In the past few quarters, Godfrey has been reporting good nos especially when compared against peers. I am sharing some notes around domestic volume growth and export business below.

04.02.2024 (thoughts post FY24Q2 results and comparison vs peers)

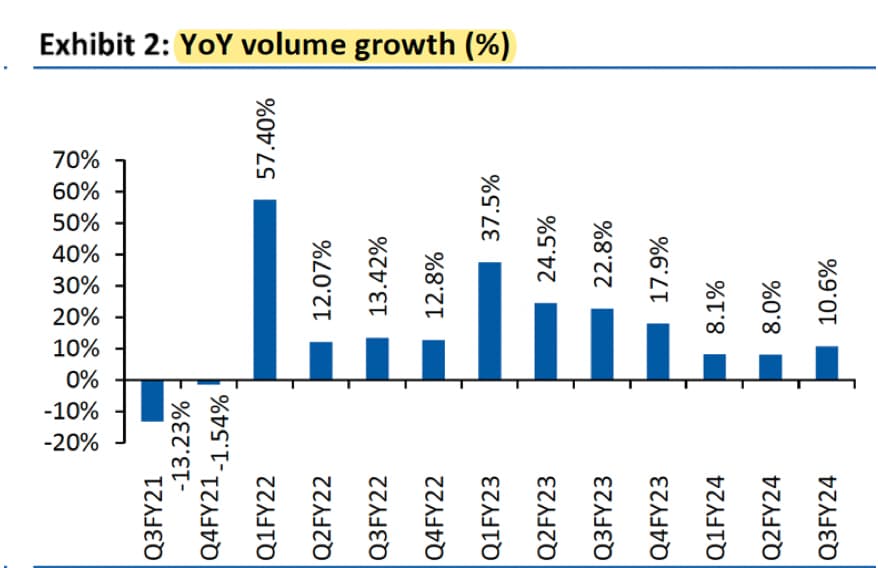

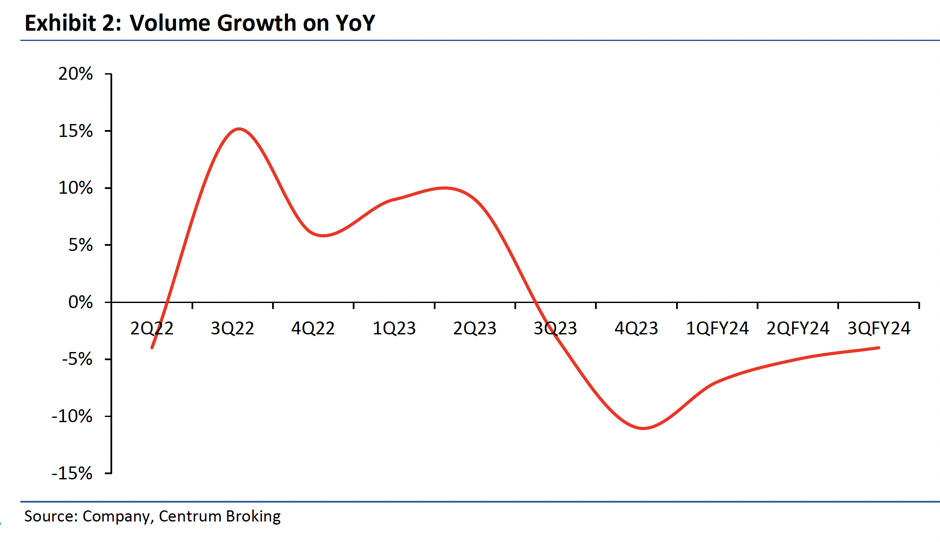

- Godfrey continues double-digit domestic volume growth

- Marlboro brand grew volumes by 27% due to launch of lower priced SKUs

- ITC reported (-2%) negative volume growth

- VST reported negative volume growth

Their domestic volume growth has been consistently higher than ITC over the past many quarters. Since post COVID dip in FY21, domestic tobacco volumes has grown at almost 18% CAGR.

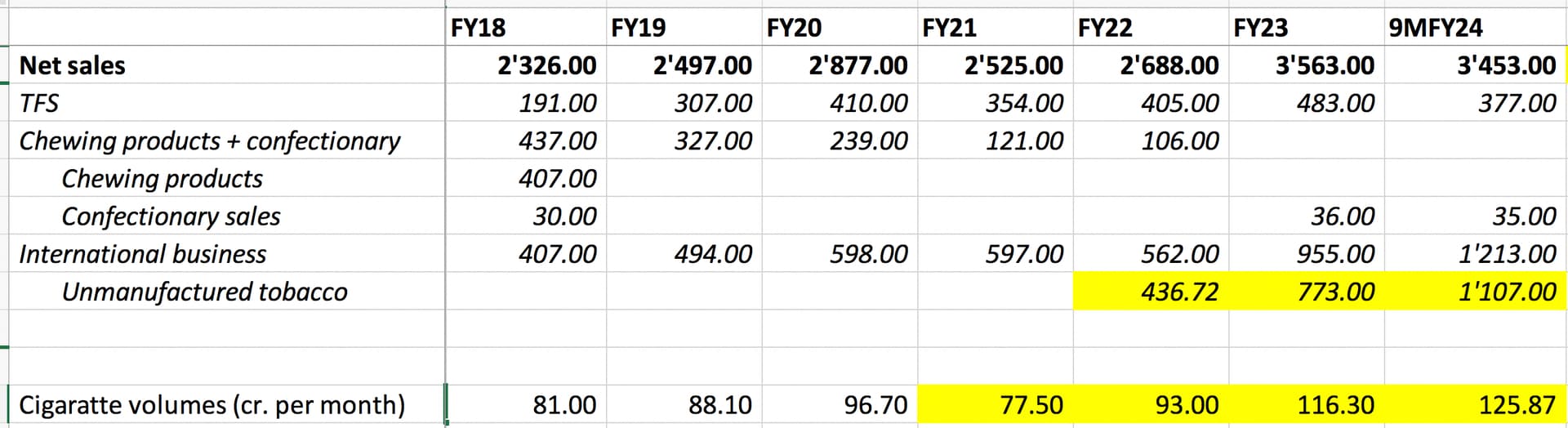

Another major revenue kicker has been their growing export business with Phillip Morris, especially triggered by the Ukraine Russia war. This is also benefitting other tobacco companies, but Godfrey has benefitted the most so far (look at growth in export nos below). International business has almost become 4x in last 6 years.

Disclosure: Invested (position size here, bought shares in last-30 days)