A few good report from Systematix, I am sharing key insights.

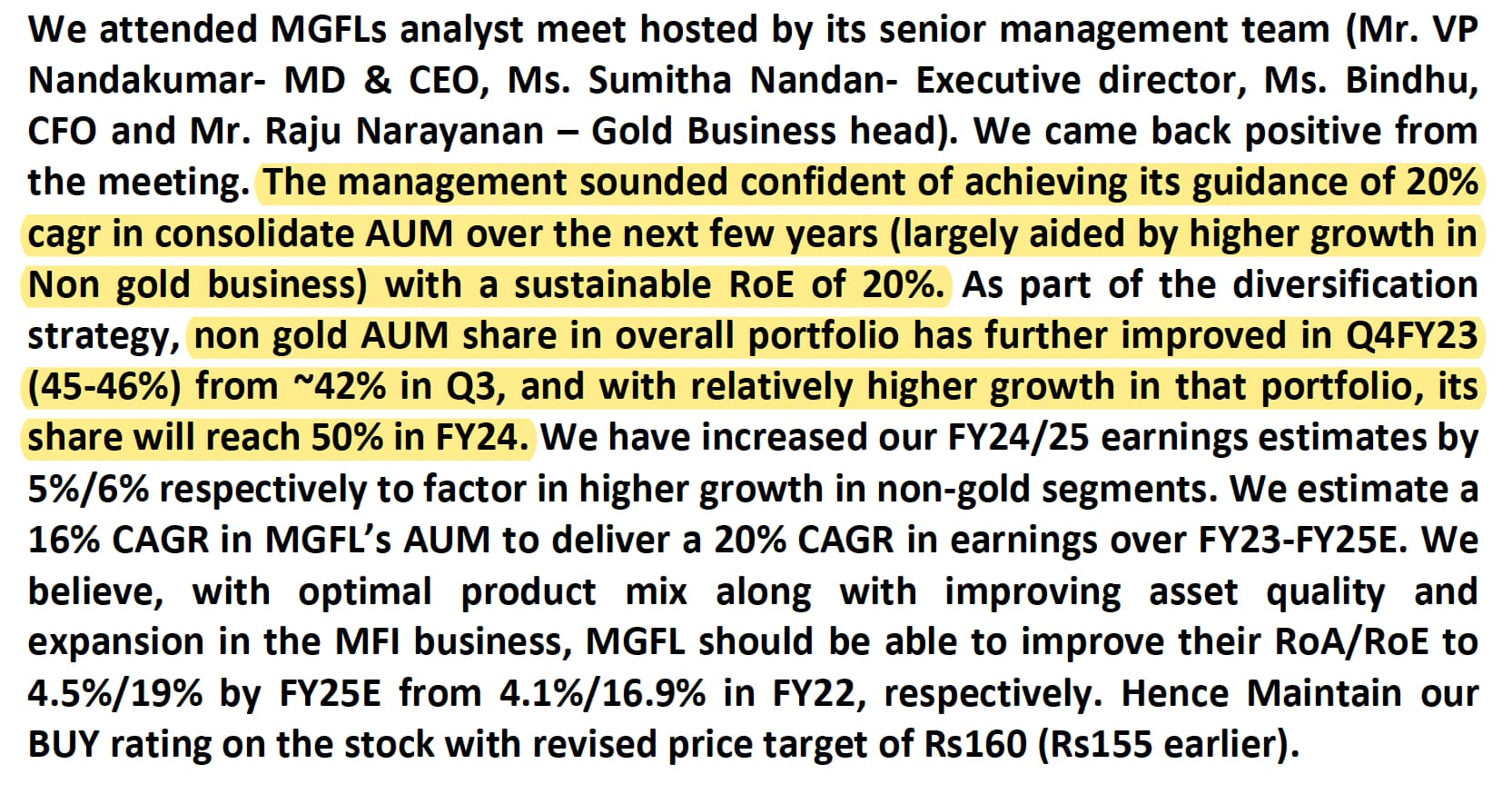

- 20% growth guidance at 20% ROE

- Sub-12% gold loans have completely run down. Gold loan yields is 21%, with incremental bank borrowing cost being 8.5-8.75%.

- Asirvad AUM has crossed 10k cr., implying ~25% QoQ growth. Growth is through new customer acquisitions. Manappuram will infuse 250 cr. into Asirvad and is also looking to raise equity capital of $100-125mn.

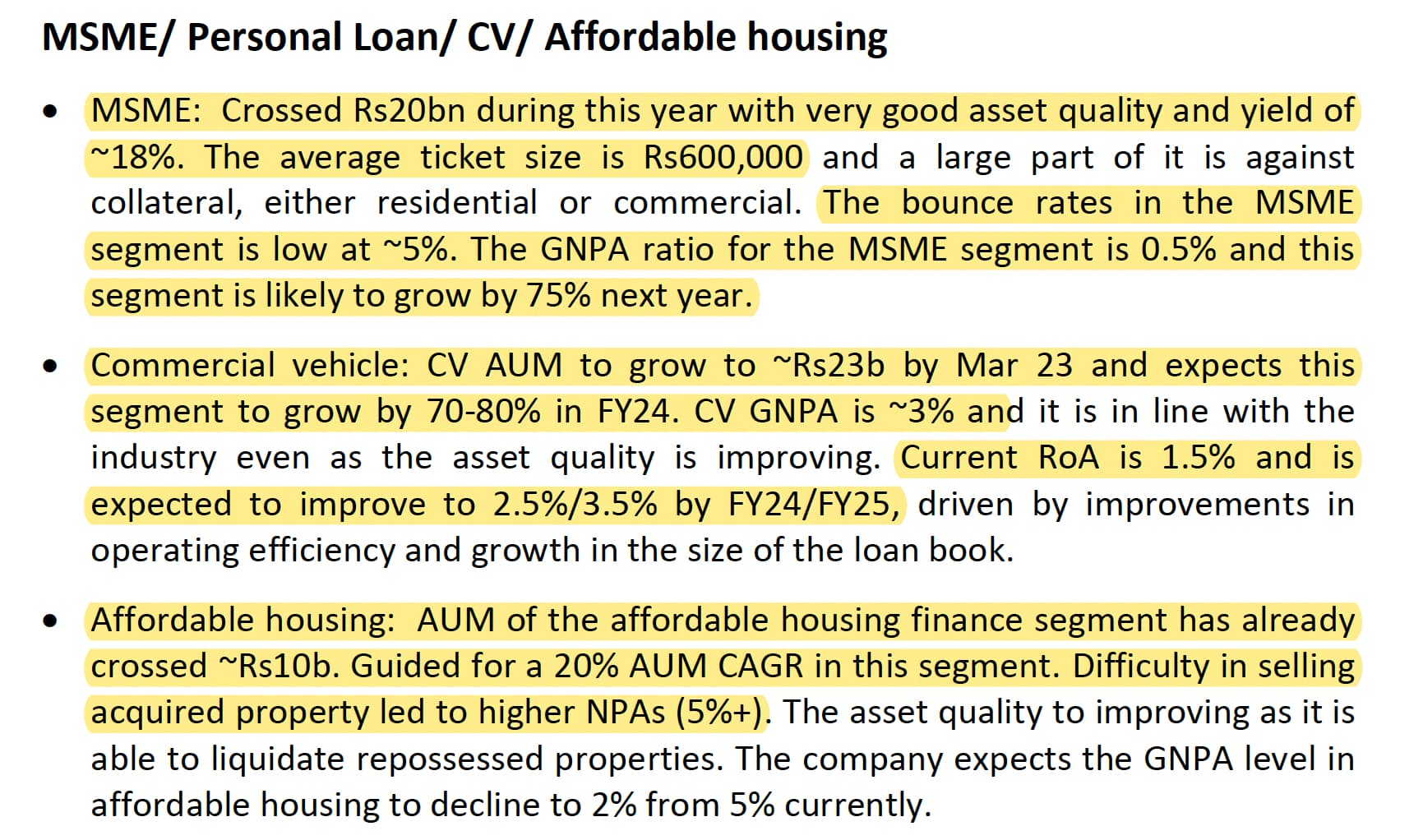

- Summary of other businesses

Overall, Manappuram is emerging as a diversified NBFC where their non-gold loan will contribute 50% of portfolio by FY24. The diversification journey embarked in 2015 will finally start bearing fruit, this is where I feel Manappuram has left Muthoot far behind.

Disclosure: Invested (position size here, no transactions in last-30 days)