Aegis reported decent nos, with most growth coming from rampup in distribution business along with revival in terminalling volumes at other ports. Its interesting to see that company has achieved this growth despite no contribution from terminalling in Kandla port, and 1-month shutdown in Morbi belt. Terminalling volumes in Kandla (which was the base behind this whole stock story) will finally start this quarter, they already have 3 ships booked for this month. Will be interesting to see ramp up in volumes along with more contribution coming from industrial division. Concall notes below.

FY23Q2 concall

- H1 LPG volumes for Mumbai, Haldia, and Pipavav was 14.70 lakh MT vs 13.05 lakh MT, increase of 13%

- Pipavav: LPG jetty work for handling VLGC is expected to completed by Q3FY23 (extended from September 2022). Railway gantry is being used by all 3 OMCs

- Mumbai: Operating LPG at full capacity

- Autogas division: Quarterly volumes declined 14.8% YOY to 5’100 MTPA

- Almost half of Morbi tile cos switched to LPG (propane) from natural gas

- Bulk industrial volumes were 173,990 MT in H1 vs 45,816 MT last year. 35-40% was to Morbi. This was despite 1-month shutdown in Morbi

- Commercial and domestic cylinder volumes were 17,310 MT vs 11,352 MT last year

- Aegis makes 2,000–2,500/ton margins on bulk industrial volumes (through trucks) to Morbi customers. They make 4,000/ton margin for industrial distribution segment done through cylinders. Blended retailing margins are 3000/ton

- Total sourcing tender volume contracts for CY22 was 800’000 MTPA. They did volumes of 457’960 MT vs 159’633 MT last year

- H2 is generally stronger than H1

- One-time special dividend of Rs. 2 celebrating JV transaction

- 7 cr. profit was accrued to minority interests. Focus is on growing EPS of the company

-

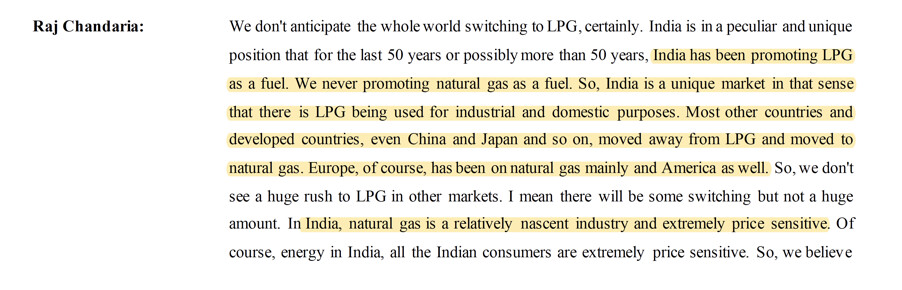

LPG vs CNG in Indian context

Kandla:

- No terminalling volumes yet. Started receiving ships with 3 ships being unloaded this month which will start terminalling volumes

- Jetty 7 is expected to become VLGC-compliant by FY23 end

Haldia:

- Lower volumes because of upgradation of both jetties

- Liquids capacity of 50’000 cubic meters will be commissioned in FY23

Disclosure: Invested (position size here, no transactions in last-30 days)