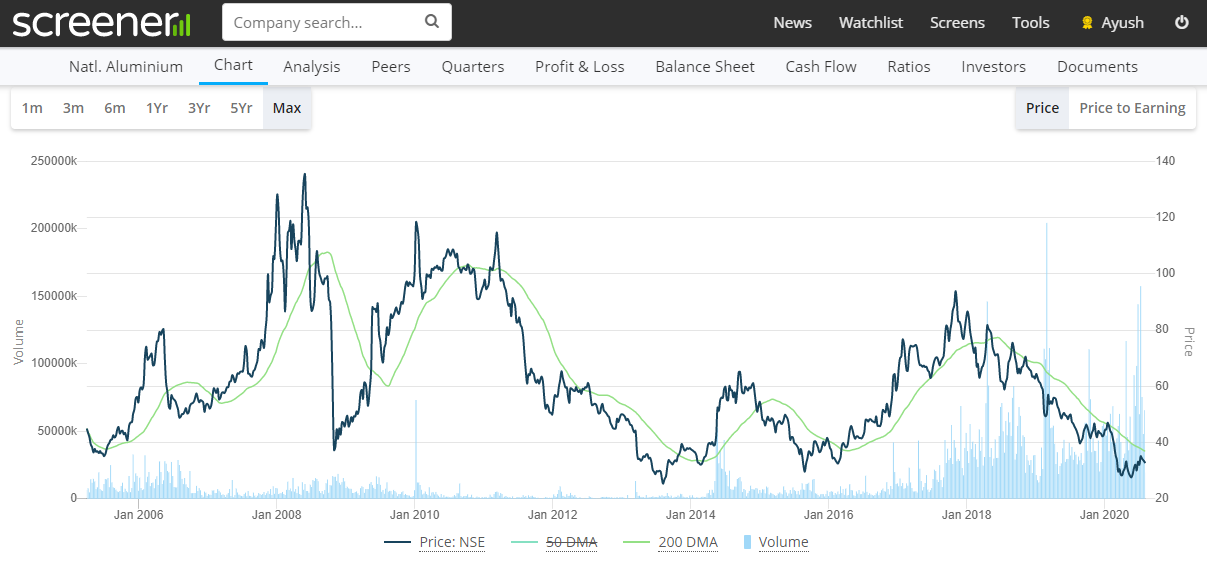

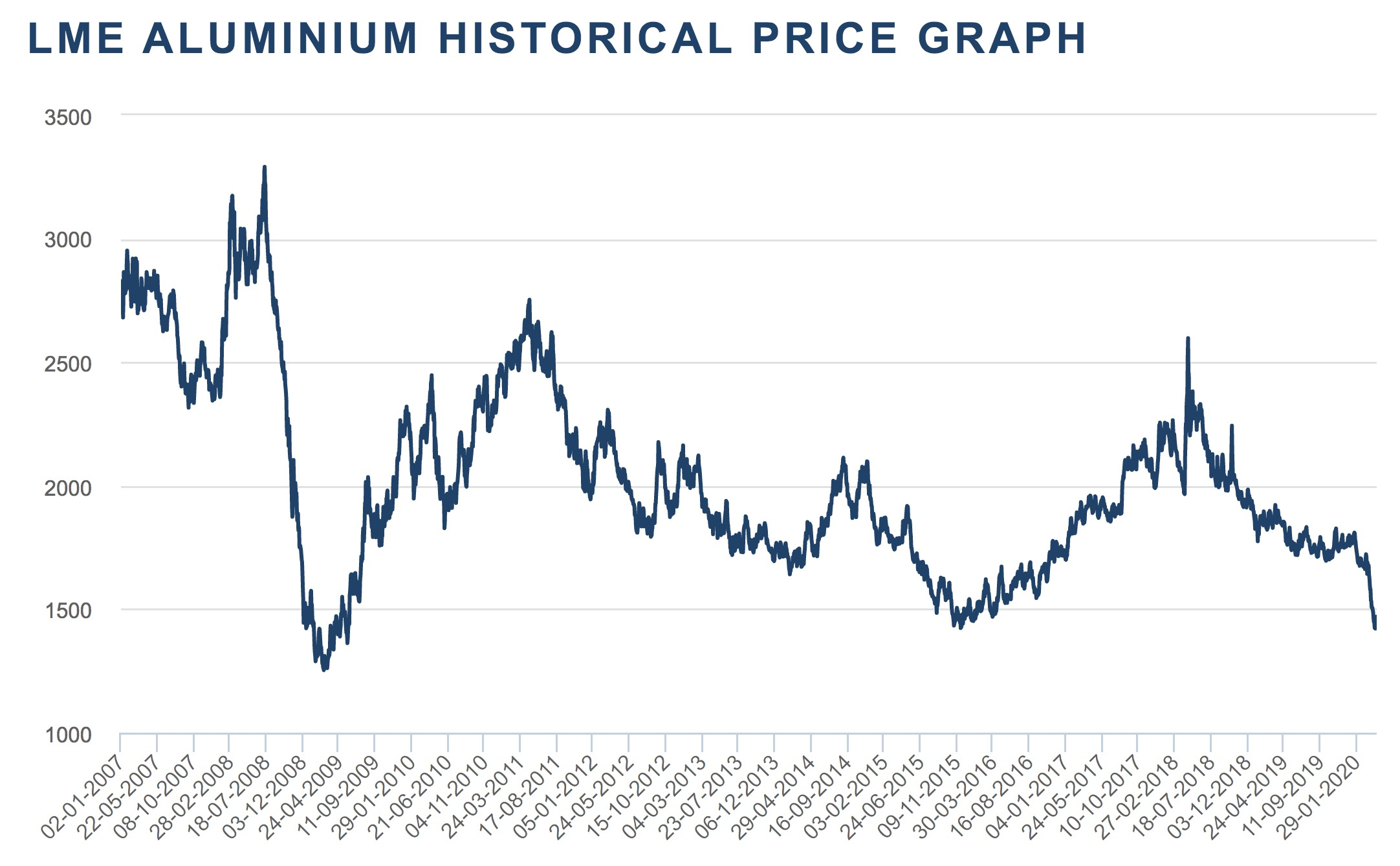

What is the downside? Well the company has almost half its current market cap as cash. It can happen that market cap goes below cash equivalents, as has happened with a lot commodity companies in the past. The share price of the company largely resembles prices of aluminum (shown below).

I would love more feedback.

Disclosure: invested (detailed portfolio here)