Kolte came with horrific set of nos, with margin misses coming from even recently acquired projects. Management keeps giving very bullish guidances and are now guiding for 13,500 cr. presales over next 3 years, when their FY24 presales was only 2800 cr. Their execution in terms of growth while preserving balance sheet has been decent during the industry downturn but they are not really showing good nos during the upcycle. Nos below

Concall notes:

FY24Q4

-

FY24 nos

-

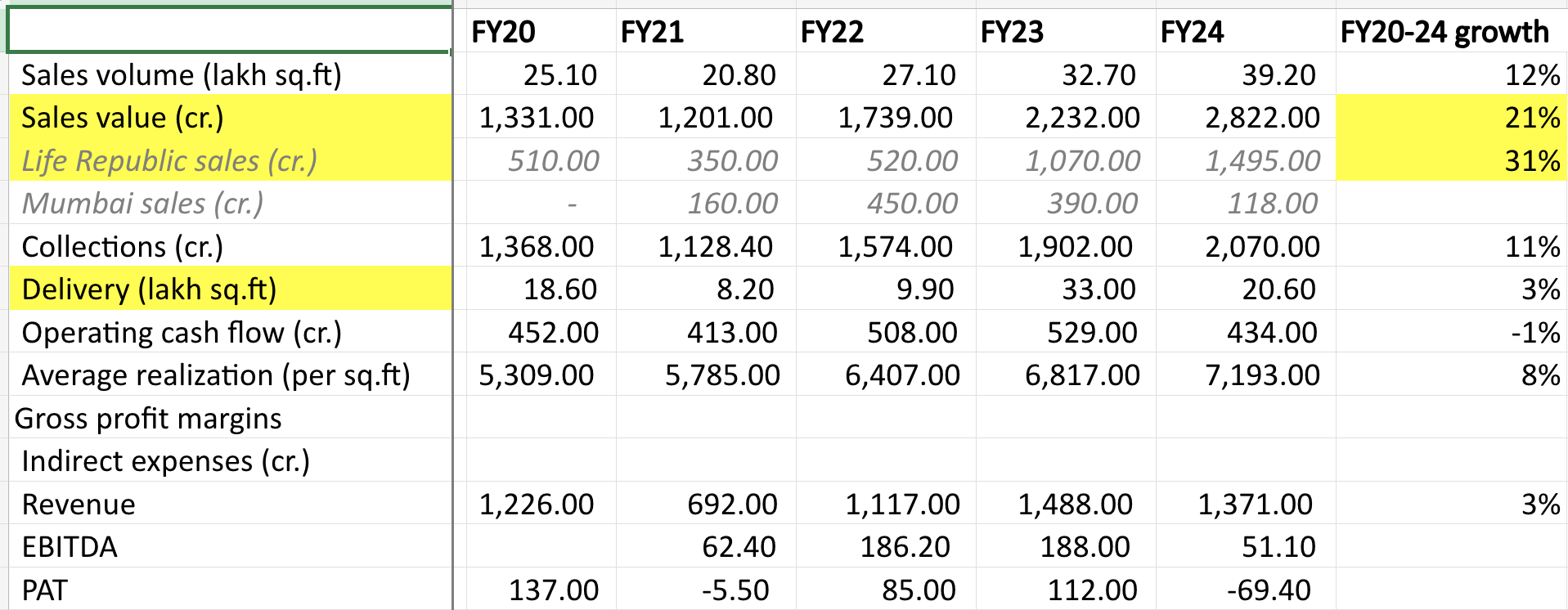

2,822 cr. presales value in FY24 (guidance of 2,800 cr.) – 20% volume growth + 6% realization growth

-

Acquired projects worth 6,095 cr. including 2,100 cr. in Life Republic (guidance of 8,000 cr.)

-

Launched 3,816 cr. projects (guidance of 5,265 cr.). Missed timely launches in Wagholi (400 cr.) and NIBM (360 cr.) which will get launched in Q1/Q2 FY25. Strategically delayed a premium project in Life Republic (1300 cr.) as they wanted to reach a volume run rate before launching it. They plan to launch it in FY25. H1FY25 will see 3,500 cr. project launches which will be driven by Pune, Mumbai launches will happen in H2FY25

-

Delivered 2.06 mn sq.ft (guidance of 3mn+ sq.ft)

-

-

Guidance for FY25

-

Expect 25% sales CAGR from FY24-26 + 13,500 cr. cumulative presales from FY25-27

-

Acquire projects with topline potential of 8,000 cr. (5,000 in Pune + 2,000 in Mumbai + 1,000 in Bangalore)

-

Launch 8.95 mn sq.ft (8010 cr.)

-

Deliveries: 2000 cr. with early teens EBITDA

-

-

Sold 1,800 cr. of 3,800 cr. inventory launched in FY24 (lower than historical runrate of 50%+)

-

Potential sales from Life Republic is 12,000 cr.

-

Kiwale was a stalled project with inventory having been sold by earlier developer at very low realizations. Their delivery has also adversely impacted their margins (when they had acquired Kiwale in FY23Q1 they had said “Kiwale acquisition (~120 cr.) gives revenue visibility of 1400 cr. (with 24-26% EBITDA margins) with all regulatory approvals in place.”

-

Margins were lower because delivered projects in Life Republic were lower margin (average realization of 5,100 vs realizations of 6,400 in FY24). Life Republic projects had 25% gross margins in FY24, other projects had 11-18% gross margins. Overall gross margins was 22% for FY24. EBITDA margins will start improving from FY25 (early teens) and high margin projects will start getting delivered in FY26 (late teens)

-

Life Republic: construction costs were 2500/sq.ft, land and utility at 1000/sq.ft and realizations delivered was 5100/sq.ft

-

Pune real estate market is ~80,000 cr.; northwest Pune is 20-25,000 cr. and Kolte has 12% market share in northwest Pune. But in rest of Pune, they have less than 1% market share

-

Focus now is really to increase realizations, did 900 cr. of presales in 24K in FY24

-

They also calculate like-to-like margins, presales in FY23 generated 18-19% margins and in FY24 generated 26% margins

-

Projects launched after October-November 2022 have good margins. Before that there were higher contracting costs

-

Goodwill due to merger of a subsidiary was impaired by 23.46 cr.

-

Anticipate 100 cr. annual finance costs in next 3-years

-

Announced dividend of Rs. 4

Disclosure: Invested (position size here, no transactions in last-30 days)