Thanks for your comments, although I am not sure whats your point. Also congratulations for your fantastic returns

The point of my investing process can be summarized by the comment made by @Vivek_Singh

I use a lot of sources for data mining (screener, tikr, tijorifinance, EPFO, eaindustry.nic.in, etc.).

Screener’s alert feature is very useful for setting valuation alerts. I also have very good friends like @rajanprabu who create automated alert systems for the stocks we track. These are generally more sophisticated alerts (like EV/sales going below certain moving threshold, etc.).

On timing and other things, these are very fluid topics. I try to do my best.

Yes, it is an issue. But I cannot control it except with position sizing and trying not to overpay. While accepting governance issues, I still want to participate in their growth opportunity. Its a very very good business.

How does it matter? I find labeling very counter productive, you dont gain anything but it often messes with your mind when you have to take certain contra calls which goes against whatever label you put on yourself.

It was a fairly straight forward question, and I am sure he wanted to know because it helps to know the answer. And from what I have read in this thread, you seem to base your investments on the businesses, valuations, and look at price in the context of the business while initiating positions, so does that not make you a fundamental investor? Dr. Hitesh is a FA+TA practitioner, who differentiates between his trades.

Hii Harsh!!! Many many thanks for putting such a marvellous thread.My question is

1.In Avanti feeds concall,they have mentioned that they are not able to pass the raw material increase price to farmers.How do you see this business now and in coming years?

2.How do you see Punjab chemical performing in upcoming quarters?

I have a slightly unconventional thought process on this. Any activity aiming to make future predictions is speculation. In my line of work, I create mathematical models projecting how climate change might affect water resources over the next 50 to 100 years. So you could say I’m a full-on speculator. I guess you could call me an “investor” if you really wanted to, but it doesn’t quite capture what I do.

Very hard to answer this question. I did some work on previous agchem downcycles which I am sharing below, maybe it can add some value.

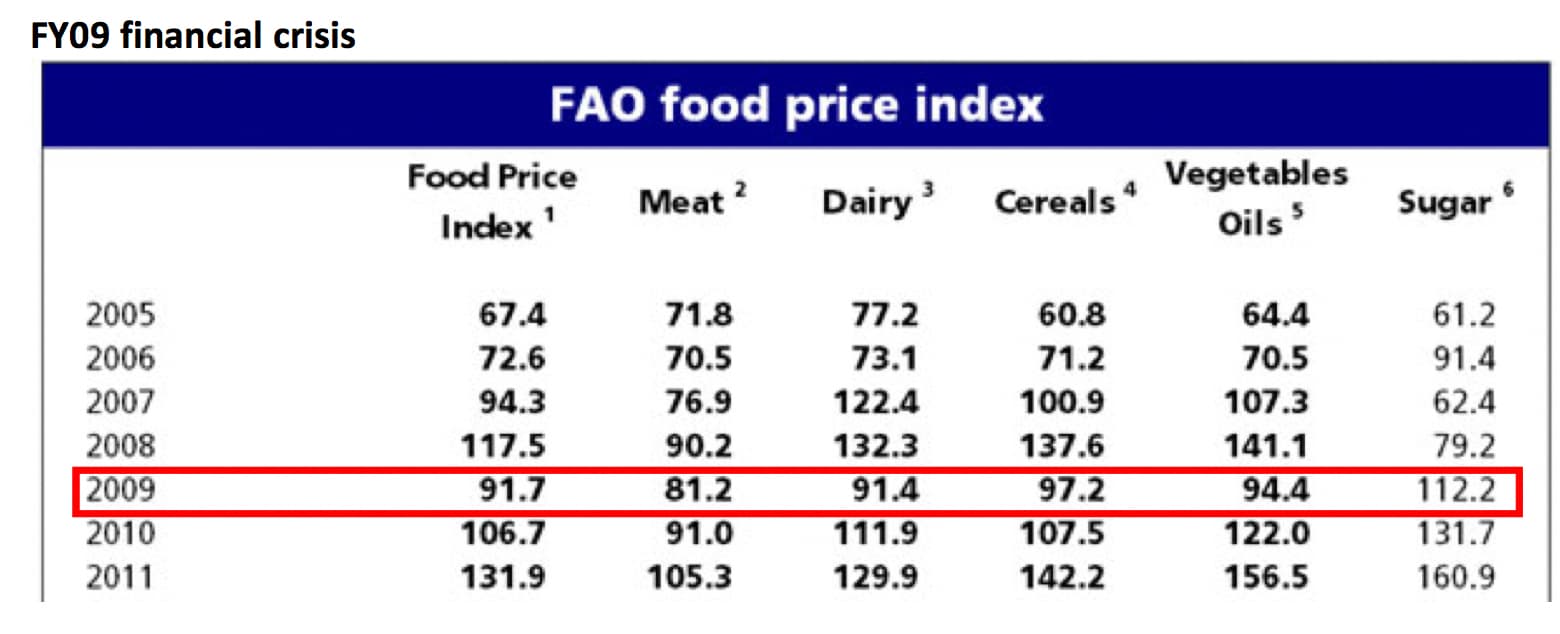

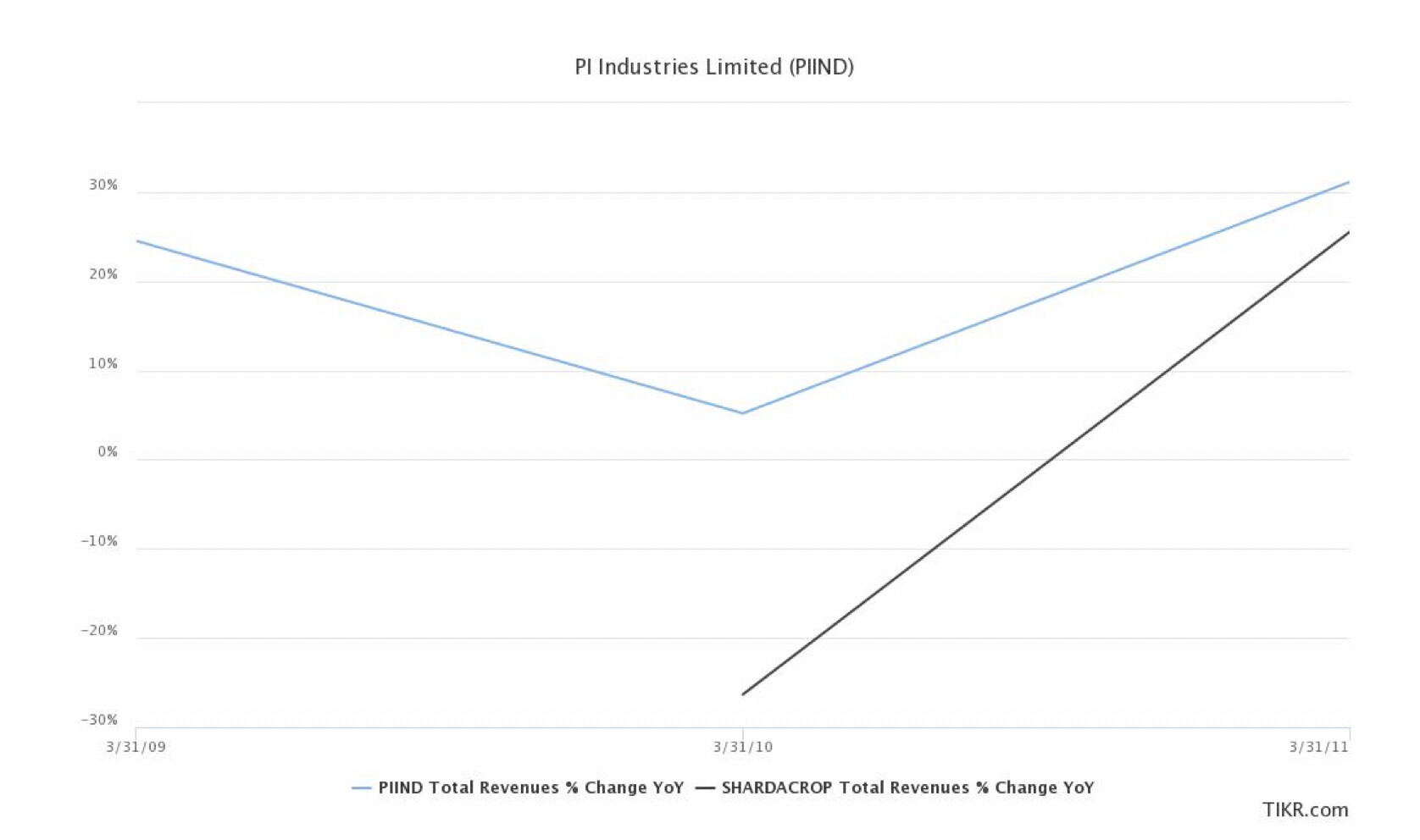

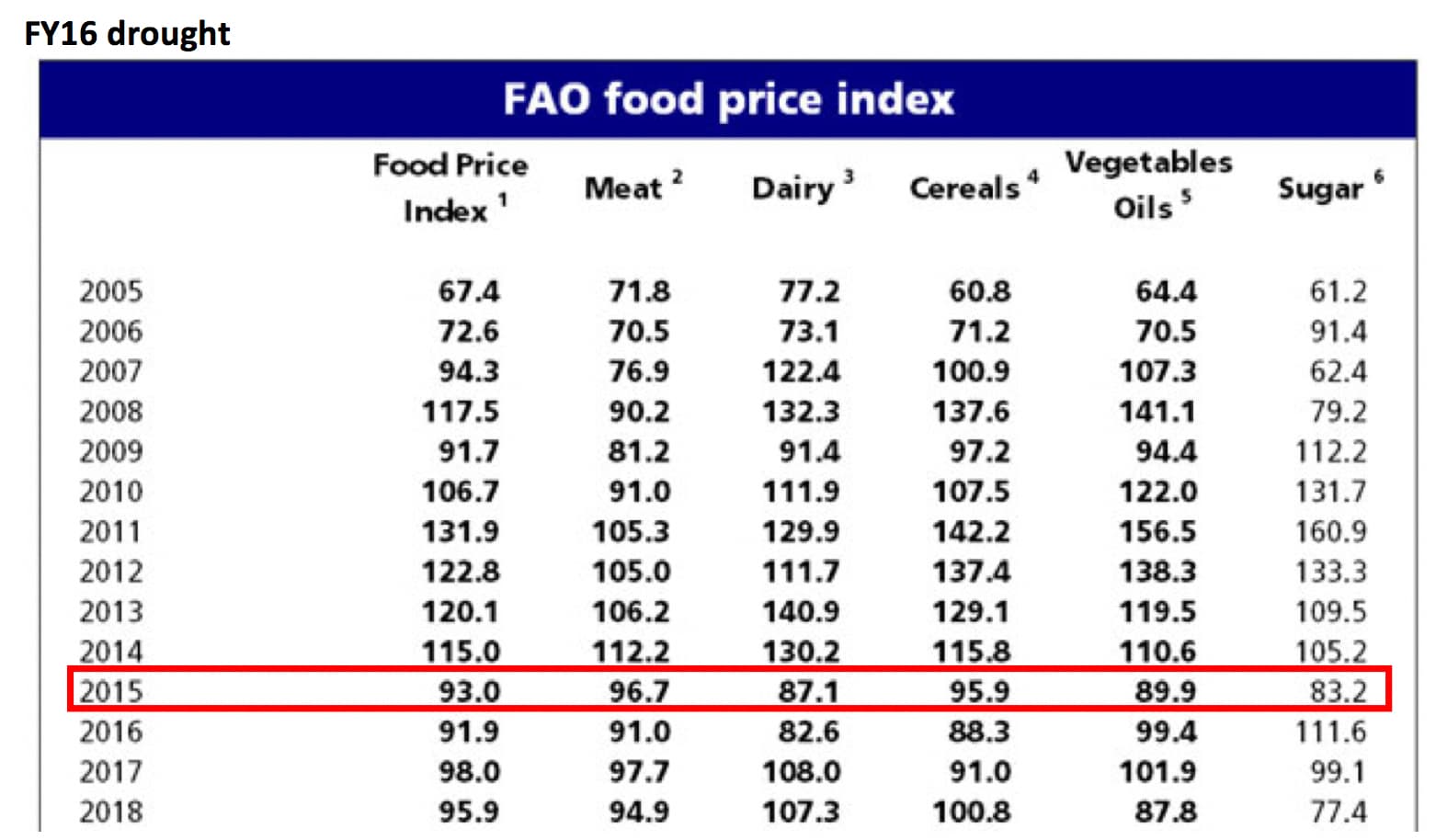

Analysis of downcycles (FY09, FY16) – 23.06.2023

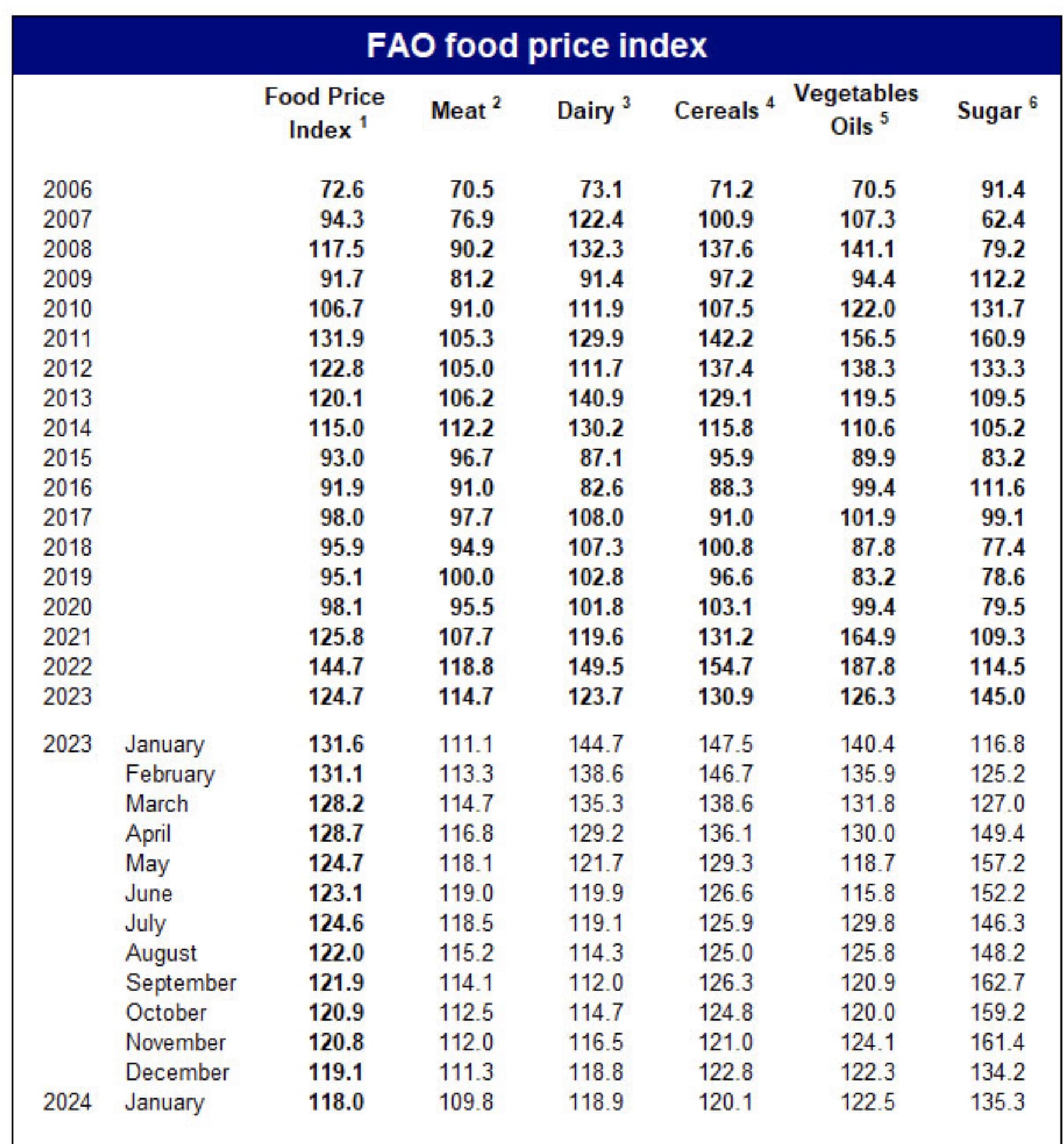

Underlying logic is when FAO food price index goes down sharply, farmers use less pesticides. Let’s see this with data of Sharda Cropchem and PI Industries. I have excluded UPL as they have kept growing in downcycles by acquisition

In 2009, FAO food price index dropped by 22%. This impacted sales growth of PIIND and Sharda in FY10. FY10 sales growth for PIIND declined to 5% (vs 25% in FY09 & 31% in FY11). The effect was more stark on Sharda, whose FY10 sales declined by 26% (vs 25% growth in FY11). However, both companies had a very clear revival in growth rates in FY11 as food prices recovered very quickly.

The next major downcycle was in 2015 where FAO food price index dropped by 19%. The impact this time around was more on PIIND, whose revenue growth rate in FY16 declined to 8% (vs 22% in FY15 and 9% in FY17). Sales growth for PIIND only recovered in FY19. Sharda managed this downcycle better, but their FY16 sales growth declined to 15% (vs 34% in FY15 and 14% in FY17). Their sales growth recovered in FY18.

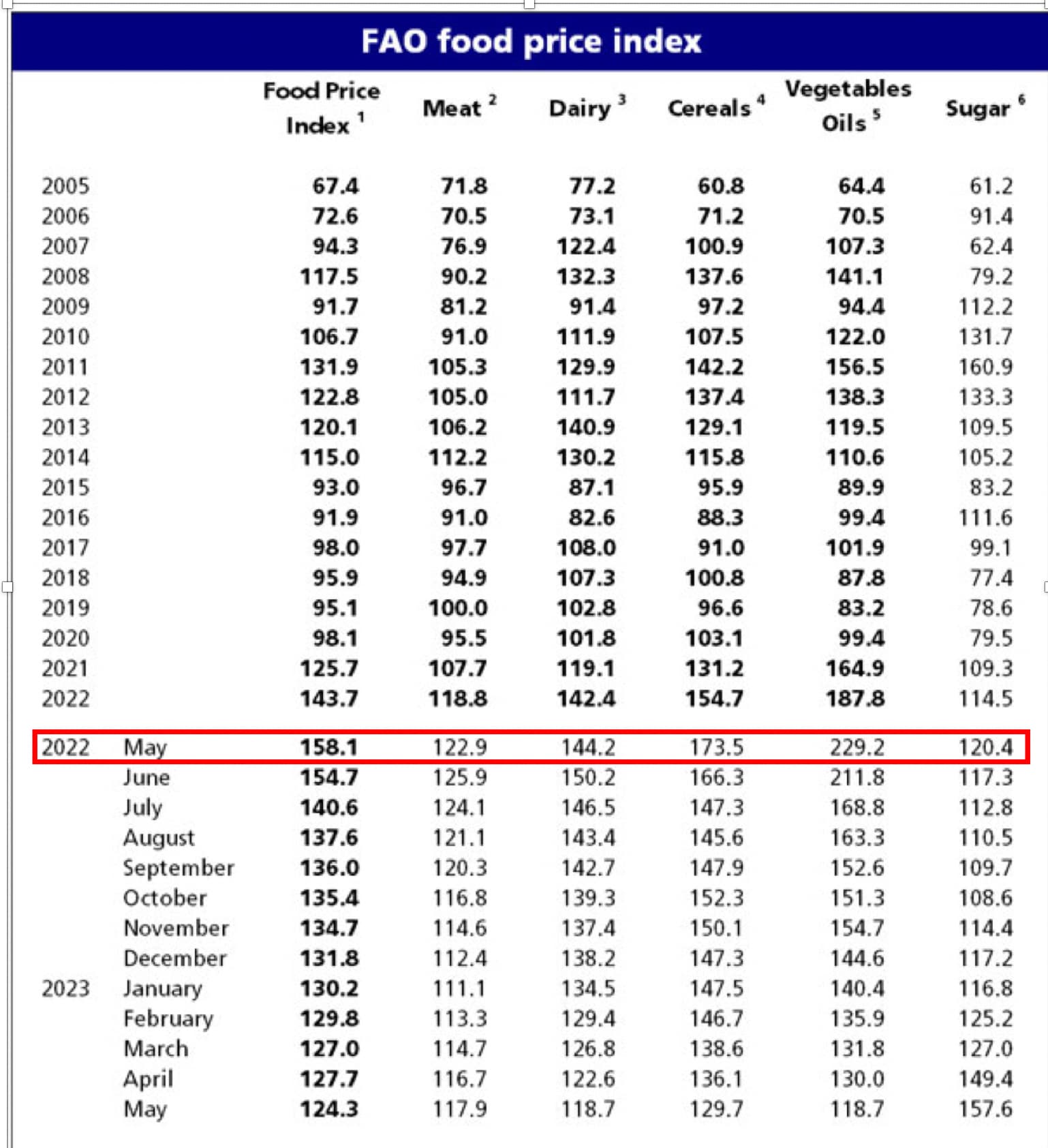

This time around, food prices peaked in May 2022 and have been showing decline for the last 1-year. It’s down by 21% already but hasn’t come down below 100, where in the past they have bottomed out. Given how high food prices became, recovery this time around can be prolonged.

Jan 2024 food prices are still 118 (very high by historical standards). So its hard to call it a bottom.

Avanti has struggled in past couple of years to pass on wheat and soya price increase because government regulated the final feed prices. Avanti nos are not really bad, look at other feed cos to see the carnage happening in this space (waterbase in losses). Avanti is a clear cut leader.

As explained in my agchem analysis above, we are coming out of a huge upcycle. I am personally still bullish on Punjab and have added shares in the last 30 days. I feel they have managed the whole downturn quite well, recovering their margins when most technical manufacturers are really struggling.

FAO index is something which i used to track in the past but lost track as i was strictly using this to guesstimate some kind of bottom. @harsh.beria93 Are the variables like meat, dairy etc equal weighted here ? or some weightage is available.

Refering to your comments on Kaveri Seeds, you said that its management is over promising and under performing now, compared to the past, where they used promise less but deliver far better.

Do you have data points based on which you can substantiate it?

@harsh.beria93 … Hello sir, one question from my side. Currently there is downtrend in agrochemicals cycle then any specific reason to invest in small agrochemical company like Dharmaj crop vs large agrochemical companies where valuation is reasonable low.

I think HDFC AMC AUM growth will not be in commensurate with its Operating revenue growth percentage.

For example, looked at YoY growth % of HDFC AMC w.r.t FY23 end → FY24 end,

AUM increased by 40% but Revenue increased by only 20%

Feel in case of CAMS, as it’s in services business, whatever CAGR growth mentioned (11%) will reflect in operating revenue.

So, not sure comparing HDFC AMC AUM growth % with CAMS CAGR growth % are the right metrics to compare for valuation perspective. Just presenting my opinion and welcoming others thoughts.

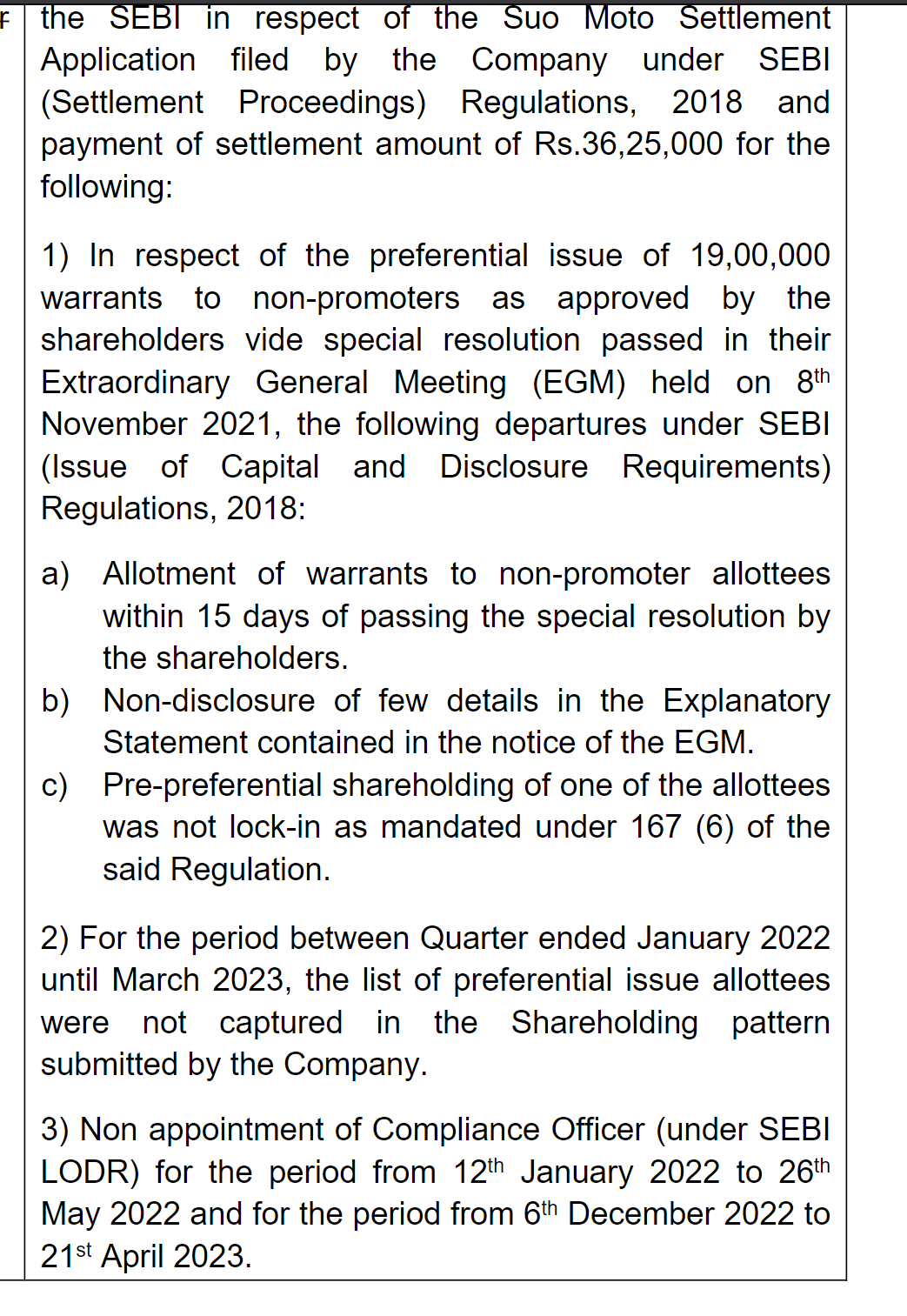

Hey Harsh, Sharat Industries has received approval for rights issue from BSE the details of which are yet to come out, the size of the rights issue is 49cr which seems quite big considering their market cap of around of 110cr. On their website a draft is available and they want to raise money for working capital purpose. Do you have any insight related to this requirement?

Also I was going through their history and found that they were penalised by SEBI for not appointing a compliance officer and for not disclosing shareholding after preferential allotment.

Hello Harsh Sir, Mayur uniquoters have given a sale guidance of 20 % increase for Fy 25. Also they have indicated that the margins will be in the range of 20 to 22 %. Given that they have done well in Q4 fy24 what is your take on this please

15% revenue growth with sustained improvement in profits is guidance from Management.

On congervative if we consider 15% revenue growth with same profit margin of 22%, EPS of FY 25 is 127.6, with that EPS forward PE comes to 28. Seems cheap with PI quality.

Please requesting your views. Looks cheap or low tax issues need to be considered in eps? Are you adding?

Thanks as always.

I find Dharmaj to be quite an interesting risk reward opportunity, as its growing quite fast and there is a good scope of margin expansion in next 3-4 years as their technical division scales up (higher margin than formulations division). However, near term profitability might be negatively impacted by operational and depreciation costs of their new plant.

As explained above, I find Dharmaj to be a good growth opportunity trading at reasonable valuations. Just to highlight how well they are doing, even in a remarkably tough year they grew sales by 24% when UPL (the largest agchem co) reported 20% drop in sales and losses! Dharmaj and UPL are at different life cycles, its easier for Dharmaj to grow at 20%+ whereas if UPL does that, they will outgrow the market they are serving.

Please read the Kaveri thread posts during the 2011-14 timeframe and make your own judgement.

I made a few changes in the last few months and will share them once I get some time. Its been a busy few months.

Sure, we all have our own ways of looking at things which is what makes the markets very interesting. The forces of decreased realisations as AUM scales also applies to CAMS, its not limited to AMC cos.

Sorry, I dont have any meaningful insights on this.

I sold out of Mayur and used the proceeds to buy more of Stylam shares. I feel Mayur is facing a very tough time scaling up whereas Stylam seems to be benefitting from multiple growth drivers (higher exports, potential of domestic scaleup, etc.).

I agree, I also bought more PI earlier this year. At different points of time, investors have gotten fascinated with a host of specialty chemical cos and have driven their valuations to crazy levels. I remember people went nuts about “fluorine chemistry” or “electrolyte chemistry” or “waste to wealth” etc. When investors start teaching you chemistry, I want to run away!

PI is probably the only chemical cos which is actually differentiated, and have grown even during these tough times. And they are now foreying into the pharma business, which is a much bigger market, more moated if one cracks it, and gives higher margins. I like how management keeps expanding their TAM.

About allocations, during 2020, my allocations in PI went to 6-10% and I tapered it down in subsequent years due to very high valuations. With their valuations now cooling down, I feel quite bullish on PI and want to again scaleup the position.

One comment on the PI Industries. From Various reports, it is evident that Chinese Agro Chem players are building aggressively and intensified Chinese dumping and also the major molecule PI is working on is going off patent. Have you looked into this aspect and still think PI industries is a good bet? I have been holding PI since 2020 and sold it now.