The Quant Journey

With 2 recent books on investors / traders who were predominantly quants, there is seemingly an awakening of quantitative methods amongst investors in India. The two books are The Man Who Solved The Market on Jim Simons and A Man For All Markets by Ed Thorp. Let me take some time to pen my journey down. This is a developing story and I am probably in the first chapter.

Flashback

My journey into quant systems started about two and a half years back.

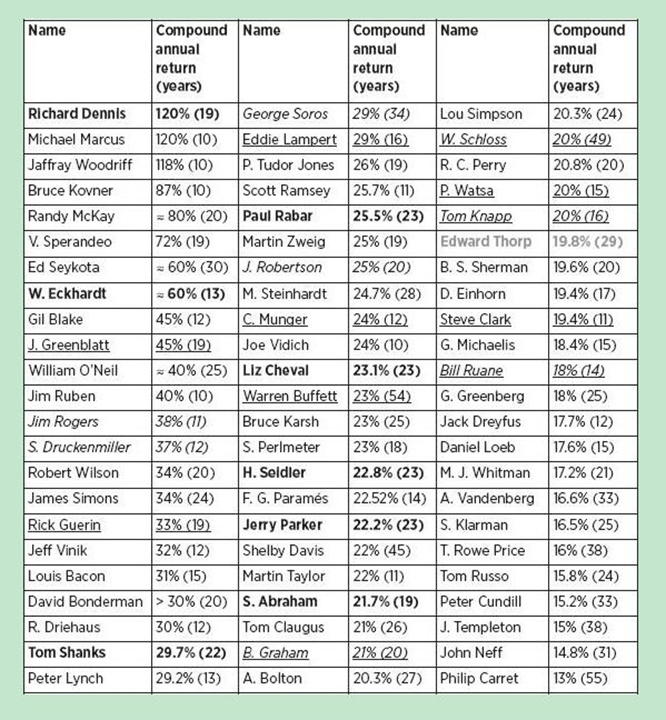

It showed, not sure how accurately though, the CAGR of some of the best investors (or traders) in the world. Scanning the list I gathered that I knew about nearly all of the people mentioned. What was interesting was that the names on the list came from completely different investment styles. Some were hard core bottom up stock pickers, some were macro traders, some technical traders, some commodity traders and some quants.

I have always been a curious person. And I always try to go back to first principles. So, I asked myself that if there are people who have been this amazingly successful over decades being non-fundamental, non-bottom-up investors, then am I missing something? Have I drunk too much of the Buffett kool-aid?

I decided to make the decision for myself. So, I started learning. I took a course of technical analysis. I started reading voraciously on quantitative systems, automated trading systems, mathematical and statistical indicators. The whole objective was to understand and assimilate as much as possible of these into my own accumulated knowledge of long term investing.

There were two other triggers to this. The first one was during our long walks on the beach during the VP annual meets in Goa with Hitesh bhai (Hitesh Patel) I realized that he had been very successful at blending technicals with fundamentals and was able to follow many more stocks and get very good results though with a higher amount of churn. That was worth thinking about.

The next thought that triggered was I wanted to be able to teach my son about investing and the road I took seemed very long and arduous and everyone has to start from scratch. I was looking for a structured process that could be taught and learnt relatively easily and in shorter time.

Cut to Now

The proof of the pudding is always in the eating. So, to prove and enhance my learning, I have worked on multiple algorithms and have picked two of them and have started investing for the last 3 months. They are mechanical, systematic, non-discretionary systems. I have a friend, who shall go unnamed for reasons of privacy, whom I collaborate with closely in this.

All the words are important. The system is mechanical meaning there is no human intervention during decision making. It is systematic meaning that buy-sell decisions are time based and pre-determined. Non-discretionary means once the algorithm tells me to buy something, I buy. I do not rationalize the choice.

The Results, Thus Far

September 2019: 0.81% (Complete)

October 2019: 22.06% (In Progress. Sell Date 1-Jan-20)

November 2019: 3.56% (In Progress. Sell Date 3-Feb-20)

December 2019: -1.02%(In Progress. Sell Date 2-Mar-20)

XIRR (till date): 58.8%

The results thus far have been excellent. To say the least. I have backtested this for various durations and periods. Since the availability of data is a major challenge, I have been able to backtest only for slightly more than a dozen years. What has given me confidence is that the backtest period covers the 2008 and 2018 periods.

More about the system in the next post. Also, will try to log my learnings in this thread for future reference.

DISCLOSURE: I am a SEBI registered RA and run an equity advisory service. This and all other posts are for educational purposes only. They should not be construed as investment advice.