I have made the following changes to the model portfolio:

- Reduced position size in Cochin Shipyard from 4% to 2%

- Reduced position size in ITC from 8% to 4%

- Created 2% position in Godfrey Phillips

- Created 4% position in Chamanlal Setia

So cash continues to be zero in the portfolio.

Drop in position size in Cochin Shipyard is due to rerating in the co from 7x PE a few months back to 14x now. When I had initially written about the company last year, I had asked the question “Will it ever become a growth stock”? If it reaches 20x earnings, I will say yes and sell.

Over the last 5-6 years, I have seen that the easiest way to make money is to buy good dividend paying cos at 5%+ yield (sustainable and not due to one-time things) and simply hold it until market gets excited about it. In this category, I have made gains in cos like Powergrid, ITC, SJVN, Cochin Shipyard. Another company which fits this criterion is PFC, but somehow I could never pull the trigger as its a leveraged play. Currently, I am looking to add Petronet LNG in this category of stocks.

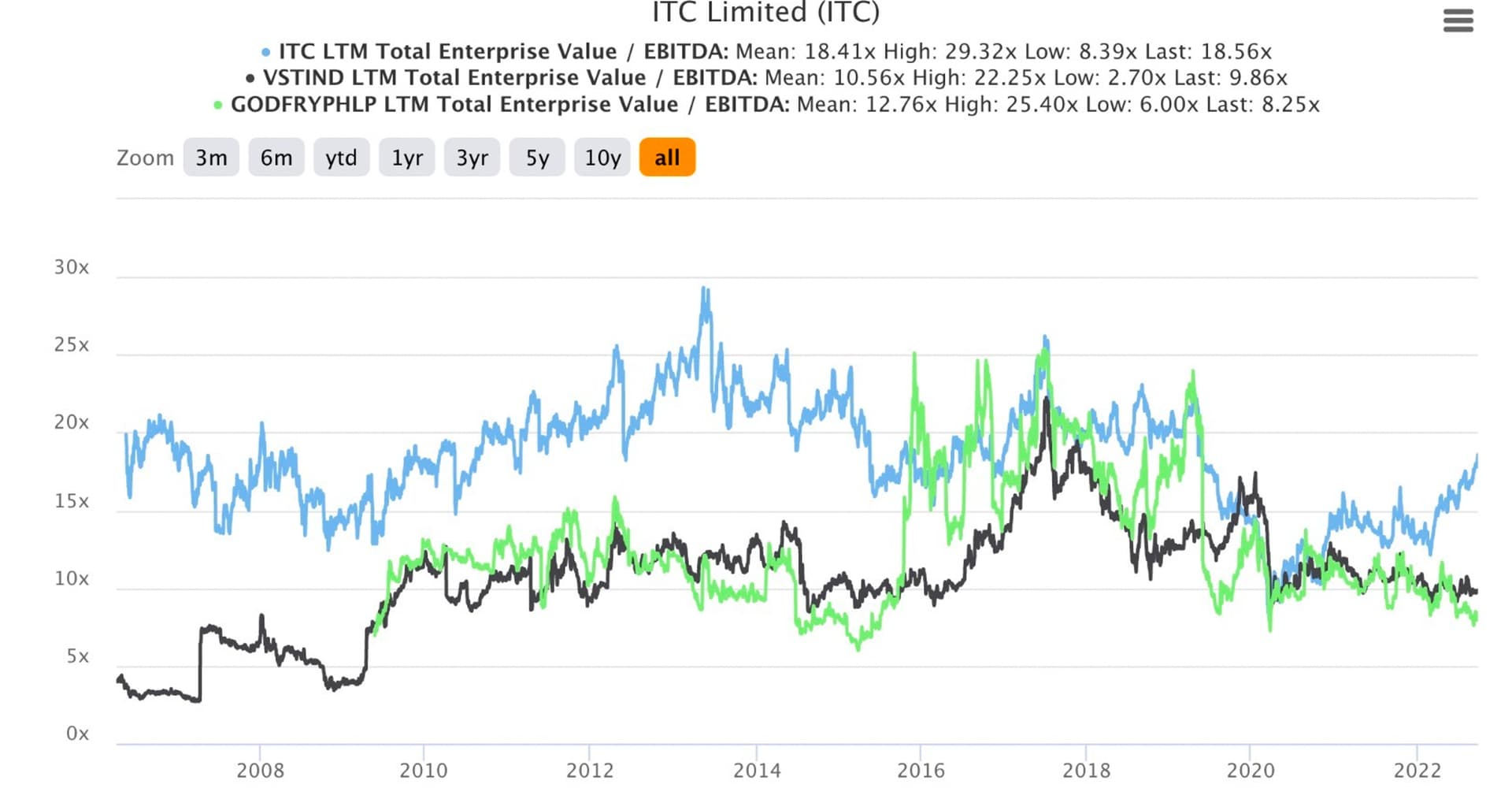

ITC has tested patience over a period of time, but it has been very rewarding. In terms of rupee value, I have made the maximum gains here and the IRRs have now reached 26%, which is why I have started reducing the position as there are better opportunities available (such as Godfrey Phillips).

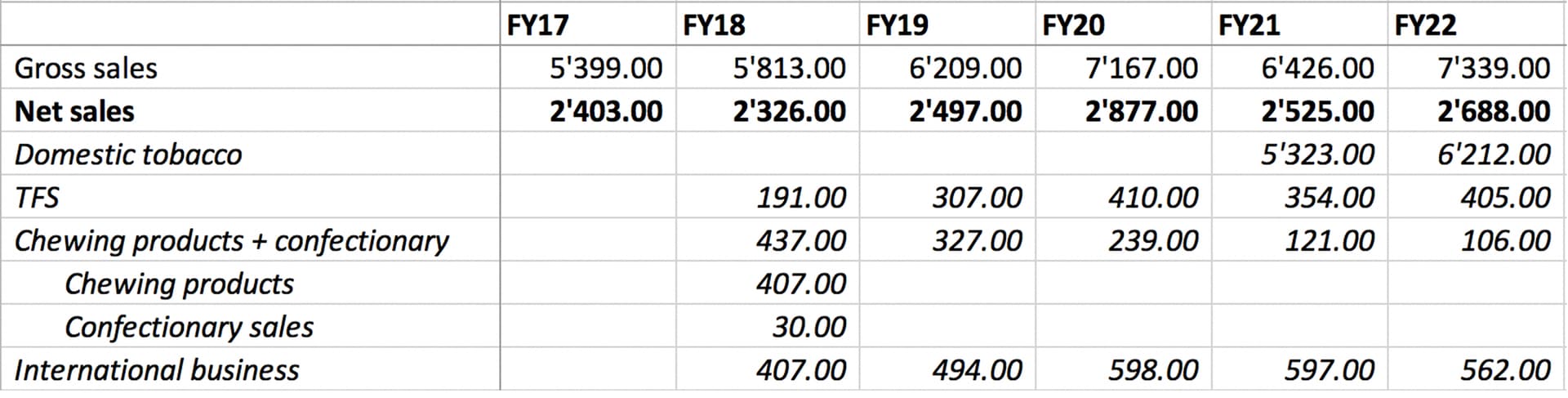

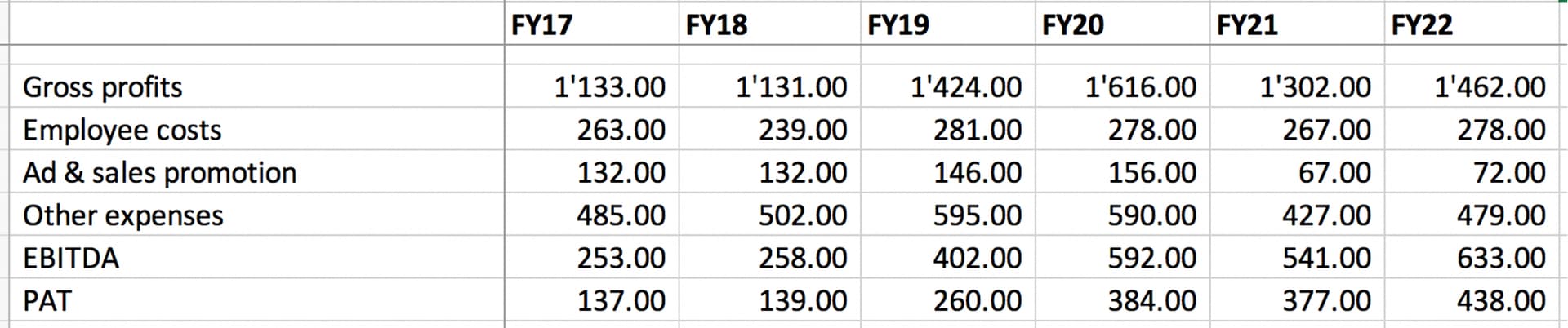

I have already written about Godfrey Phillips in the previous post, so I will not repeat the thesis. The basic idea is fast growth and reasonable valuations.

Chamanlal Setia is a basmati trader and has better return metrics vs market lead KRBL, and has also grown at higher rates, despite being in a sector often plagued by debt issues. Every 4-5 years, Chamanlal seeds a new market or a new set of customers, which results in 50%+ sales growth (FY14, FY18). In the next couple of years, they work on improving margins.

FY23 is another year which will show 50%+ sales growth. I expect margins to revive in the next couple of years, leading to a large delta in earnings. Its attractively valued even on trailing earnings where margins have been subdued (7.5x earnings, 3.5x EV/EBIT). So, I expect good growth in earnings in next few years, and hopefully some rerating.

Updated portfolio is below.

Core compounder (42%)

| Companies |

Weightage |

| I T C Ltd. |

4.00% |

| Housing Development Finance Corporation Ltd. |

4.00% |

| NESCO Ltd. |

4.00% |

| Eris Lifesciences Ltd. |

4.00% |

| Ajanta Pharmaceuticals Ltd. |

4.00% |

| HDFC Asset Management Company Ltd |

4.00% |

| Aegis Logistics Ltd. |

4.00% |

| Gufic Biosciences |

4.00% |

| HDFC Bank Ltd. |

2.00% |

| PI Industries Ltd. |

2.00% |

| Shri Jagdamba Poly |

2.00% |

| LINCOLN PHARMACEUTICALS LTD. |

2.00% |

| Godfrey Phillips |

2.00% |

Cyclical (46%)

| Companies |

Weightage |

| Kolte-Patil Developers Ltd. |

4.00% |

| Sharda Cropchem Ltd. |

4.00% |

| Avanti Feeds Ltd. |

4.00% |

| Aditya Birla Sun Life AMC Ltd |

4.00% |

| Alembic Pharmaceuticals Ltd. |

4.00% |

| Amara Raja Batteries Ltd. |

4.00% |

| Chaman Lal Setia Exp |

4.00% |

| Ashiana Housing Ltd. |

2.00% |

| Ashok Leyland Ltd. |

2.00% |

| Heranba Industries |

2.00% |

| Kaveri Seed Company Ltd. |

2.00% |

| Control Print Limited |

2.00% |

| Sundaram Finance Ltd. |

2.00% |

| Time Technoplast Ltd. |

2.00% |

| RACL Geartech Ltd |

2.00% |

| Manappuram Finance Ltd. |

2.00% |

Slow grower (2%)

| Companies |

Weightage |

| Cochin Shipyard Ltd. |

2.00% |

Turnaround (4%)

| Companies |

Weightage |

| Punjab Chem. & Corp |

4.00% |

Deep value (6%)

| Companies |

Weightage |

| ATUL AUTO LTD. |

1.00% |

| Jagran Prakashan Ltd. |

1.00% |

| D.B.Corp Ltd. |

1.00% |

| Shemaroo Entertainment Ltd. |

1.00% |

| Modison Metals |

1.00% |

| Suyog Telematics |

1.00% |