Thanks for the suggestion, Ashok Leyland is going through a cyclical uptick and I dont think its appropriately valued. About Krsnaa, @Chins has done amazing work and has kept sharing his thesis around the company. I haven’t invested in it because I dont feel comfortable buying at 17x earnings when there are so many opportunities available at cheaper multiples, and growing at similar rates. One such co is Caplin Point where again @Chins has done amazing work!

I havent done much work on cement cos. I actually dont get why cement cos trade at a premium vs other commodity cos given they dont have higher growth rate or better ROCE. Its just wrong in my opinion.

Hard to tell, I have also been surprised that they have been struggling with margins despite having a strong competitive position. Even Care downgraded their rating due to this reason.

However, I have seen problems like these persisting for a few quarters in a lot of small cos and then they get resolved. The idea is to buy at very cheap multiples in expectation for a mean reversion. Sometimes, it happens quickly and other times it takes more time. Lets see what happens in Modison.

As of today, I switched out of Godfrey Phillips and added Transpek to the model portfolio. Godfrey trade played out very well, with market recognizing change in operating margins and resumption of growth in tobacco. While margin benefit is likely permanent in nature, the huge jump in revenue growth came because of tobacco exports which has now normalized. Although valuations are not demanding in Godfrey, I prefer playing tobacco sector with ITC as they have multiple value drivers.

Transpek has got back to pre-covid revenue run rate in their core business and are now getting more aggressive in growth, as shown in launch of five new products this fiscal. Margins have also shown a clear revival trend, in good times Transpek can do 20% EBITDA margins.

In the last concall, Transpek management guided that they have clear order visibility for CY23 and are working on reaching 1000 cr. of sales in a couple of years. At 20% EBITDA margin, this can translate into 200 cr. EBITDA and potential enterprise value of 2000 cr. (basically a doubler with good visibility).

I like the setup where a conservative management becomes more aggressive in pursuing growth (another e.g. is Sundaram Finance). Lets see how Transpek works out. Updated portfolio is below and cash stays at zero.

Hi Harsh,

You put in so much effort to find out good companies.Would not it make sense to have higher allocation to the ones with higher conviction and reap higher benefit. A 2% may not move the needle much is what I assume

Extremely well defined approach.

Also, I like the fact that, your allocation is same for all stocks with only 2 levels i.e. 4% and 2%. This gives arise to Equal Weight Portfolio which I believe is more stable and may give better returns. Most of us have tendency to allocate more weight to high conviction, highly undervalued stocks but often end up generating inferior returns as Mr. Market does not move the stocks up or down based on our convictions. Mr. Market does opposite things many time.

I am sure that, you might have thought about increasing allocation levels to 5% as well.

I will like to know your rationale behind only 4% weight. May be it is due to high no. of stocks which you like to own.

While calculating net return, most of us ingore dividend. Since the benchmark considered is also without dividend (Sensex/Nifty or any other index), and dividend yield being generally 1-2% for sensex and most of portfolio, we tend to ignore importance of Dividend. However, since I expect most of us to remain in stock market for 2-3 decades and more (depending on age and ability to digest market volatility and survive), the dividend is real return genetor in portfolio over 20 years+ horizon.

For instance, Sensex (1979=100) with Dividend yield estimated by me from various data on every March end, without Dividend would have been 58,568 as on 31 March 2022. However, if we have assume dividend from Sensex being reinvested, the closing value would have increased to 137,347 as on 31 March 2022.

My calulcation for very long term, almost century for Indian stock market, as on 31-3-1928 are estimated to be 40.98 as on 31-3-1928. (I have applied various periods RBI variable yield securities index and back calculated sensex value from 1979 being 100), increases to 58,568 as on 31 March 2022. However, with assuptions of dividend being reinvested, the Value of portfolio increases to 800,908 with dividend as on 31 March 2022. So ignoring dividend may not see any major impact on 1-2-3-5-10 years horizon. However, as period increases, Dividend contribution to portfolio return is much higher than capital appreciation in my limited understanding.

Some old working on this subject are avialble on this link

Thank you for this wonderful comment and a constant reminder of long term thinking. I love your work on extracting longer records for so many companies, I just hope you can get more time to keep sharing this kind of work for larger number of securities. I have found them very useful and have used them a lot for my own analysis

Coming to dividends, no other person has ever asked me about it or suggested me to maintain a record. Over past 5-years, my dividends have grown at a very meaningful rate (starting capital size was also very small). My longer term objective is to ensure that annual dividends exceed my net income.

Year

Dividends received (base normalized to 100)

2018

100.00

2019

383.79

2020

1’151.05

2021

1’729.63

2022

2’349.01

No scientific reasoning behind it, there are so many stocks having similar risk reward that I find it easier to maintain a certain allocation and worry more about finding new opportunities. At this stage of my life, I am much more interested in broadening my investing universe than worrying too much about exact allocations.

Congrats Harsh! Your thread is an absolute delight to follow. The clarity in your thought process and honesty in recording the results is amazing.

I have few questions just to pick your thought process:

1)How do you stay clear of those hot stocks (stocks with stories going round and round and prices move up and up till the sanity returns). Eg. API stocks after covid telling India is going to eat China’s market, Auto Tier 2 stocks which are sold as EV plays, Commodity chemical stocks sold as once in a lifetime capex+export substitution stories etc.,

2)I can see low P/E is a key criteria in your stock selection. Do you have any absolute value only below which you’ll buy or any range?

3)50% in cyclicals and how do you try to stay on top of the cycle. I understand you intend to get in lower end of the cycle and sell at peak. But how do you track? Do you have a source tracker of exports, Commodity prices, Chemical prices etc., How often do you check? Any entry and exit criteria?

I will invert the question and ask if you know of any investor who has consistently outperformed the market by buying whats flavor of the season? Most successful investors I know of are either very early in catching the growth cycle or have made money by investing through despair. You dont need to answer me, but I will request you to think deeply about this.

For well discovered companies (like ITC, HDFC bank, etc.), I see what valuation bands a company has traded in its past and try to buy towards the lower end of the band (more details below)

For undiscovered stocks or very small companies, I try to buy at <10x normalized earnings. I almost never pay >15x for small companies, unless I am very confident of the business quality and growth profile.

I am often not on top of the business or the market cycle. When I am buying, its almost guaranteed that there will be few brokerage reports and most of my work focuses on quality of balance sheet (rather than profit & loss statement). During upcycle, there is a lot of coverage around the stock and valuations are much higher than long term averages. Although, exiting just based on valuations implies that I will miss some part of the upside, its generally not a problem as there are often ample available opportunities. Over the past few years I have worked a lot on improving my selling skills (see some examples below).

Very few investors have focus on dividends and glad to see this post.

Another interesting point that I had highlighted elsewhere is that when one invests in growth companies for long term, as growth for those companies normalises, dividend yield from them increases. So dividend graph from these should increase at much higher rates than EPS growth.

Regarding your analysis, curious if you considered the path of dividend not being reinvested. Will then also dividend be much more significant than capital appreciation over very long term?

My logic tells me Yes it will be very close for above but would be good to know if your accurate analysis also reaches out to same conclusion.

Also, first decade can be considered accumulation and dividend reinvestment phase but subsequently constant capital and no dividend reinvestment.

You may not do this exercise (because already you have proved a very significant point rightly) but just thought to mention this practical scenario as for multi decades most would not keep reinvesting dividends or adding capital

Thanks again for enlightening this forum with number analysis as that is what many investors follow and admire. Simple logic often is overlooked cheers

Thanks for your nice reply. On specific, one has to assume certain return on dividend cashflow. In my case, I have assumed that Dividend being reinvested in market at the prevailing level. Hence, results in higher units of Index holding, resulting higher dividend inflow in future and also high terminal end value. Now, another approach could be assume dividend being invested in G-Sec and then to calculate terminal value of G-Sec. While it may be correct for some investor, it is difficult to calculate for me.

On point of dividend being taken at nominal value my view is if period is longer, one has to account for reinvestement of dividend. Dividend of Rs 1,000 at 31March2000 is equivalent to Rs 4000 in 31Mar2010 (assuming 15% growth) or Rs 1967 (assuming 7% of growth). The growth rate might vary, but absolutely wrong to assume 2000 Dividend value being same as 2020 Dividend value. That is why it is very difficult to do calculation of Total Shareholder return over 20 years period. Any return generated would have reinvestment rate which may vary from person to person. I have assumed that the funds generated from Dividend are reinvested in Index on that year level. I find that being simple, fair and practically executable assumption. Just adding nominal value of dividend and than compare to market value of portfolio after 20 or 25 years, would give to wrong results in my view.

Compounding appears simple/neglible in initial years, but become very complex to comprehend once time horizon of investment increases above 20 years.

Hi @harsh.beria93, thanks for the amazing thread and for sharing your strategy.

You were invested in Shri Jagdamba Polymers earlier. i made a small tracking position in it last year. fundamentals look good and it seems cheap. I have couple of questions regarding companies like this:

How do you get more information about such companies when they don’t have regular concals and not much available on the web?

Trading volumes are very low and it’s easy to manipulate the price i think. most of the time, volume traded is in 100s. is it a risk?

There are more opportunities now vs in 2021 where it was much harder to find good value companies. In current market, I am facing more problems in deciding what not to buy as a lot of very good companies are trading at cheap valuations

Unfortunately, Shri Jagdamba doesn’t share much information with investors, even their annual reports do not have much details. One can try to look at other proxy sources of information like trying to figure out US residential demand, sales trajectory of their largest customer Epilay, etc. but its very hard to get much insights beyond what we already know. About liquidity, volumes in smaller cos dries out during bear markets. Its a feature meant to be used by investors rather than a bug.

In my observation, problem of information availablility is widespread in very small cos. My way of dealing with this is to allocate smaller positions and diversify extensively. Also, beyond a point I dont see the logic of tracking companies very closely. Having more data points has often not resulted in superior investing results for me, instead sometime I get an interesting insight and that simple logic helps me holding through a longer period of time.

For e.g. I have been buying Propequity recently where the only meaningful insight I have is, this is one of the few Indian cos with real estate data for last 15+ years. This data required investments of 70-80 cr., company’s enterprise value is around this number. Indian real estate data should be more valuable than 100 cr. I dont know if this logic sounds reasonable to you, but I feel this company’s market cap should be significantly higher than what its quoting at today (how much? I dont know). Side note: Propequity is the first company that Berkshire has partnered with for its real estate activities in India.

Have u ever gone through Kfin technologies? At what valuation you feel comfortable to enter it if at all you are interested… Comparing to CAMS size of Kfin is small, but runway looks bigger as they are expanding outside India also. Your thoughts would be very helpful and insightful.

Thanks

Reduced position size in Punjab Chemicals from 4% to 2%. This reduction is because of their share prices seeing a sharp drop and not due to my own selling. As we are coming off a huge agchem upcycle, I want to be more measured in buying as channel inventory is still at high levels and might require 6-12 months to clear. I still feel Punjab is one of the most promising bets with multiple drivers (sales growth, margin improvement, balance sheet improvement), but want to add further once I have better visibility.

Added 1% position in Shree Ganesh Remedies (SGRL) PP (rights issue shares). SGRL IPO’d as a SME co in 2017. In the next 5-years, their sales multiplied by 3.5x and PAT by 4.3x. SGRL manufactures intermediates for pharma and agchem cos. Their business model is to manufacture intermediates with small market size and high realizations which large players don’t want to manufacture, thereby giving them higher margins. SGRL has garnered 50% market share in their top 4 molecules which is very impressive for such a small company. Additionally, they are doing multiple capexes which should result in good growth going forward. What attracted me towards SGRL was their margins, which have been maintained at 24-25% even in this chemical downturn. I think this is indicative of their differentiated business model. I initiated the position at a small size due to high starting valuations. In addition, I have preferred buying SGRL rights issue shares (SGRLPP) as there is a 15% arbitrage between SGRL and SGRLPP.

Added 1% position in Propequity (P.E. Analytics). Propequity runs a website that shows historical property prices in different parts of India. Their main customers are banks, NBFCs, investors, and real estate companies. Recently, they have started a new business vertical where they provide valuation services for housing finance companies. In this vertical, they do due diligence on real estate properties and give valuation reports to the financing co, on the basis of which financiers can underwrite loans. Co has been growing fast and have a very long growth runway.

Recently, Propequity has also announced a partnership with Berkshire Hathaway Home Service, but not much is known about the deal terms. I guess this will be a real estate agency kind of setup. Valuations are very reasonable for the co, especially if one removes the 55-60 cr. cash they have on their balance sheet. I want to scale this position as I get more conviction in this idea.

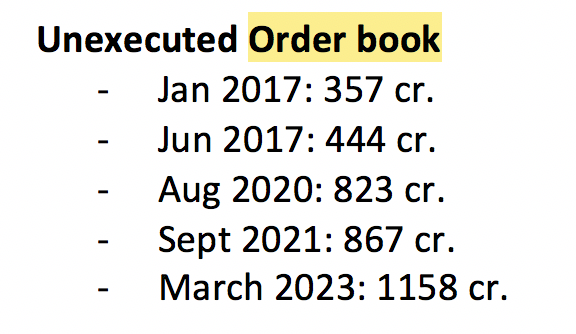

Added 1% position in RKEC projects in the deep value portfolio: RKEC does EPC work and has strong positioning in marine works. Their current order book is around 1150 cr. and their Mcap is 150 cr. About 5-years back, their Mcap was 400 cr. on an order book of 400 cr. Company is coming off a poor couple of years and disclosed very good results in Dec-22 quarter (~10 cr. quarterly PAT). I am hoping they are able to execute their order book in 2-3 years, which can give them annual PAT of 40-50 cr. On a Mcap of 150 cr., it becomes a very interesting bet.

Apart from these, I am also looking to add Mayur Uniquoters and Glenmark Lifesciences in the model portfolio, and want to increase position sizes in Transpek and Caplin Point. I need to think what I can switch out of. My current thoughts are to sell Control Print and Chamanlal Setia, as both have done very well in the past few weeks and are reaching cyclical high valuations. Any other suggestions?

Cash stays at 0 and updated folio is below:

Core compounder (41%)

Companies

Weightage

I T C Ltd.

4.00%

Housing Development Finance Corporation Ltd.

4.00%

NESCO Ltd.

4.00%

Eris Lifesciences Ltd.

4.00%

Ajanta Pharmaceuticals Ltd.

4.00%

HDFC Asset Management Company Ltd

4.00%

Aegis Logistics Ltd.

4.00%

Gufic Biosciences

4.00%

HDFC Bank Ltd.

2.00%

PI Industries Ltd.

2.00%

LINCOLN PHARMACEUTICALS LTD.

2.00%

Caplin Point Laboratories Ltd.

2.00%

P.E. Analytics Ltd

1.00%

Cyclical (51%)

Companies

Weightage

Kolte-Patil Developers Ltd.

4.00%

Sharda Cropchem Ltd.

4.00%

Avanti Feeds Ltd.

4.00%

Aditya Birla Sun Life AMC Ltd

4.00%

Alembic Pharmaceuticals Ltd.

4.00%

Amara Raja Batteries Ltd.

4.00%

Chaman Lal Setia Exp

4.00%

Stylam Industries Limited

4.00%

Ashiana Housing Ltd.

2.00%

Ashok Leyland Ltd.

2.00%

Kaveri Seed Company Ltd.

2.00%

Control Print Limited

2.00%

Sundaram Finance Ltd.

2.00%

Time Technoplast Ltd.

2.00%

RACL Geartech Ltd

2.00%

Manappuram Finance Ltd.

2.00%

Transpek Industry Ltd.

2.00%

Shree Ganesh Remedies Ltd - PP

1.00%

Turnaround (2%)

Companies

Weightage

Punjab Chem. & Corp

2.00%

Deep value (7%)

Companies

Weightage

Geekay Wires

1.00%

Jagran Prakashan Ltd.

1.00%

D.B.Corp Ltd.

1.00%

Shemaroo Entertainment Ltd.

1.00%

Modison Metals

1.00%

Suyog Telematics

1.00%

RKEC Projects

1.00%

Sorry I haven’t looked at Kfin. At current multiples, I prefer HDFC AMC over Kfin or Cams.

Hi Harsh,

Alembic has been there in my portfolio for above 8 years and you have rightly put it in the cyclical basket and I am holding on because they have this ability to spot once in a lifetime opportunity. I am tempted to sell because of their bad capex call and depressing commentary from the management, What is your thesis on holding on to this

Hi Harsh. Hope you are doing well.

What do you think about HDFC AMC’s current valuations? With a PE of 27 and a P/B of 7, it looks quite fairly valued. Do you think it would be good to double down and add at current levels?

Thanks for the reply…In regard to Punjab chemicals, I am planning to buy for the first time in the range of 725 to 750 and possibly it may come at any time as it is not interested to participate in recent “rally” in smallcaps. However I feel technically it will become buy near it’s previous all time high in the zone of 725 and valuation is any how will become attractive. Chamanlal I am expecting to reach 210+ before coming down significantly. So still holding it from my first buy of 110+ which we had discussed in same thread I guess previously.

Thanks

One of the things I observed on Ganesh Remedies was that the cash flow does not show payment of taxes despite provision for taxes in P&L, what do you make of it?

Punjab chemicals will have a good Q1 - they seem to be ticking right boxes. Sizing ur positions is apt but i still feel they have it in them as per the last concall they are getting inquires + plant visits. So in small caps like Punjab Chem this is one optionality that can play out any Qtr. Playing the probability here.