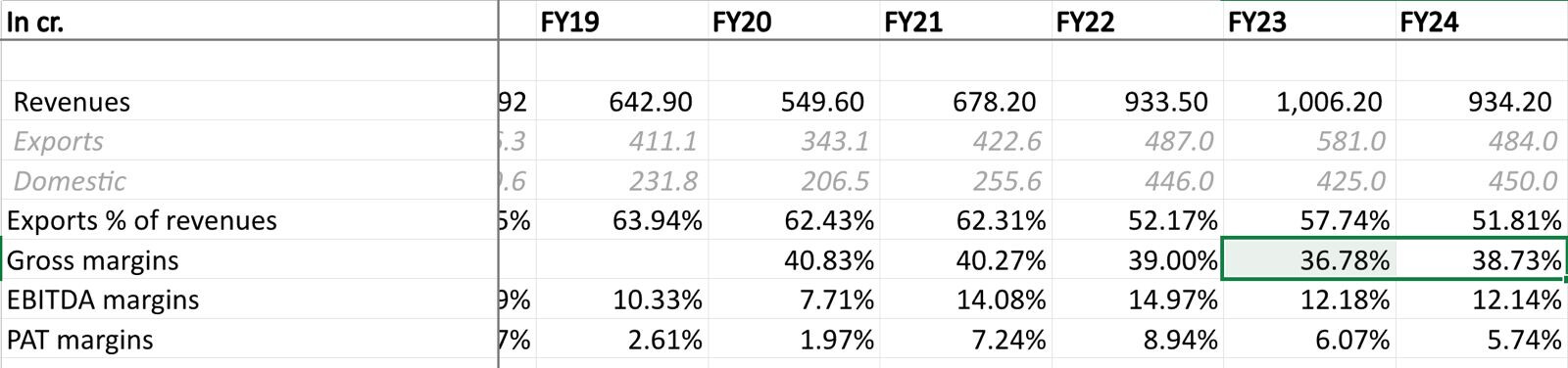

Punjab came with flattish numbers (1% sales growth, -25% EPS decline). The good thing about FY25 was their numbers were way better than most other technical manufacturers, they improved gross margins while seeing margin decline in sales (-7% in FY24) in a very tough year.

Volume growth is coming back and they expect complete revival by H2FY25. Management is also guiding for doubling of sales in 1-3 years. Concall notes below.

FY24Q4

-

Seeing demand offshoots and expect recovery in second half of FY25

-

Freight costs have increased significantly for certain routes (e.g. Europe, USA). 1.2 cr. increase in freight + higher CSR costs + certain one-time costs which have resulted in EBITDA margin decline despite maintaining gross margins

-

Have received commercial orders for new molecules (both in agchem and specialty chemical)

-

Receivable increase is temporary and because of domestic receivables being stretched from 90-100 days to 120-130 days. This has started coming back to normal in May

-

Capex

-

FY25: 50 cr. in existing sites (1 new manufacturing block + maintenance)

-

Continue scouting for new production sites and want to time it to industry revival

-

Expect 1000-1200 cr. additional revenues in next 1-3 years. 10-15% of this will come from existing products and remaining from new products. This will require 250-300 cr. capex (3.5-4x asset turns) at existing sites and can be done from their existing plans

-

-

New products

-

New product contributed 7% to revenues

-

1 product has global sales potential of $100mn, another one has $20-25mn

-

Producing 2-3 products every 6 months, should commercialize 2-3 new intermediates in next 6-months

-

EU commercialized product should reflect in next 6 months because of high current inventory

-

-

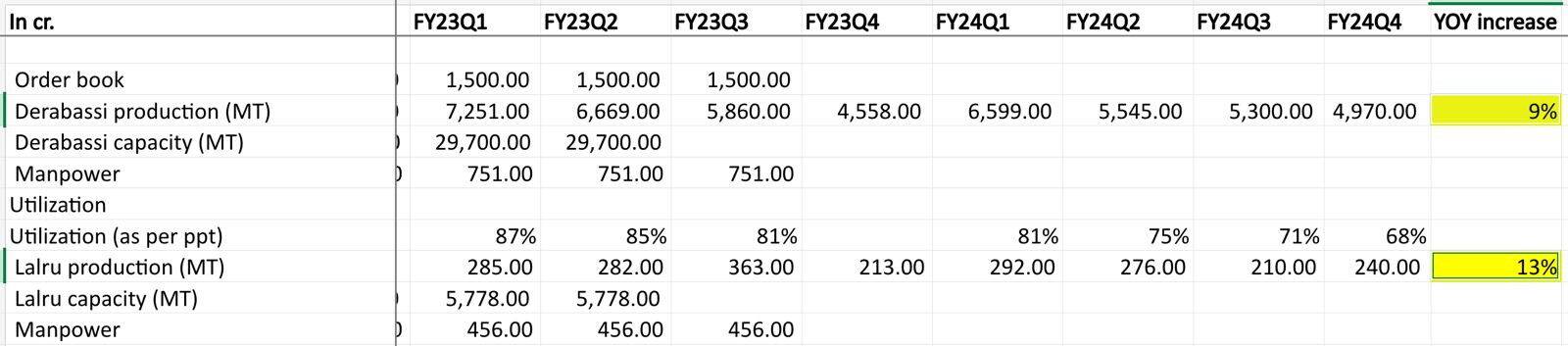

Business mix: 70% Derabassi, 15-18% Lalru, 12-15% Pune

Disclosure: Invested (position size here, no transactions in last-30 days)