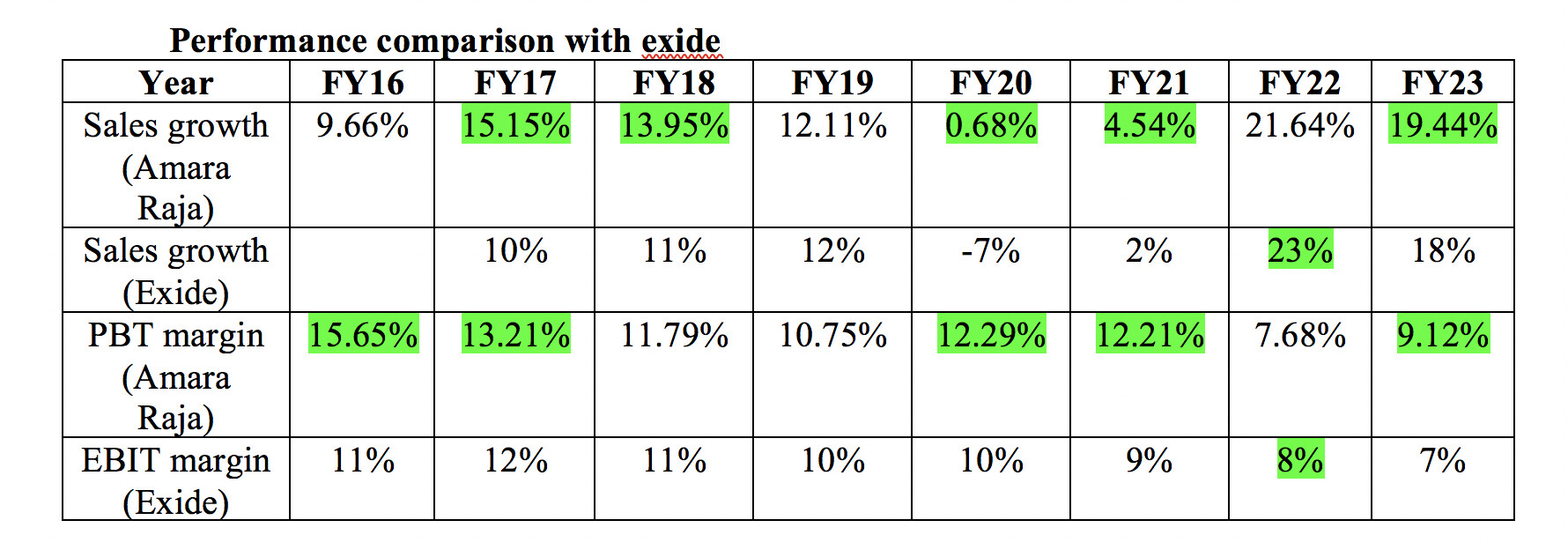

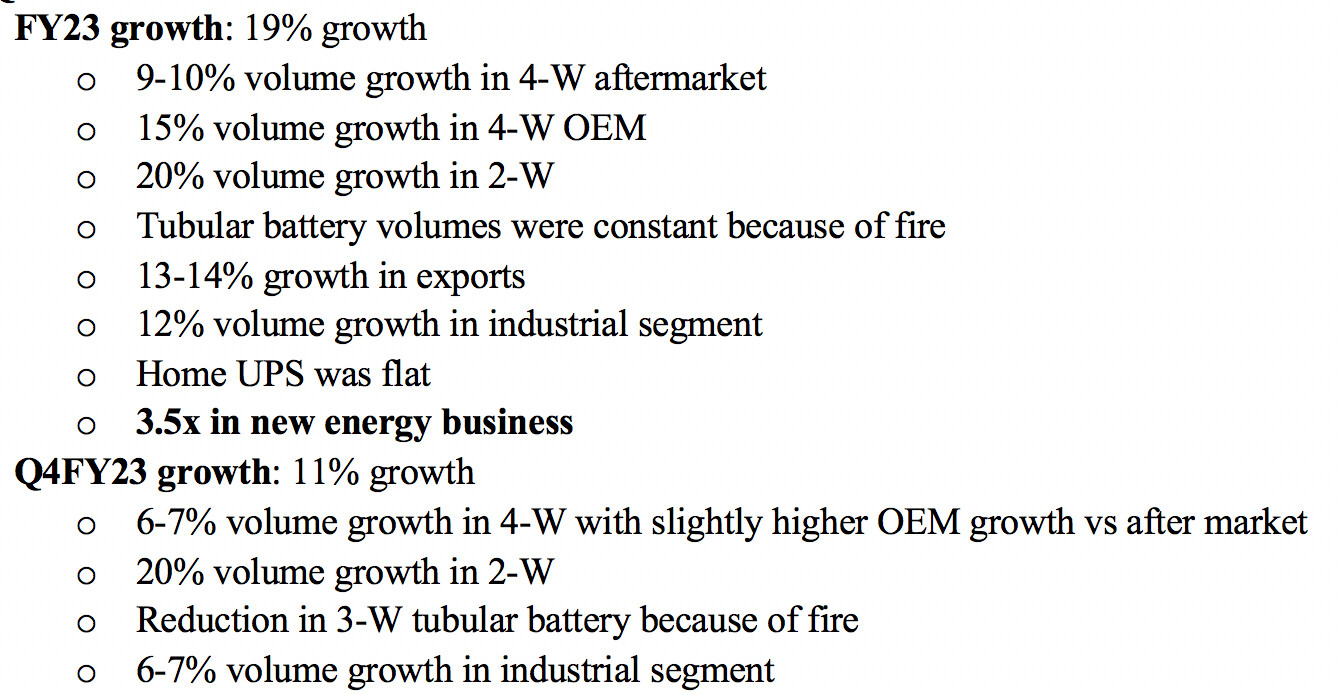

Mixed set of results from the co, the fire at their 3-W tubular battery led to muted growth. If we compare them vs Exide, they have done better in FY23 (both in margin and sales growth front).

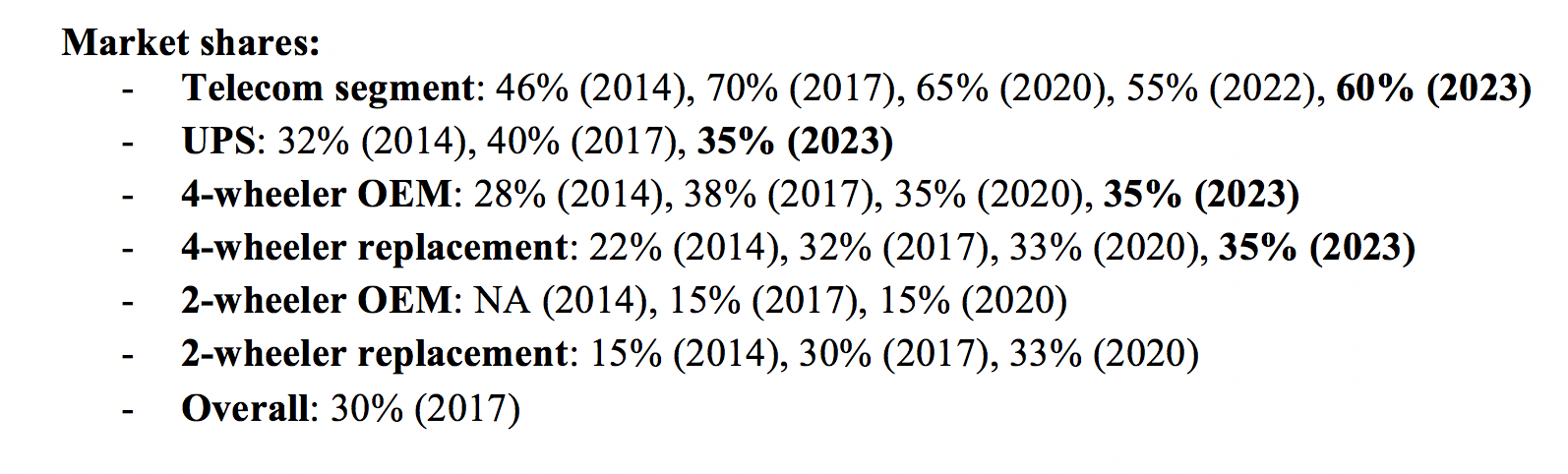

In the past few years, Amara Raja has made serious in-roads in 4-W battery (both OEM and after market) and has reached 35% market share. As the 2-W market has been largely flat in past few years, Amara Raja has done well in making in-roads with 4-W batteries. Additionally, they have maintained very high market share in telecom segment.

Most interestingly, Amara Raja has been very calibrated in spends in their lithium battery investments and can now completely fund the expansion from their own cashflows. They are generating close to 1000 cr. of cashflows each year, and plan to spend 400 cr. on both lead acid and lithium batteries each year for the next 3 years. This gives them 200-300 cr. of freecashflow which can be shared back as dividends or used for further expansion (like acquisition of Amara Raja Power systems or Mangal Industries).

On the negative side, lithium battery investments are really low ROCE as lithium battery packs generate 25% gross margins and work at asset turns of 1-1.2x currently. As lithium is largely imported, creditor terms will be unfavorable for the co and require higher inventory requirement. Even assuming a 120 day working capital cycle, ROIC comes in single digits. This has to change in the future, or Indian battery cos cannot be competitive.

Notes from concall below.

FY23Q4

- Margins: Gross margins have started reviving. Power costs were higher and should reduce due to commissioning of new power plant. Had higher employee costs as employees that were working in tubular factory (which caught fire) were kept on payroll. Hoping to get back to 14-16% EBITDA margin in lead acid division, but overall margins will be lower due to investments in lithium ion (13-15%)

- Will take 2.5 years in commencement of CQP and 2GW lithium plant and require 1300 cr. of investments (will use NMC technology). Investments will be spread over 2.5 years. Focus will be first on EV 2-W. Based on current prices, asset turns will be 1-1.2x

- Capex: 300-400 cr. for lead acid in FY24 and FY25. 300 cr. for new energy business in FY24 and 500 cr. in FY25

- Lead recycling plant will cater to 30% of lead requirements

- Have not taken price hikes in after market in Q4 due to recent lead price increase (it was not very high)

- R&D spends are 2-2.5% of sales

- Current capacity utilization is 90-93%

Disclosure: Invested (position size here, no transactions in last-30 days)