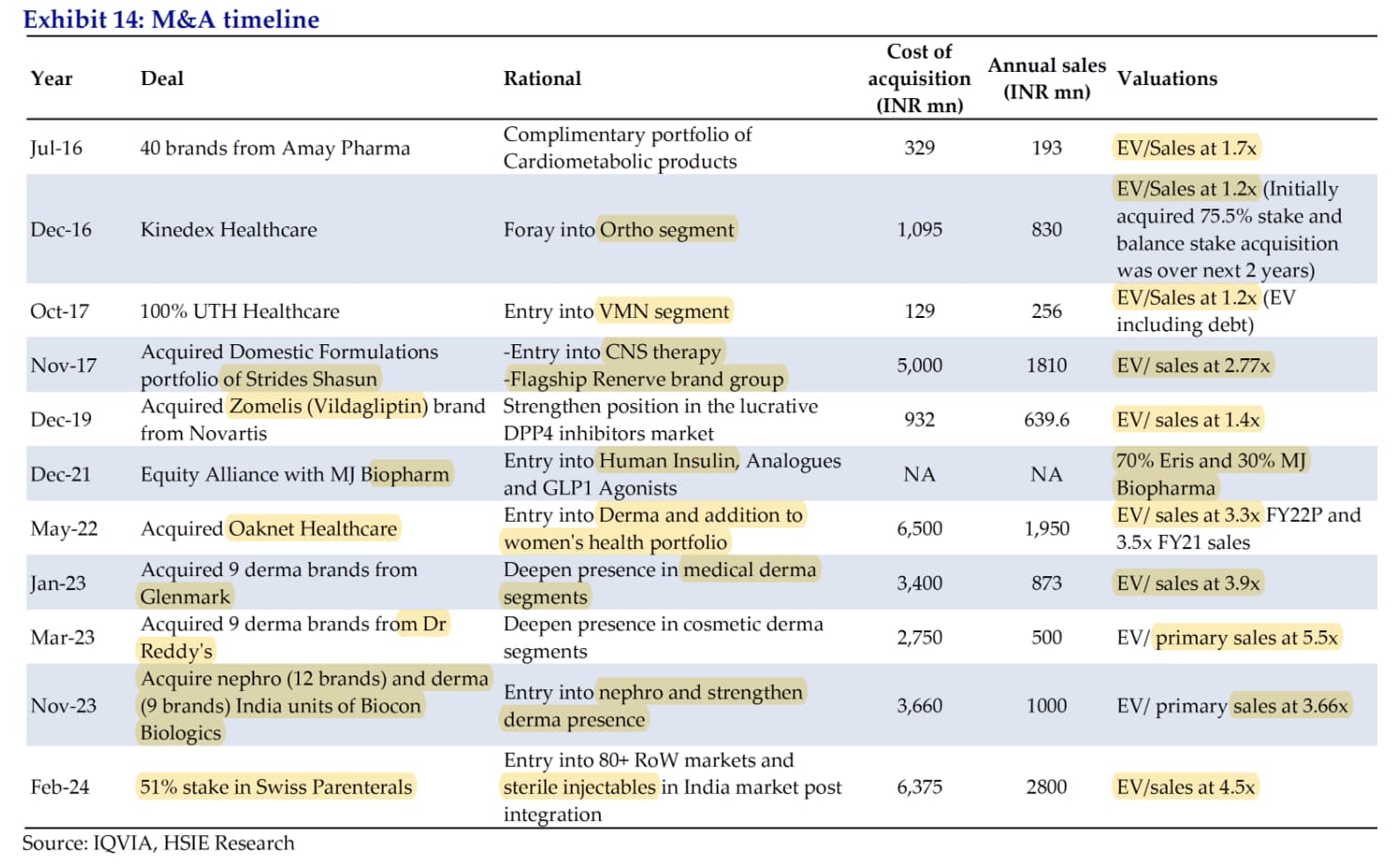

Eris has been now on a huge acquisition spree, having spent close to 3500 cr. in last few years on acquisitions. One thing this clearly highlights is how hard it is to grow organically in branded market (or that Eris is lacking that capability).

The only good things about their acquisition is large acquisitions are done to get into new therapies, and they pay reasonable valuations for most acquisitions (~3x trailing sales). See a summary of all their acquisitions below.

14.03.2024 call notes

-

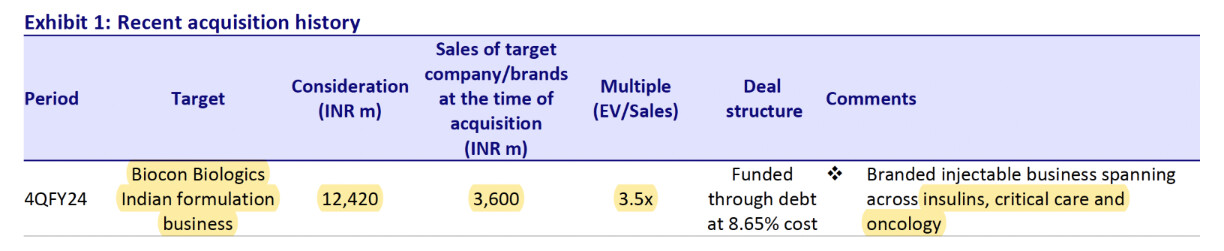

The Swiss Parenteral and Biocon biologics deals were evaluated together

-

Biocon biologics

-

Acquired Indian branded sterile injectable business of Biocon Biologics (1242 cr.; 360 cr. sales; 70 cr. EBITDA and will increase to 100 cr. in FY25). This will expand their presence in the sterile injectables market and has synergies with Swiss Parenterals Limited

-

435 employees (325 MRs), price includes 50 cr. net working capital

-

Oncology (Monoclonal antibodies; MAB; 80 cr.; 40 field force including 30 MRs) + insulin (200 cr.) + critical care portfolio (80 cr.; 70 field force)

-

Critical care manufacturing will move to Swiss Parenteral, Mabs and Insulin will be sourced from Biocon

-

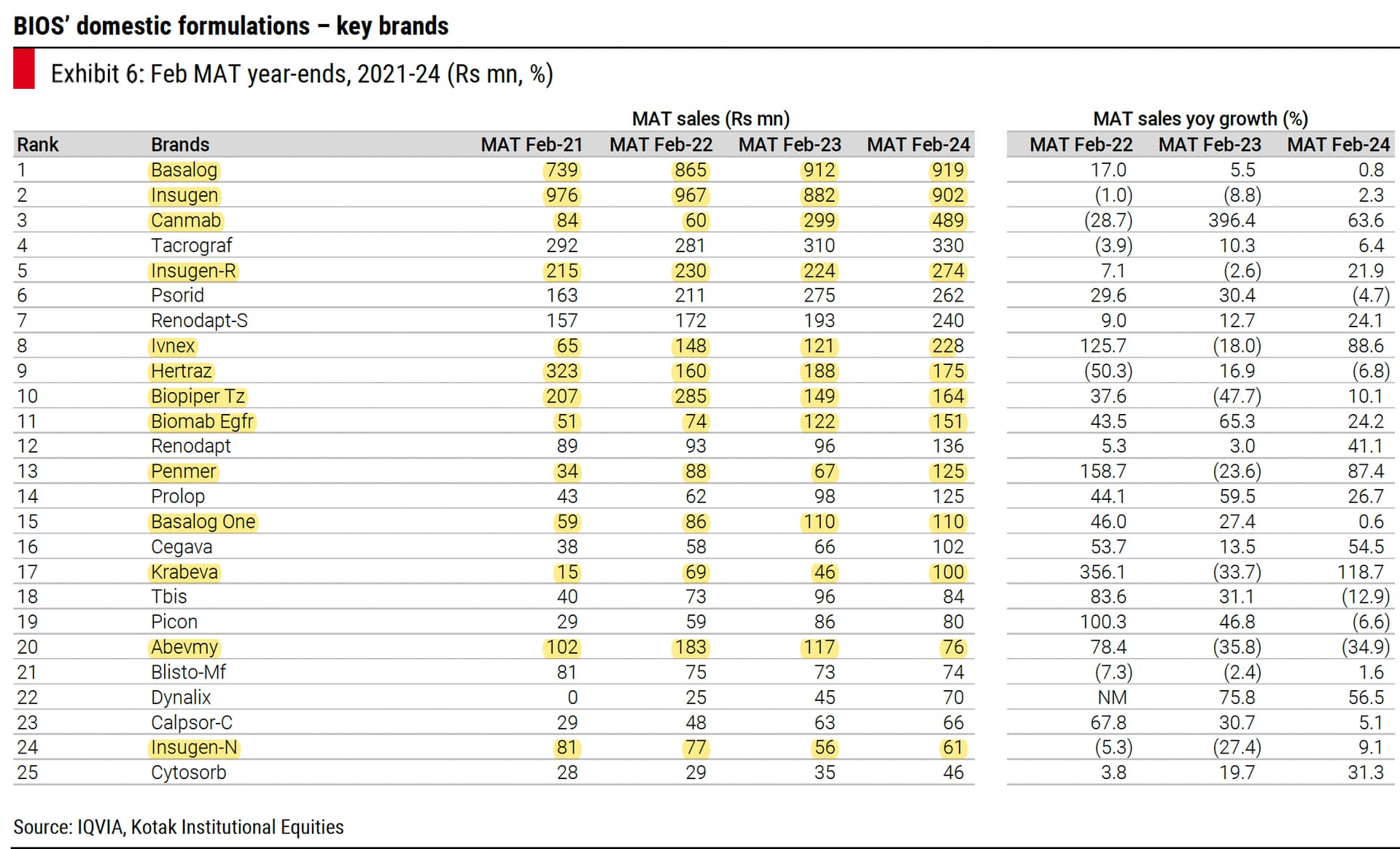

Insulin:

-

Basalog (Glargine; 8.2% to 10.5% market share in last-4 years) - 100 cr. brand

-

Insugen (rH insulin; 9.5% to 11% market share in last-4 years) - 100 cr. Brand

-

Both Basalog and Insugen have not grown in last 5-years, but have gained volume market share

-

RH insulin Indian market has declined in volume terms in last 5-years

-

Insulin can reach 70% gross margins

-

Hope to gain from interchangeability acceptance for Basalog (no other biosimilar in India has this)

-

-

Will continue their own Xsulin and Xglar brands

-

Anti-diabetes will be a ~1000 cr. franchise now

-

Oncology – 5 main brands (Biomab, Canmab, Hertraz, Krabeva and Abevmy). Market is growing at 26%+ p.a. 80 cr. sales with

-

Acquired brands highlighted below (maybe more, only highlighted ones where I am sure)

-

-

Will acquire 19% equity stake in Swiss Parenterals Limited from Eris’ promoters (237.5 cr.; same as original acquisition price of 1250 cr.)

-

FY25 net debt will be <2x of FY26 EBITDA (1-year forward). Net debt will be 3000 cr. From now on, focus will be on optimizing acquired units. Cost of debt is 8.65%

-

Target to reach 5,000 cr. revenues in FY28 (vs FY29 earlier)

Disclosure: Invested (position size here, no transactions in last-30 days)