Hi @harsh.beria93 Yesterday Samir Jasuja the proprietor of P.E analytics offloaded some of his shares. Is it something you would be concerned about?

Hi Harsh,

What’s ur view on the ongoing legal battle of Godfrey Phillips promoters : -

It vl be good for the biz if the dispute settles either way bt as these cases drag - wont that remain an overhang on the stock?

Disc :- Not invested. I sold this positn after 2X in Nov’23

I have made a few changes to the model portfolio which are summarized below. My thought process at this point is to reduce allocations to stocks trading at higher end of their valuation band, and also reduce allocation to very small cos, especially without any clear triggers. Market has been excessively rewarding, and in the past my major mistakes have come in these times. Lets see how many mistakes I make in this cycle.

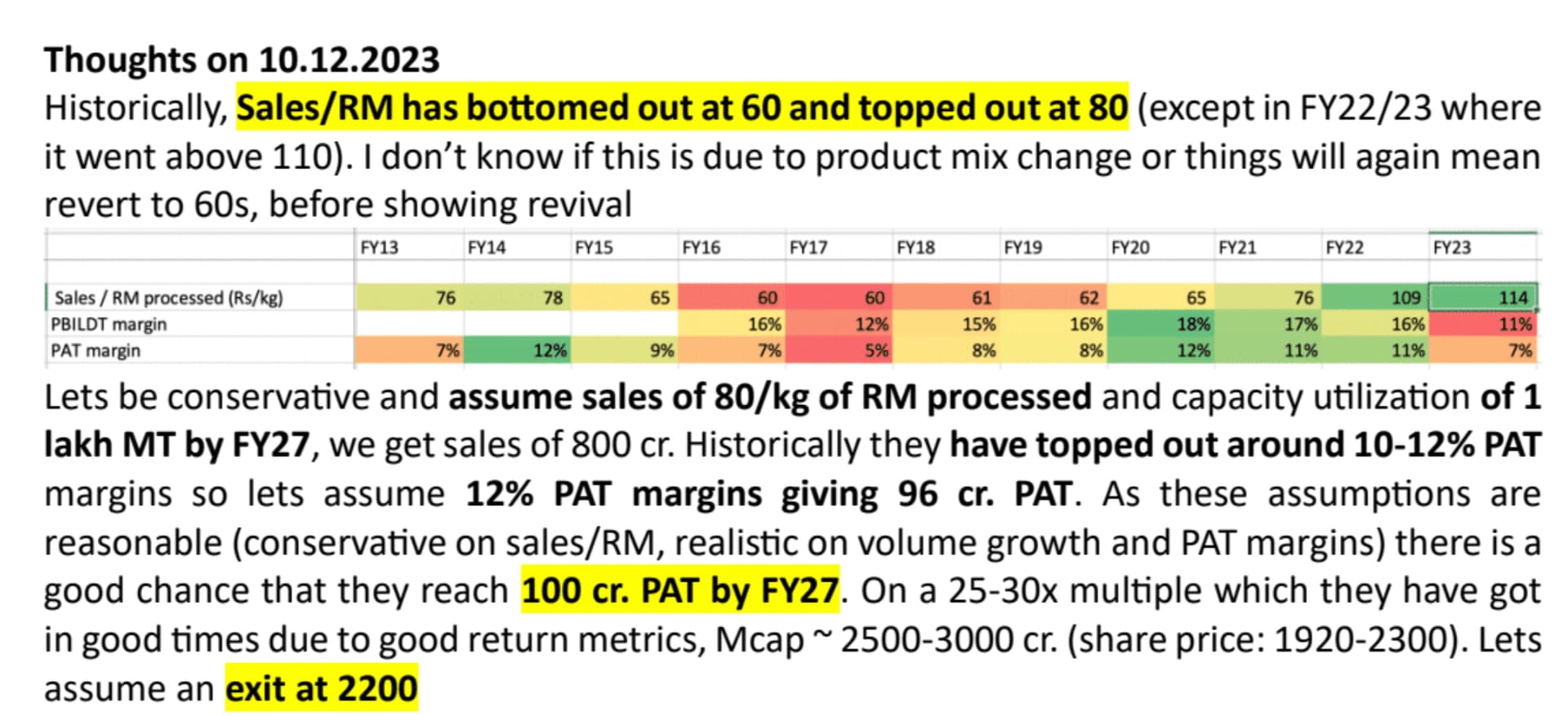

- Added 2% allocation in Fairchem Organics. I am looking to add chemical companies which have done capex, have good unit economics, and whose prices are down a lot. In Fairchem, logic is quite simple. Their new product (stearic and isostearic acids) are 2.5x realizations vs Dimer acid, has limited competition, and a large market size. Fairchem’s margins are at life lows. So there are two clear earning drivers (mean reversion in margins + new product growth). I feel they can reach 100 cr. PAT over the next 3-4 years. My detailed speculation around their future nos are below.

-

Added 2% allocation in Garware hi-tech. Garware’s VP thread is amazing to understand what differentiates them vs other packaging/polymer cos. Their PPF scaleup has been quite good and I feel if they can reach 2,500 cr. sales/ 500 cr. EBITDA by FY27, they will get atleast 10,000 cr. Mcap. I somehow missed buying it last year when their valuations fell to 10x, but I still feel there is good potential from current prices.

-

Increase allocation to Manappuram from 2% to 4%. I should have added to it when price had dipped below 100 but somehow failed to act. Business is clearly recovering and valuations are quite cheap. The Asirvaad IPO should also create some excitement around the stock. I feel its one of the best, yet one of the most misunderstood managements. Their capital allocation and scaleup since 2015 has been spectacular. @maheshkumar does an amazing job in sharing everything there is to know about the co.

-

Reduced allocation to Gufic biosciences, from 4% to 2%. Their stock price has moved up significantly in anticipation of growth from their large capex, as a result Mcap/sales is towards the higher side. I want to reduce my risks here.

-

Exited newspaper companies (DB Corp, Jagran). The idea of mean reversion in valuations is so simple, yet somehow unloved. Since I invested in 2021, DB Corp has returned 20% of my initial capital as dividends, and share price is close to 5x. Jagran has been a bit disappointing vs DB Corp, but it has been reasonable (7% dividend + 2x price). I am unwilling to pay 20x PE for slow growth newspaper cos like they are valued now. But single digit multiples on depressed earnings is something I am happy to bet on, especially because these companies are paying out earnings to shareholders.

-

Exited CV cycle plays (Ashok Leyland, Sundaram Finance). Both have been very rewarding but recent CV sales data suggests some slowdown and I am unwilling to go into a bad market with CV companies at their top.

I find that cyclical and value investing jells very well with my personality, its possible to make 3-5x by buying into a bad cycle and waiting for recovery. CV cycles are really predictable and one can make good returns by just betting on leaders during downcycles. E.g. I started buying Ashok Leyland in 2020 when its price had dipped below 50, since then it has been a decent journey.

Sundaram Finance is a CV lender with an amazing track record, and it got sold in 2022 and reached cyclical low multiples. One could see CV revival in monthly sales data, and it was a 2.5x in quick time, despite being a leader and being well followed. However, valuations now are closer to their upper end, thats why the exit.

Updated folio is below and cash stays low at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| Aegis Logistics Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Godfrey Phillips | 4.00% |

| P.E. Analytics Ltd | 4.00% |

| Gufic Biosciences | 2.00% |

| Ajanta Pharmaceuticals Ltd. | 2.00% |

| NESCO Ltd. | 2.00% |

| I T C Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 2.00% |

| Garware Hi Tech Films Ltd | 2.00% |

Cyclical (45%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| Chaman Lal Setia Exp | 2.00% |

| Fairchem Organics Ltd | 2.00% |

| KSE LTD. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (8%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Worth Peripherals Ltd | 2.00% |

| Sharat Industries | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

Its called Pareto chart, you can find it on excel.

No idea, sorry these are too complicated concepts for me.

Dont know how to think about these things. Promoter selling in isolation doesn’t provide any insights.

There is a lot of buzz that finally the battle will settle this year. For the kind of nos they are reporting, current prices are capturing a lot of downside already. But I dont know how to think of it, its been going on since 2019.

51 Likes

Can you please share the link of Garware’s VP thread link?

Thank you Harsh sir for adding so much knowledge in my life.

1 Like

Hi @harsh.beria93 , would this be a good time to re-evaluate ICICI/IDFC over HDFC Bank?

Results have mostly disappointed since some time.

2 Likes

2 Likes

Good returns but it’s wrong to compare them with Nifty50 as the latter is not a representative benchmark for you. Your portfolio is heavily tilted towards small and microcaps where risk premium is always considerably higher than Nifty 50 index. If some PMS fund manager came to me and asked me to give them 100 dollars and then told me that they would invest all that money in small/microcap and deliver 10% more return than Nifty 50 in next 5 years, I’d not be impressed.

However if that return was 30% over and above Nifty 50 then I’ll think about it. At the same time if they told me that they would deliver to me small caps index return then again I’d not be very happy as I can buy a small caps index myself and save PMS fee.

Finally, my humble opinion is that buying 50 stocks and churning them every 3-4 months is not a great strategy for wealth creation (I’m yet to see anyone building great wealth over a long period of time with this strategy) unless you are regularly beating the representative index or mutual funds (having the same portfolio mix). If not, you are better off buying representative index and mutual funds and reduce your opportunity cost, unless, again, you enjoy the process of investing and analyzing companies.

9 Likes

I see a lot of stocks in core compounder that are at best cyclical businesses. A compounding businesses has three main characteristics that are repeated over the years regardless of anything: 1)stable top and bottom line growth 2) stable margins 3) long term upwards trending pricing chart.

Trent, Nestle, Titan, HDFC banks to me are good examples of compounders. You can buy into these companies at any point in time regardless of valuations, economic cycles or general mood of markets, and still compound wealth at 15-20% over a long period of time. They have great underlying business model, a tangible moat and high quality management with great track record.

Calling some of the companies, whose businesses and stock prices have done nothing except post-covid, compounders will be a leap of faith. Also it’s hard to distinguish a compounding stock from the rest in a scorching bull run, we have seen post co-vid, where every single stock runs and market cares least about quality of books, management or underlying businesses. Narrative about every second company is so good that it leads common investor to believe that nothing can go wrong.

To me a good judge for a compounding business is if one can see themselves staying invested in a company for next 10 years and being confident of maintaining their returns.

I’d love to see how many of some of these small/micro-caps are still around in next 4-5 years and if they are still generating wealth. I’m sure 1-2 of them will become large caps or compounders but I don’t see any of them coming from real estate, chemical or pharma space. It hasn’t happened in the history so very less chance will happen in the future.

8 Likes

Harsh sir define their process of selecting consistant compunder in his past blogs in many times. Please read it carefully.

This thread is very much knowledgeable for new investors like me in which harsh sir define their process of selecting stocks , portfolio creations, weightage of stocks and selling process of stocks.

Thanks Harsh sir for your valuable inputs in this threads and i am always very grateful to you in my investment journey for your wisdom.

8 Likes

I’m not against any particular style of investing but having been in the market for quite sometime and observed several investors (both successful and unsuccessful) over a period of time, I believe that one can not be both trader and investor at the same time. Long term investors share certain characteristics that traders find it very difficult to emulate and vice-versa. That said there are enough statistics available that favor long term investing as a more effective means to generate superior wealth than trading.

To me having 40-60 stocks in one’s portfolio with constant churn is not long term investing but more of a trading style which chases momentum and narrative. In a prolonged bull market (like the one we are seeing currently) narrative and momentum trump fundamentals and every second stock is a winner. In 2023, over 1600 stocks delivered more than 50% return. My own portfolio generated more than 50% return but I only attribute this to the luck of being in the market than any specific skill I possess.

There have been so many cases of promoters of small caps/micro siphoning off funds, cooking books and colluding with operators to run the stocks. Their narrative to the market is always rosy and they always say the right things in interviews/concalls to convince the common investors that their company is the next best thing. You will see such companies doing very well during bull market and not so good during bear market.

For new investors it’s safe to stay with quality names than take too much risks get into small and microcaps where it’s very hard to assess quality of management. No reading of financial reports or management commentary will help unless one has direct access to the management (and even then there is no guarantee). If 15% CAGR with all the risks of small caps/microcaps investing is goal, buying an Nifty ETF will generate better return on a risk adjusted basis.

11 Likes

Could you pls list a few names that have generated 50% return over 10-20 years so that I can study their style? I am yet to find someone who has done 20% on a long term basis (let alone 50%) but I may be wrong.

1 Like

There are likely numerous ways to make money and that is the primary purpose of investing.

- What matters is portfolio returns and not individual stock returns.

- The actual returns are only known to the person who is doing the investing. Investing is an individual sport which is not in competition to others. So beyond a point there is no point in such discussions.

- The idea of investing is not necessarily to follow a more publicly defensible/popular idea. If I cannot explain my idea clearly and am still making money, I am happy to follow that. Ideas can be complex.

- My purpose of being in this thread is to get ideas passively and not debate. At least not debate the basic approach of the author. This thread has been incredibly useful to me - in terms of making money by getting ideas.

Certain ideas (like “consistent compounders”) are more popular but we can never know the actual returns made by its practitioners. But investing is not about popularity of ideas rather than XIRR made on the portfolio.

28 Likes

Hi @harsh.beria93,

A few questions regarding your data sources and process:

Do you use screener.in for all your data/ratios or do you use other sources as well? e.g. Sometimes Screener.in, Trendlyne and Money Control will have slightly different PEs for the same stock.

How do you track stock prices since you have a largish portfolio? Where do you have your price alerts setup? Do you set PE alerts as well?

How long do you spend studying a company before deciding to invest? Do you have a method to study all companies or does it vary from industry to industry?

How many hours a week do you spend on the market?

Congrats on the great work.

4 Likes

@newbie_007 check this

4 Likes

Thank you Vivek ji for pointing out this thread. Valuepickr itself seems like a treasure island with so many nooks and corners containing interesting information.

1 Like

Hi Harsh,

About Garware Hi Tech are you not concerned about the fact that nearly 30-35% of PAT is paid off as a fee to unlisted party ?

4 Likes

PROPEQUITY_02022024120044_InvestorPresentation_Q3Final.pdf (4.9 MB)

Prop Equity (P.E Analytics) investor presentation for Q4

4 Likes

Hello Harsh sir, first of all thank you so much for sharing such great content regularly. Sir i just want to know that are you only a Fundamental Investor or a Techno-Funda investor?

Thanks for your comments, although I am not sure whats your point. Also congratulations for your fantastic returns ![]()

The point of my investing process can be summarized by the comment made by @Vivek_Singh

I use a lot of sources for data mining (screener, tikr, tijorifinance, EPFO, eaindustry.nic.in, etc.).

Screener’s alert feature is very useful for setting valuation alerts. I also have very good friends like @rajanprabu who create automated alert systems for the stocks we track. These are generally more sophisticated alerts (like EV/sales going below certain moving threshold, etc.).

On timing and other things, these are very fluid topics. I try to do my best.

Yes, it is an issue. But I cannot control it except with position sizing and trying not to overpay. While accepting governance issues, I still want to participate in their growth opportunity. Its a very very good business.

How does it matter? I find labeling very counter productive, you dont gain anything but it often messes with your mind when you have to take certain contra calls which goes against whatever label you put on yourself.

17 Likes

It was a fairly straight forward question, and I am sure he wanted to know because it helps to know the answer. And from what I have read in this thread, you seem to base your investments on the businesses, valuations, and look at price in the context of the business while initiating positions, so does that not make you a fundamental investor? Dr. Hitesh is a FA+TA practitioner, who differentiates between his trades.

2 Likes