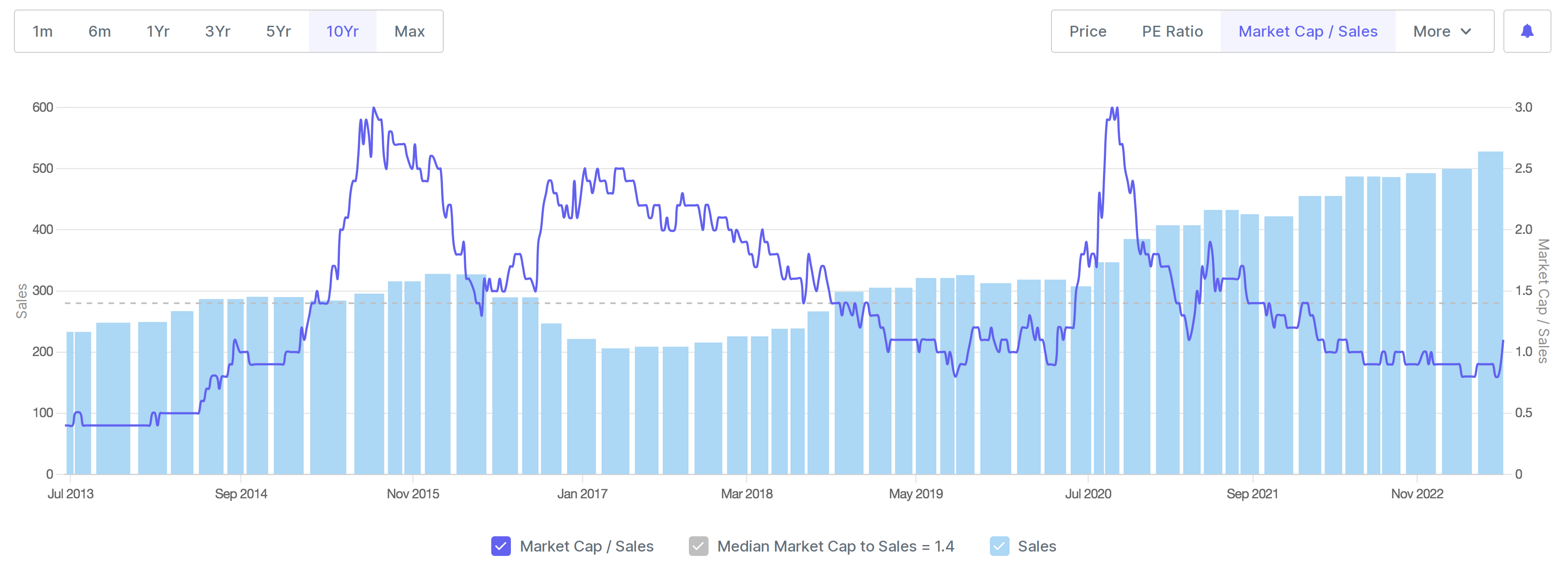

My logic is simple, Alembic has gone through a bad business cycle and its valuations (on EV/sales) is at pre-2014 levels. The idea in any cyclical business is to buy during bad times and hope for mean reversion. When it plays out, you want to sell to people who thinks this cyclical is now a structural opportunity. Sometimes, this logic works out, sometimes it doesn’t. So far, I have observed that it works out more often than not.

I have thought a lot about HDFC AMC and an appropriate benchmark, as there are very few business that dont require any capital to grow. The correct benchmark for HDFC AMC in my opinion is CRISIL and if we look at long term valuations of CRISIL, they tend to bottom out around 25x PE, except for the 2009 crisis when their valuations went down to 10x. So I feel reasonably comfortable holding and adding to HDFC AMC at current multiples.

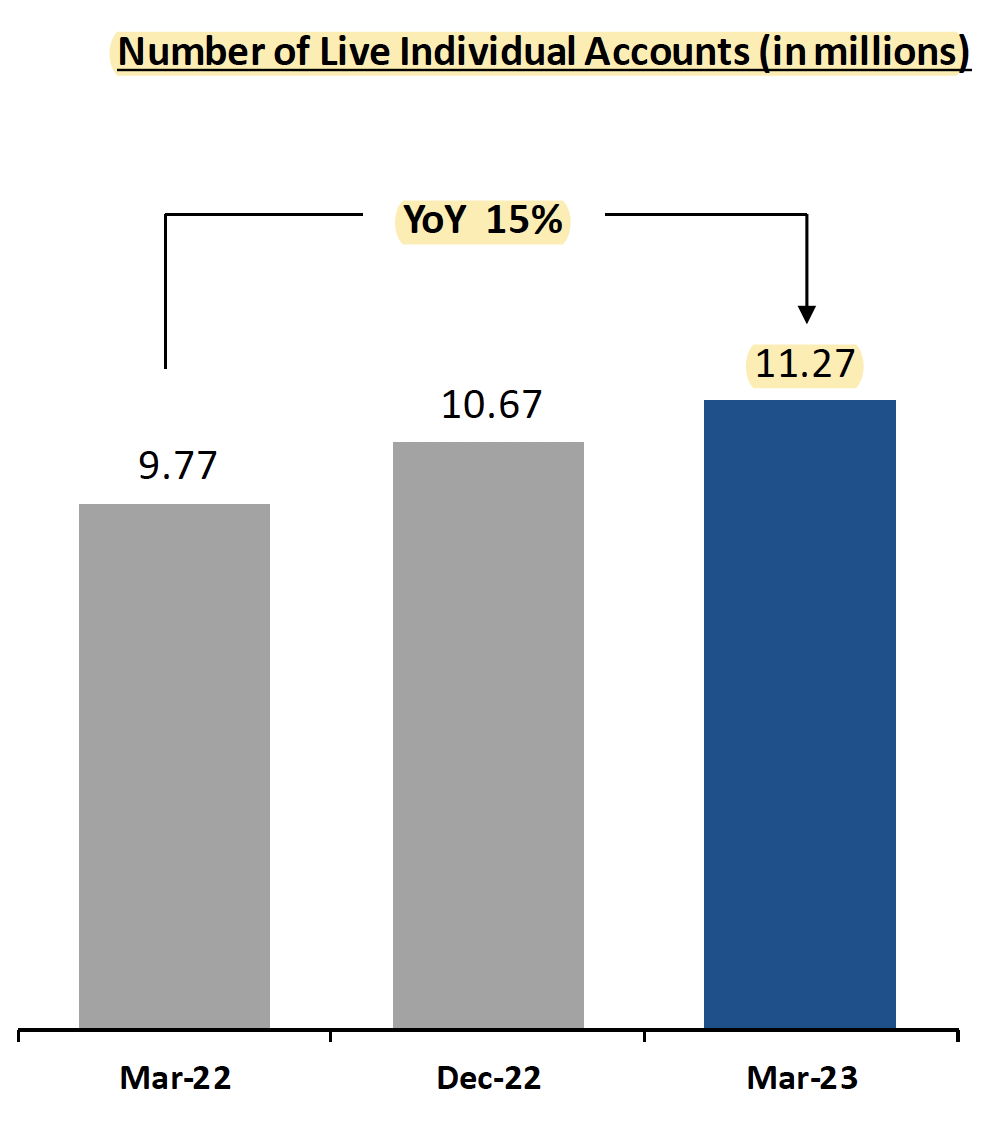

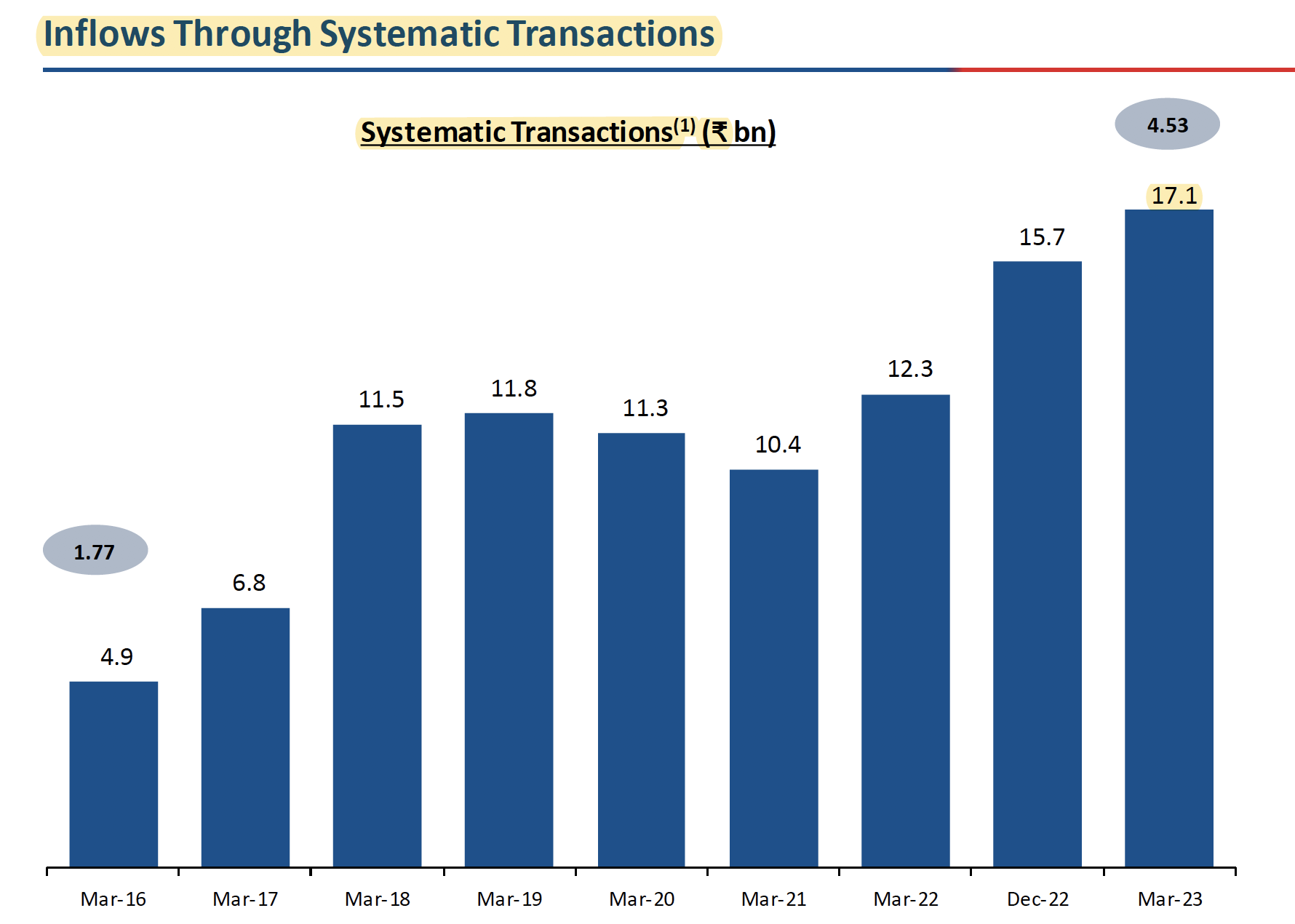

Also, if you look at presentation of HDFC AMC this quarter, the most encouraging trend is that number of individual accounts have increased by 15% and SIP monthly flows has grown by 39% in FY23. So business is back and management is doing the right things. Lets see how future unfolds.

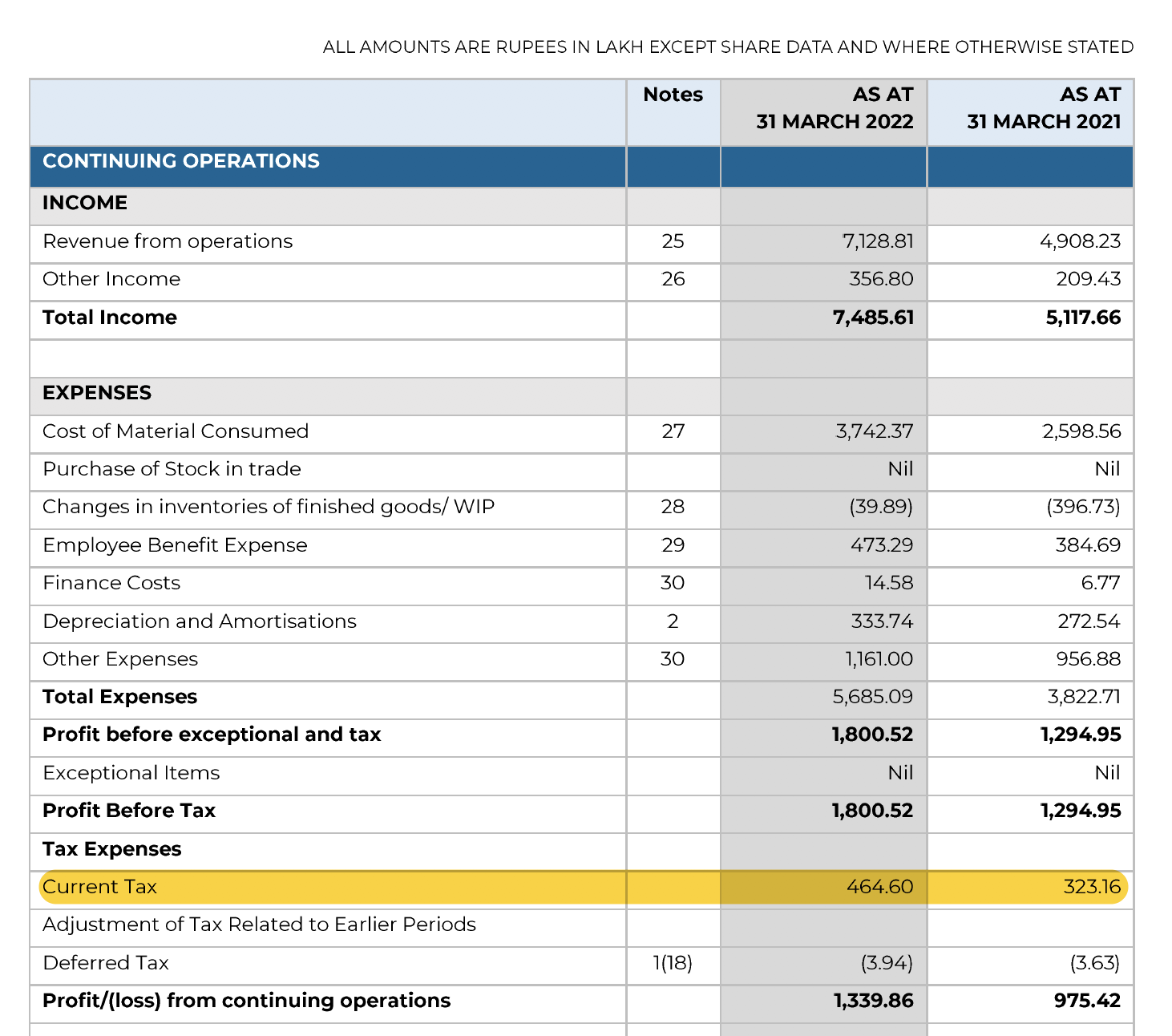

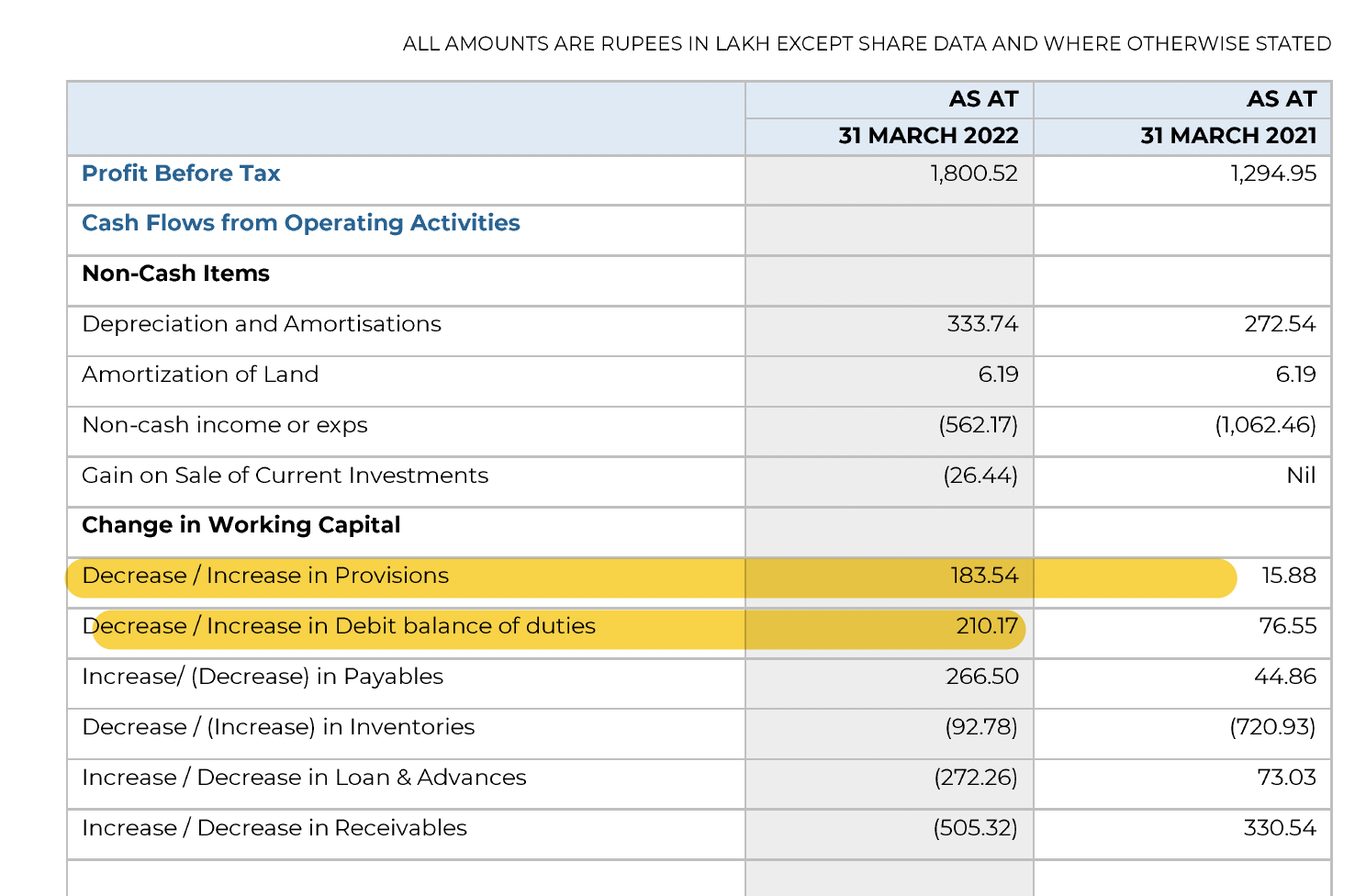

In the past, I have seen companies adjusting their taxes in working capital items and I think thats what SGRL is also doing. If you look at FY22 annual reports, they provisioned 4.65 cr. as taxes in P&L statement. In cashflow statement, if you add provisions and debit balance of duties it comes around 4 cr. I am not fully sure, but I think these two items are w.r.t. taxes paid.

However, this is a major doubt I had when I was doing accounting verification of the company. The way I came to terms with these was using two different sources:

-

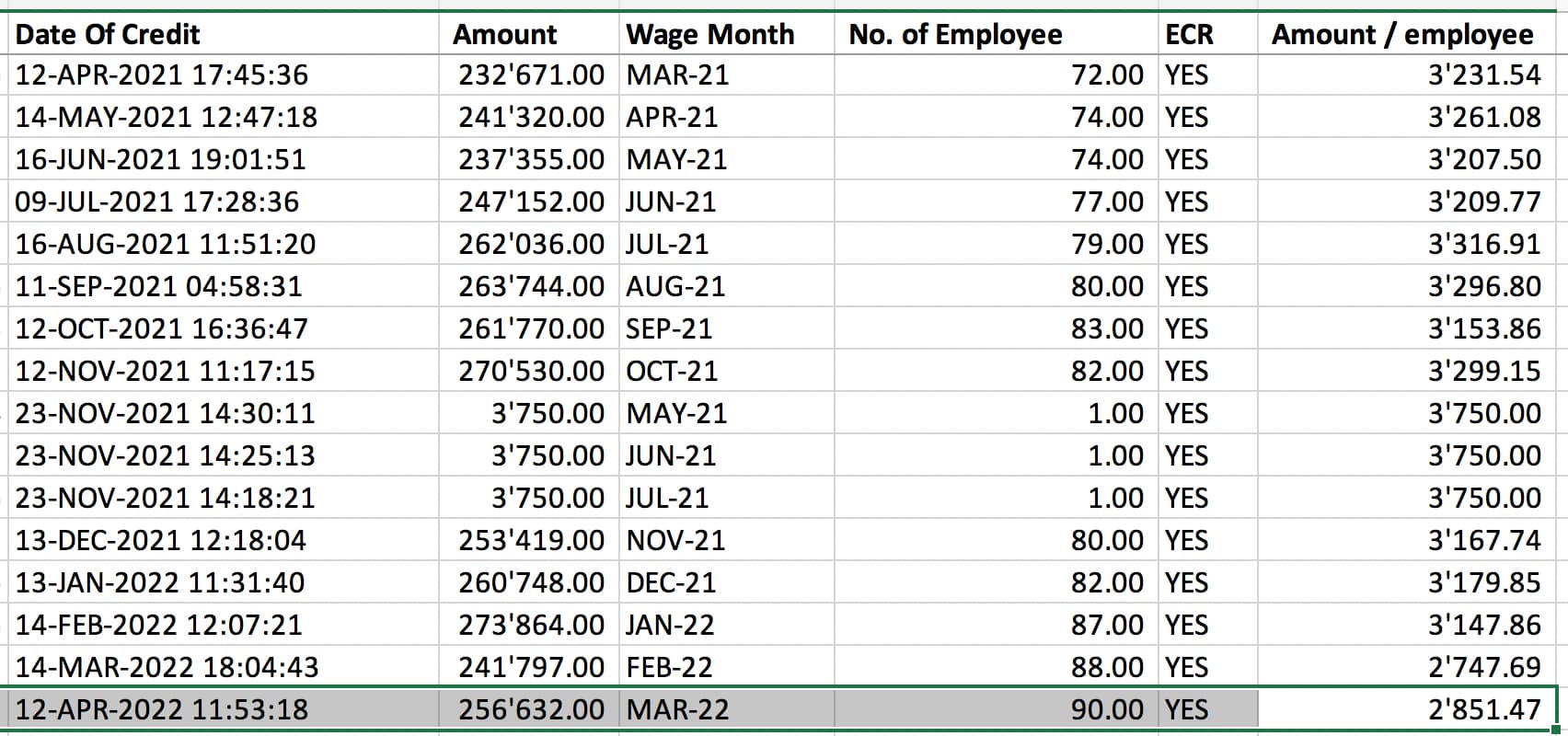

Their EPFO tax data broadly matches the number of employees claimed in the annual report, and they are regular in depositing these. In a lot of small companies, I have seen delays in depositing provident fund money which is not the case in SGRL.

-

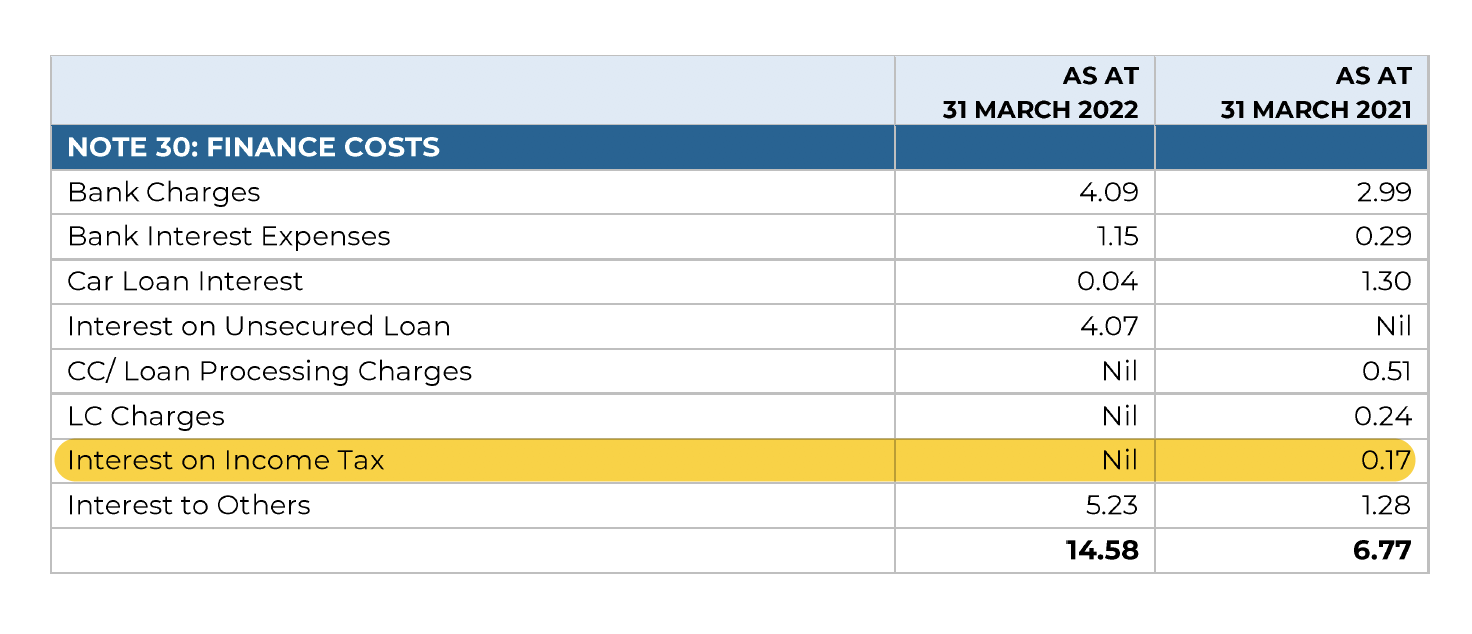

They didn’t pay any statutory fines on income taxes. Generally, when companies delay tax payments, they have to pay additional interest.

I agree, management guided in last call that growth will come back in Q1FY24.