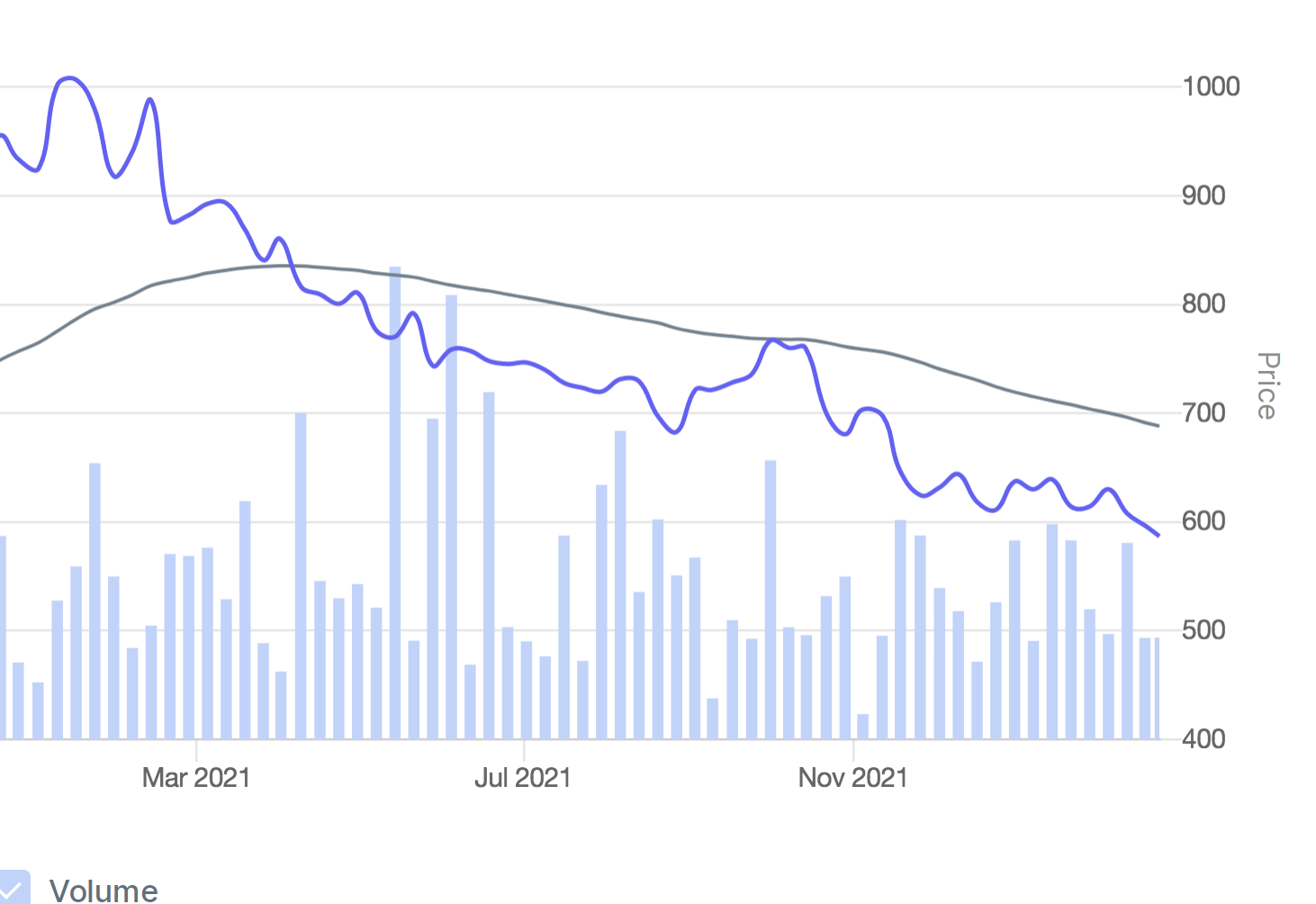

I had an interesting discussion with @Rafi_Syed about Amara Raja and am trying to capture the same on VP. Prices have gone down by 40%+ from a peak of ~1000 in January 2021.

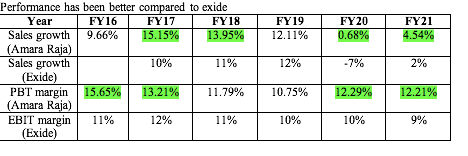

That was also the time of peak operating margins, since then margins have come down (for both Exide and Amara Raja) due to increase in lead prices.

They also ran into environmental compliance problems starting in Q4FY21.

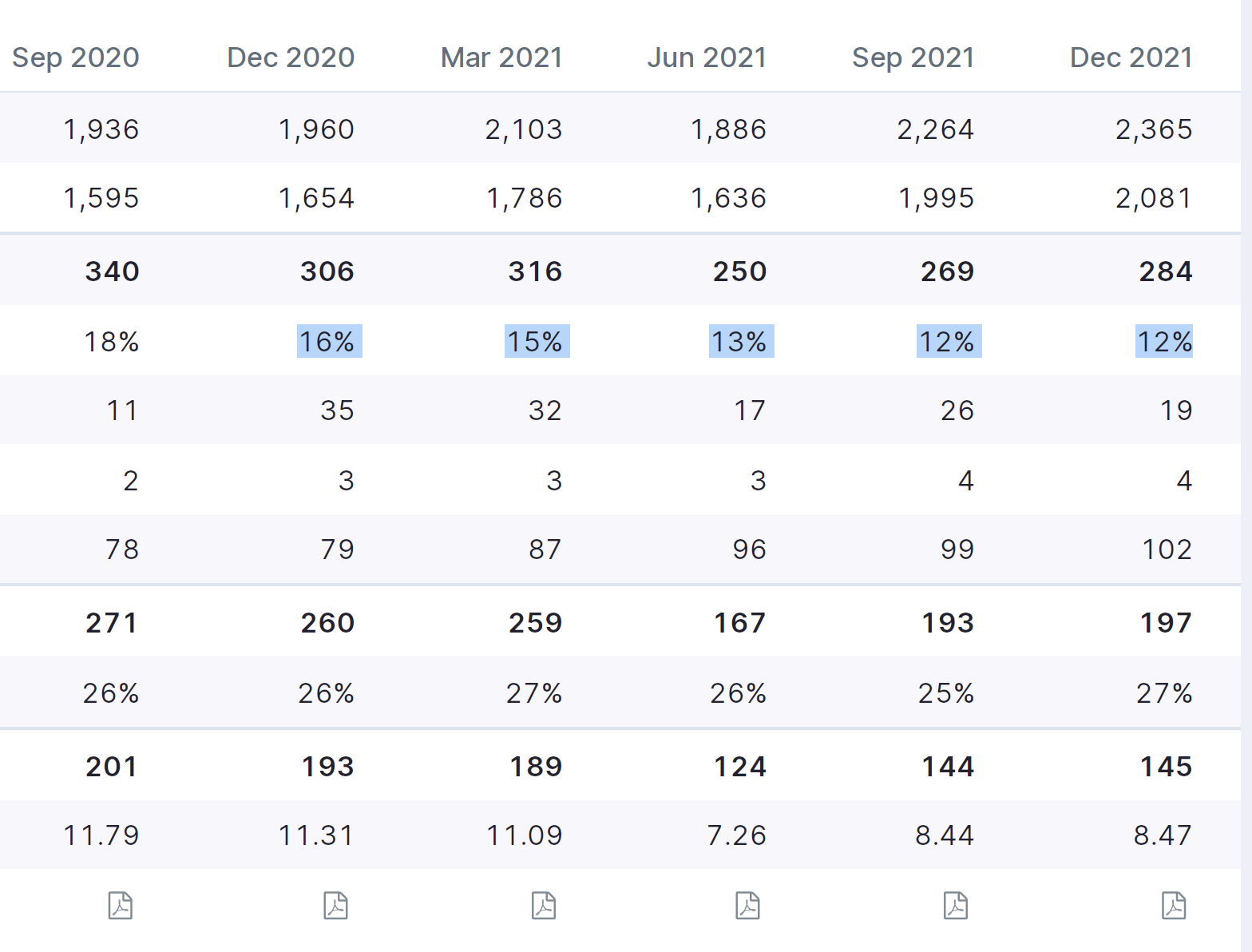

All this being said, they are trading at ~16x P/E on trailing profits (which are depressed due to cyclical low margins). On a normalized PAT margin of ~10%, they are trading at ~11x P/E.

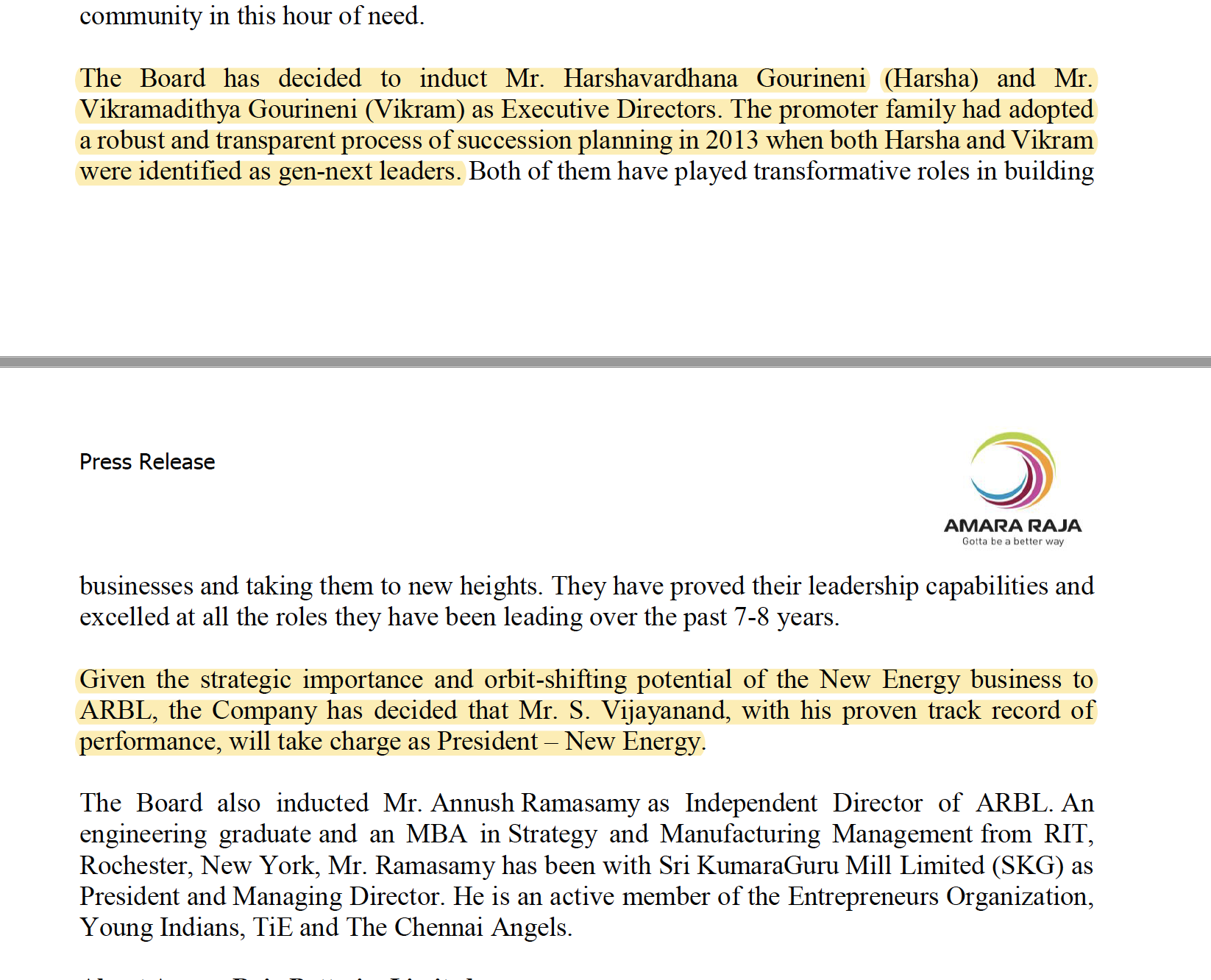

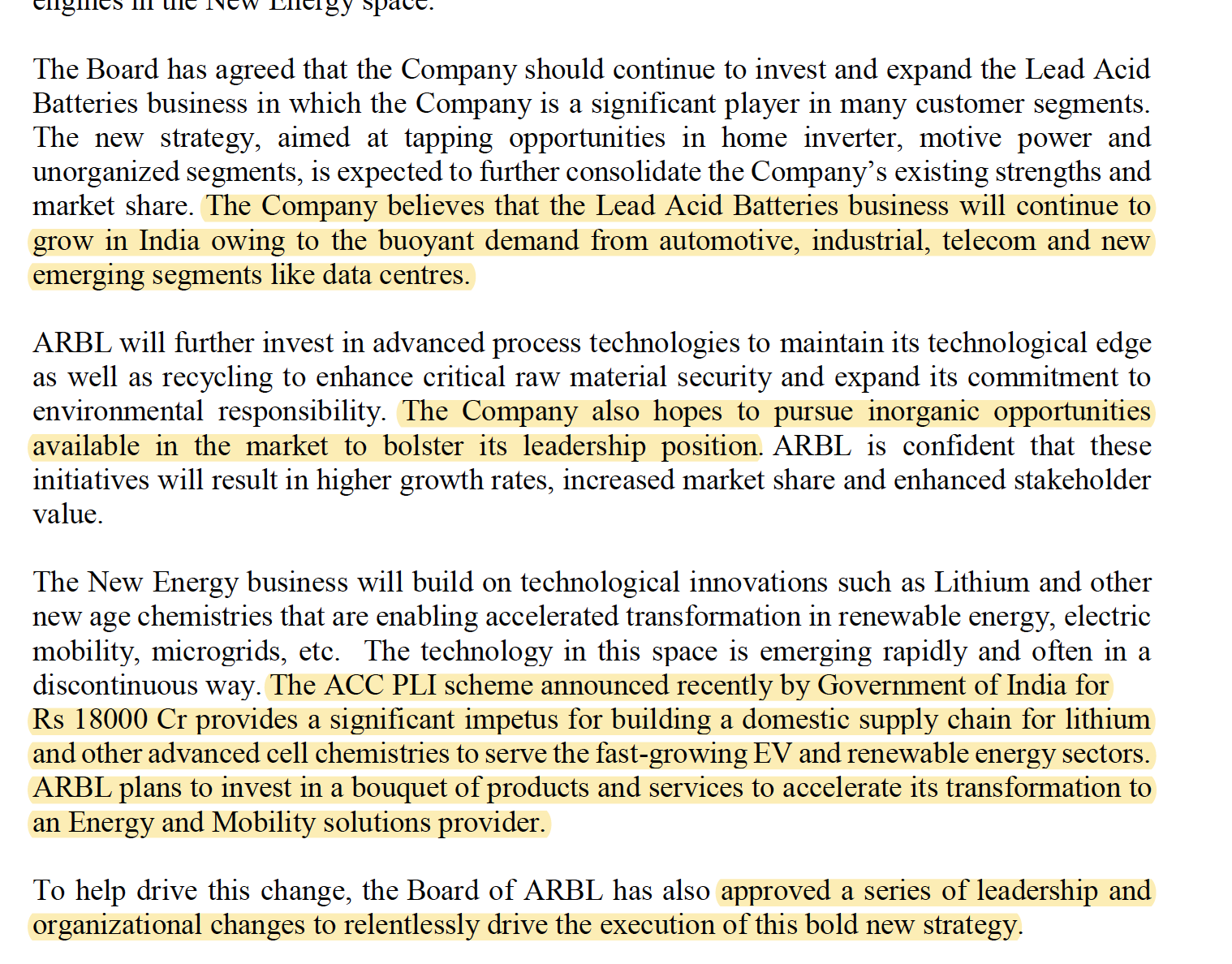

Also, the next generation has been inducted in leadership roles and are prioritizing investments in lithium ion batteries.

Comparison with exide: Growth and margin performance has been better than Exide.

During the cyclical auto downturn, they managed to grow sales and profits.

So it seems company is investing in future technology, gaining market share and trading at reasonable valuations. A cyclical uptick along with a resolution of their compliance problems can benefit company’s performance. Key risk remains the high level of investment required in building lithium ion capabilities which will hamper free cash generation.

Disclosure: Invested (position size here)