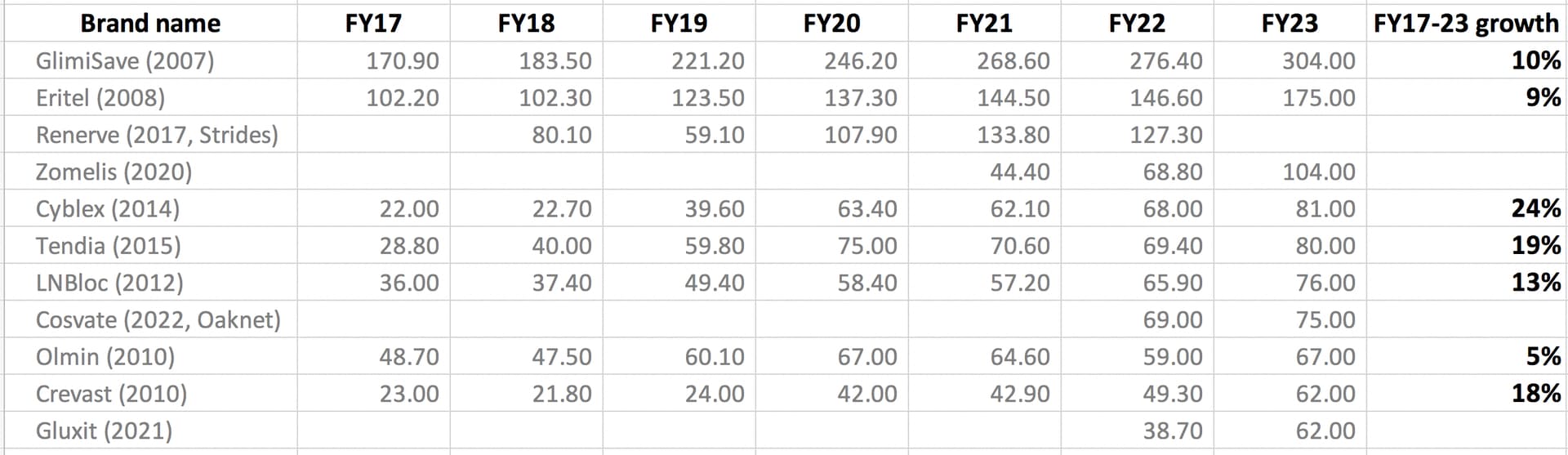

Muted set of nos continues for Eris, with organic growth at 9.5%. However, their big brands such as Glimisave, Eritel, etc. have finally started growing after a gap of 2-3 years. Management is very confident of recouping margins in FY24 and is looking to pay down 400 cr. of debt in FY24.

FY23Q4

- Organic revenue growth was only 9.5% due to discontinuation of Zac-D (covid product) and Zayo (legal issues). Ex of these, growth was 15.6% in FY23

- Spent 1265 cr. in dermatology acquisitions

- Clocked 17 cr. revenues in Insulin, should be EBITDA neutral in FY24. Q4 run rate was a bit lower due to supply issues

- Trade generics: Hoping to not incur loss in FY24, not focusing on growth in this segment

- Will give FY24 guidance at end of Q1 with more visibility on integration of Glenmark and Dr. Reddy brands

- Dermatology brands are currently outsourced, looking to bring in to Gujarat facility by end of FY24 (15% tax rate)

- FY24 ETR: 14-15%

- Intend to pay down 400-500 cr. debt in FY24

- Eris standalone metrics: 82% gross margins, 5L YPM and 38% EBITDA. Oaknet metrics: 78-80% gross margins, 5L YPM

- MR expansion: will setup 1 more division in dermatology in H2FY24 (~100 people)

- MR: 2200 (standalone) + 700 (Oaknet)

- Oaknet FY23 revenues (pro-forma): 250 cr. (booked 226 cr. for 10.5 months) and 61 cr. EBITDA

Disclosure: Invested (position size here, no transactions in last-30 days)