Sign up for mprofit…it will do the xirr tracking for you including dividend…

I have made the following changes in the model portfolio.

- Sold 2% position size in Cochin Shipyard and added Stylam Industries as a cyclical bet

- Switched 1% position size in Atul auto with Geekay wires in deep value portfolio

Stylam: They have grown very well in past few years, reduced debt by selling non core IT business and are now building a branded B2C business. Valuations are in fair range, so upside will be because of good sales growth and margin revival to 16-18%.

I got interested in Stylam because of their continuing export growth because of penetration into newer markets such as Saudi Arabia, which has differentiated their growth trajectory vs other building material cos like Carysil. Additionally, Stylam is getting more aggressive in domestic market.

In terms of margins, despite having 20% lower realizations vs market leader Greenlam, Stylam has higher operating margins due to integrated nature of operations. If their branded business in India succeeds, it will be a huge margin boost for them.

Geekay wires makes steel wires and nuts and sells them in USA. They have shown tremendous growth in past few quarters (50%+ growth in past 6 quarters) and are trading very cheap (6x PE). There are 2 issues which I could identify with the company:

- They sell in US through a promoter owned subsidiary

- They have an ongoing anti dumping duty probe against them in USA.

This combined with them being very small in size (70 cr. Mcap), I have limited its position size, but am happy adding it as valuations are very cheap given their growth profile. Lets see how future unfolds.

Updated portfolio is below. Cash stays at zero.

Core compounder (42%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Shri Jagdamba Poly | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Godfrey Phillips | 2.00% |

Cyclical (48%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Chaman Lal Setia Exp | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| Suyog Telematics | 1.00% |

I have answered this in the past (links below). Alembic Pharma can be a beneficiary of an upcycle in the US generic market due to their very large capex, which is now getting approvals from FDA. To give some context to the size of Alembic’s ANDA pipeline, only Aurobindo files similar no of ANDAs annually and they are almost 10x bigger than Alembic Pharma. If growth comes, delta in earnings will be the highest for Alembic vs peers. Also, currently there is a shortage of anti biotics in US due to flu season which should benefit Alembic temporarily. Lupin and Ajanta should be larger beneficiaries, but Alembic will also benefit from this.

Its actually quite simple. Just compute your monthly returns using formula below and keep benchmarking yourself against peers (MFs, Nifty and PMSs).

11 Likes

Harsh sir, a very naive question. Whether the weightage is calculated based on the original cost or current value? And how do you keep exact percentage when a particular scrip moved faster than other portfolio companies. Do you exercise balancing it on with a particular time-frame.

3 Likes

Hi Harsh, I am curious to know, why you have so may stocks with such small allocations in your PF. Is it not that too many stocks average out the performance and result in performing more or less similar to good mutual funds. I understand the thrill in picking individual stocks oneself but I feel with your stock picking abilities, you can do better with 8-10 stocks.

1 Like

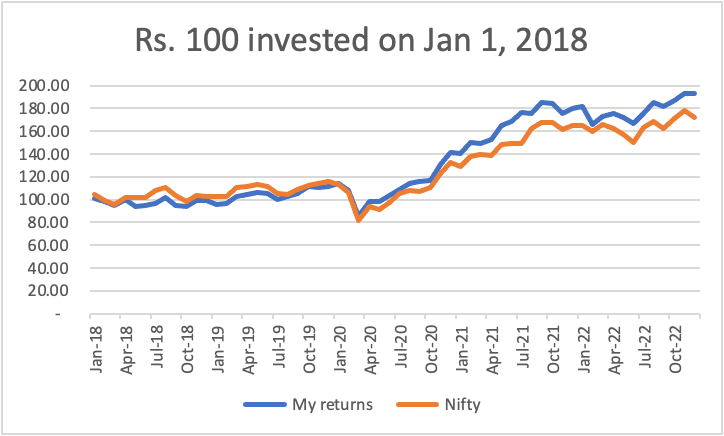

Its been 5 years since I have maintained my investing records, the performance according to calendar years is shown below.

| Calendar year | My returns | Nifty returns | 100 invested in Harsh folio | 100 invested in Nifty |

|---|---|---|---|---|

| 2018 | -0.63% | 3.15% | 99.37 | 103.15 |

| 2019 | 11.83% | 12.01% | 111.13 | 115.54 |

| 2020 | 27.18% | 14.89% | 141.33 | 132.75 |

| 2021 | 27.30% | 24.12% | 179.92 | 164.76 |

| 2022 | 7.26% | 4.33% | 192.97 | 171.89 |

A more granular performance (on monthly returns) is shown below.

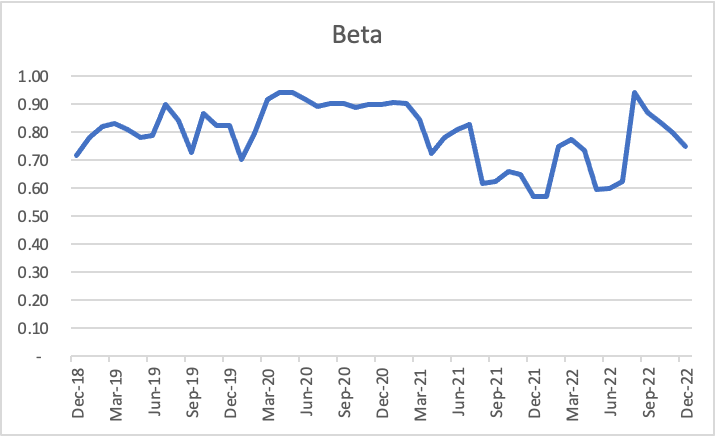

I have managed to outperform nifty over this period, with CY20 being the year with maximum outperformance and CY18 being the year with maximum underperformance. I also track other features of my portfolio. My portfolio beta has consistently stayed below 1 (computed on monthly data with 1-year lookback).

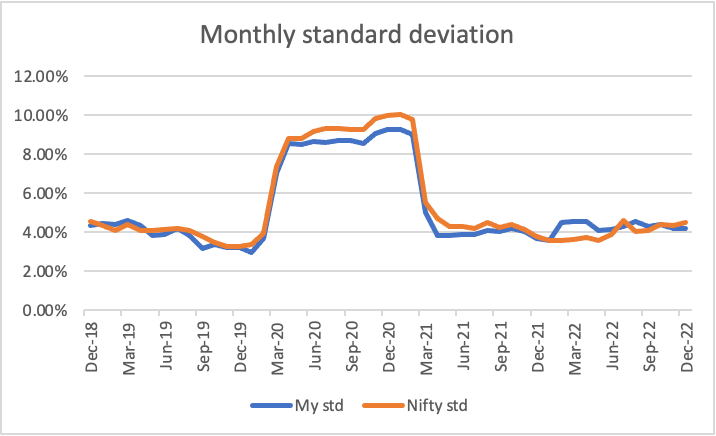

This is mainly because of increasing divergence of my returns with Nifty returns as a result of more bottom-up stock picking. This is clearly shown in the standard deviation chart, where my portfolio’s std has increased over time.

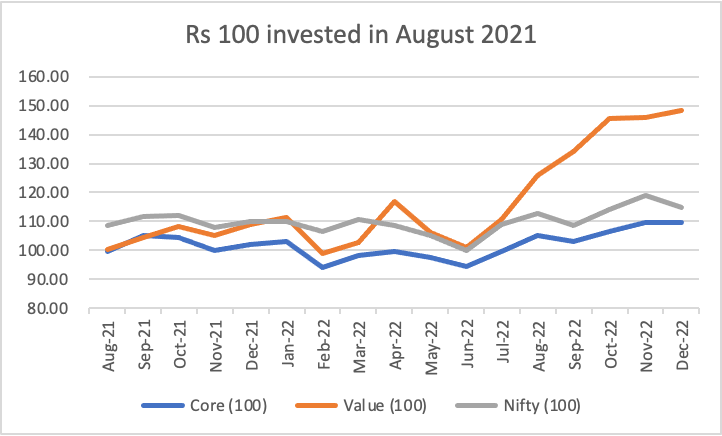

Deep value performance

Since August 2021, I started a new strategy (deep value bets) which has done exceedingly well.

Returns have been very high in past few months, as its components mostly include microcap value stocks, which swing more (higher upside during good times & vice versa). 2022 has been a mean reversion year, so its natural that a deep value strategy will do well. Lets see how 2023 pans out.

I wish everyone a lot of success in all their endeavours and a very happy new year ![]()

79 Likes

Hi Harsh,

Wish you a very happy new year and all the prosperity with it!

It’s so nice to see such a wonderful application of statistics and more so the discipline to keep the records necessary to facilitate that. I want to add a small idea to the mix:

How about instead of using Nifty as the benchmark, you categorize the stocks you hold (let us say based on their market cap) and recalculate the same set of KPIs in comparison to their respective benchmark indices?

Thanks

Arnab Roy

2 Likes

At the outset, I wish to thank you for sharing such detailed analyses with us.

Mind sharing the avg buying cost per share along with the % contribution to your Portfolio?

Thanks

Ramanjan

3 Likes

Its at CMP, I let weights vary ± 2%. Beyond that, I rebalance.

I have written about this numerous times, it feels like repeating the same answer over and over again. You can search through this thread to understand my thoughts on diversification. My performance (excluding dividends) has been in the top quartile of all MFs over my investing period, despite having such a diversified portfolio. So, I do not see a point to these discussions, as they are not value additive.

Good point. It requires a lot of effort to benchmark each stock against the appropriate index, and I dont see the upside of doing this. Nifty is the actual opportunity cost for me as it is very easily accessible in a low cost manner.

As I have mentioned before, I have three benchmarks: Nifty, Banyan tree PMS, Mittal analytics PMS. I have managed to do better than the first two, but have underperformed the third.

I can share it, but I dont see the rationale for doing that as I keep on rebalancing regulary to take care of weightage. As a result, in a lot of positions my actual invested capital (net of redemptions and dividends) is negative. Also, I keep on booking losses regularly to offset capital gains which again skews the average price.

Today’s allocation at CMP is the only thing that matters, everything else (like what price I bought it at) is just an academic exercise.

9 Likes

Hello Harsh… Would you be able to advise on the rationale for Godfrey Phillips?

I was earlier invested in this company for their 24/7 convenience stores which could be a big thing…

However when I learn about the management and the absconding Nirav Modi and family were promoters, I sold it entirely.

I would like to know how much wieghtage would you put on management and governance?

Also would appreciate the rationale for Jagran Prakashan, my understanding is that its a dying business and its terminal value is something I cannot evaluate…

Thanks in advance

1 Like

Hi Harsh, About Chamanlal thesis, can you please share the source/pointers indicating below mentioned management intentions

With regards to sales growth

But on screener, I noticed the sales growth not being around 50% YoY. Did you mean the total sales growth from 2014 to 2018?

Irrespective of the clarification above points, a company with ~680 Cr market cap, 258 Cr cash in hands, better return ratios than industry leader (due to asset light business model) available at below 8 PE with positive industry tailwinds (clearly indicated by KRBL management in their media interactions and concalls) - A clear opportunity in terms of risk-reward.

Thanks

-Manohar

1 Like

Godfrey Phillips’ promoter is not Nirav Modi. For understanding family dynamics, please go through the Godfrey thread.

If you look at volume nos of Jagran or DB Corp, you will realize that this business will be here for atleast the next 5-10 years. And because people do not want to look at these ideas, pricing is very attractive. As a result, my own IRRs in both have been in excess of 30%, despite all kinds of narratives against newspaper cos. I am happy taking these kinds of bets again and again.

No I meant the sales growth in years 2014 and 2018 (look at screenshot below).

I agree!

1 Like

Hey Harsh,

I was looking at this company today,

Business is growing at high rate, but I see a problem with it.

- Demand of working capital can not be entirely fulfilled through internal accruals and there is limited scope to increase debt as Interest coverage ratio is low, so equity dilution is the way going forward I think.

- Dividend shall go to zero as company will not really have any free money to distribute.

- Lots of other income come from gov. schemes and FX, if any changes happen to that then business valuations may come down overnight. Possibility is low, but it is still a risk. FX can vary.

Its a good thing that you allocated just 1%.

Would like to know your views.

3 Likes

Hi Harsh,

May I dare to ask if this performance of yours is before or after taxes, fees and frictional costs?

Regards,

M

As of today, I have switched out of Shri Jagdamba Polymers and utilized the proceeds to buy more shares of Stylam. As a result, Stylam’s position size increases to 4% in the model portfolio.

The reason for exiting Shri Jagdamba is that they will likely be adversely impacted from the current US real estate downcycle. Also, their capex is still sometime away. On the other hand, Stylam has multiple earnings driver (export + domestic + margin improvement). I find the risk reward more interesting in Stylam, and hence the switch. Cash stays at zero.

Core compounder (40%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Godfrey Phillips | 2.00% |

Cyclical (50%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Chaman Lal Setia Exp | 4.00% |

| Stylam Industries Limited | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Heranba Industries | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| Suyog Telematics | 1.00% |

These are valid points and I agree with most of them. However, the way I approach microcaps is slightly different. If there is anything attractive that I find available at a very small market cap, I do some basic work and build a small position if things look reasonable. The idea is not to have a rigorous checklist, otherwise it becomes very hard to buy anything at such a small market cap. In the past few years, this approach has worked out very well for me.

Coming to Geekay, I was attracted by growth and reasonable dividends. While the core business is not great as reflected in mid teens ROCEs, the high working capital and poor cashflow generation is due to very low payables (and not high receivable days). That means, sales are probably not fictitious. Also, we can verify their sales with export data.

Low payable days is generally a strategy to get cash discounts, resulting in higher margins. However, if they keep growing like this, they will need to do equity dilution. Lets see how this plays out.

All the records that I share is pre frictional costs and also pre dividends. Actually, my dividend yield is much higher than the index, as I keep 10-20% of my portfolio in high dividend yield cos. As a result, dividends more than pay the frictional costs.

14 Likes

Hi Harsh bhai, could you please share your reasoning behind choosing PI over UPL? Valuation wise does UPL look a better option over PI if I take fresh entry in any one of them?

I have gone through your analysis on Punjab Chemical and UPL is one of their major clients, so if I have to shortlist two stocks from Agrochem space what would those be, Upl,PI or Punjab Chemical considering current valuation?

PI is a very old position, it has continued growing over time and has shown clear leadership in their core business. Over time, I have reduced my position size due to higher valuations. However, I have not sold out fully as growth is still very high and I want to be more measured in selling. UPL is in a very different lifecycle as its a mature company and can have limited growth. Given their size, they have done tremendously well to still keep growing. None of their global peers grow at these rates.

This being said, I think a better way to play UPL growth story is to buy Indian vendors that cater to UPL, as their individual earnings growth will be much higher. A lot of agchem growth observed in Indian companies is due to UPL outsourcing more volumes to these players. Hope this clarifies my thought process.

17 Likes

As of today, I have switched out of Heranba and replaced it with Caplin Point Laboratories. Cash remains zero.

Heranba reported a howler in this quarter which was due to pricing pressure in pyrethroids. We have gone through a very good agchem cycle in past few years, so mean reversion is likely to occur. In my experience, when earnings start dropping at such rates, it takes quite sometime for things to fall in place. With this in mind and due to many more available opportunities, I booked my losses despite valuations being very cheap.

Caplin Point has been one of the most consistent growth companies over the last decade. In the past few years, they have started building their US business which is scaling rapidly. One of the most common playbook to build US generic business is to get into products with small market size, some niche and grab large market shares. In the past few years, this playbook has been successfully implemented by Ajanta Pharma and Unichem Lab. With this strategy, companies scale to $100mn annual run rate in 3-5 years. Caplin is adopting the same playbook, lets see how well they can execute. Its available at 15x PE and I expect earnings to grow at 15%+ over the medium term. Historically, they have grown earnings at 25%+.

Other than this, I am building positions in RKEC projects and Propequity. Once I have built my positions, I will add them to the model portfolio. Currently, I am facing the problem of too many opportunities, its hard to decide what to sell.

Core compounder (42%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Godfrey Phillips | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

Cyclical (48%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Chaman Lal Setia Exp | 4.00% |

| Stylam Industries Limited | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

Turnaround (4%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 4.00% |

Deep value (6%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| Suyog Telematics | 1.00% |

16 Likes

@harsh.beria93 Do you track Krsnaa Diagnostics. I think that might fall in your (shallow?) value bucket. You might think of replacing Ashok Leylands with this. Pardon, I don’t track Ashok much but seems to be at near peak valuations. Thanks.

1 Like

Have you thought of adding grasim inds to your portfolio?

Modison Metals is facing huge margin pressure, with EBITDA margin dropping from 8% to 1% mostly due to inflation in raw material prices.

Where do you see the company stand in next 1-2 years and would they be able to grow in the same manner as they used to from 2020-22.