Punjab came up with very good sales growth of 33%, but margins were stressed due to RM inflation and higher power costs. Management remains confident of strong growth and are guiding for 1100-1150 cr. of sales in FY23, and 1500 cr. in FY24. My concall notes are below.

FY23Q2

- Headwinds in business environment, have adopted flexible approach in product pricing (to increase market share) and are focusing on new geographies such as South America

-

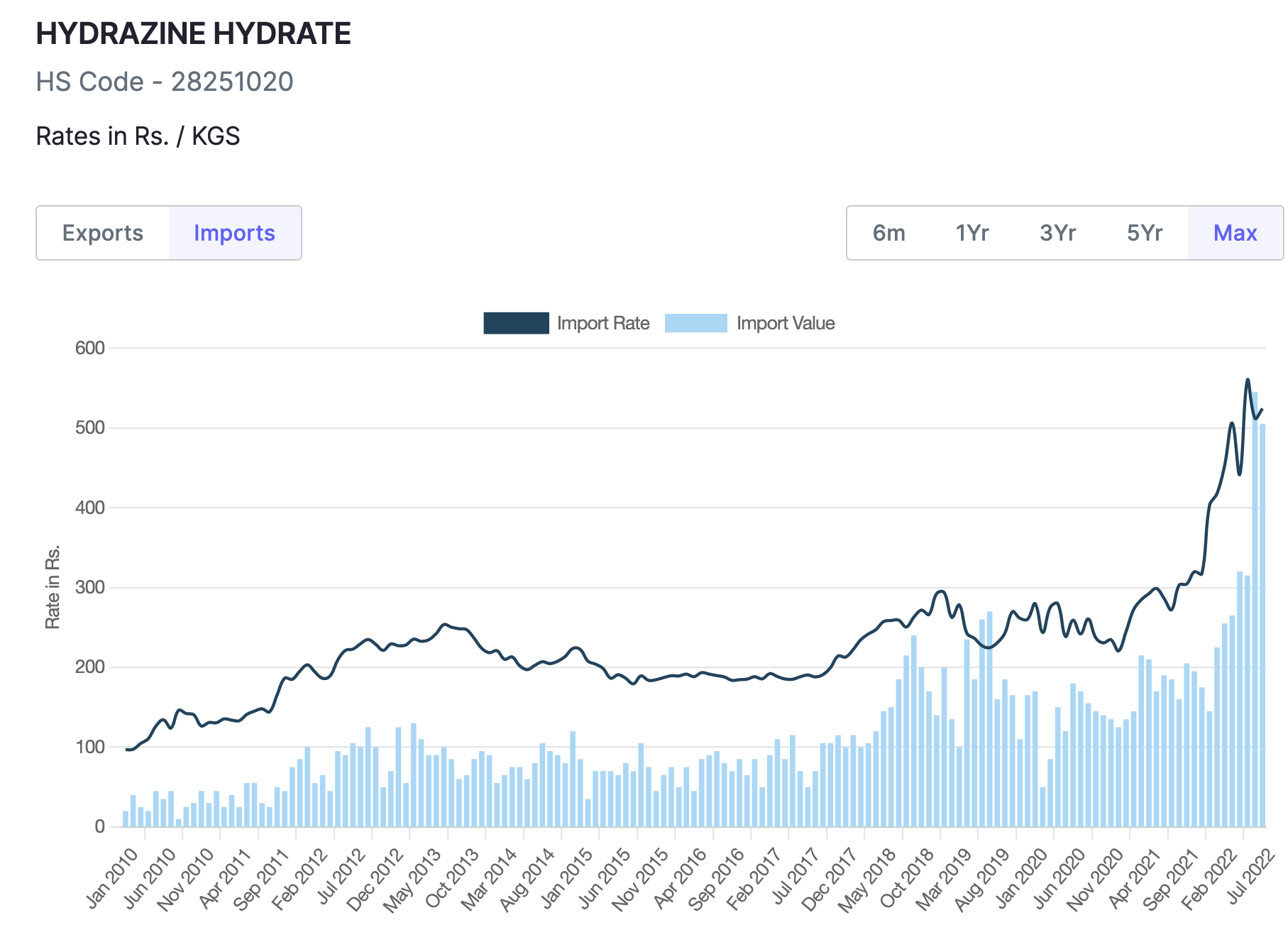

Margins: pricing pressure, product mix, carry over of high cost inventory from earlier periods (mainly hydrazine hydrate). Energy, fuel (rice husk; gone up) and freight costs impact other expense. Will be able to pass on cost pressures by Q4 and revert to 14-15% EBITDA margin

- Hydrazine hydrate prices have started tapering off

- Power costs (60 cr. in FY22 vs 32/33 cr. for IPL/Bharat Rasayan): Products (herbicides) are more power intensive + due to farm law changes in last couple of years, availability of rice husk has become a challenge

- Investing in renewing assets that are 30-40 years old (should have replacement capex of 30-40 cr. over 2-years)

- Lalru: facing raw material problems resulting in lower production and delay in registration. Hope to come back to 70%+ utilization in Q3/Q4. Large part of CRAMS business comes from Lalru, and majority of expansion will also happen here

- Derabassi: mature products, debottlenecking

- Order book: has increased from 1500 cr. to 2500 cr.

- Looking for a new site in Maharashtra or Gujarat and should finalize by end of FY23

- Lot of customer visits happening from multiple geographies (Japan, Israel, etc.)

- Phosphorus derivative: Faced pressure in this division due to pressure from Chinese suppliers. Have seen large margin drop, should see it come back to 16-18% next year

- Have seen some slowdown in demand from domestic market

- Agri segment has seen significant growth in South America

- 15%+ volume growth. Maintain 1500cr. revenue by FY24

- Thiocyclam: Full potential of this product has been delayed due to registration an should be realized in FY24

- Singapore customer molecule (most likely prosulfocarb): Registration has been delayed and growth should come in FY24

- Capex: 120-150 cr. over next 2 years

- CRAMS: 65%; 40% from generic molecules + 25% from tech transfer of 2 molecules from Japanese customers + 1 more. Are either first or secondary supplier in CRAMS business. Have quarterly review on forex adjustements

- FY23 sales will be 1100-1150 cr.

- 60-65% CRAMS + 15% specialty chemicals + 15-20% intermediate & fine chemicals. On spot basis, sales are very low (maybe 5%)

- 2 new products coming in agro + 1 in specialty chemical in FY24

- Making intermediates for Israeli company specializing in fermentation space (most likely NextFerm Technologies). It’s a small high margin business

Disclosure: Invested (position size here, bought shares in last-30 days)