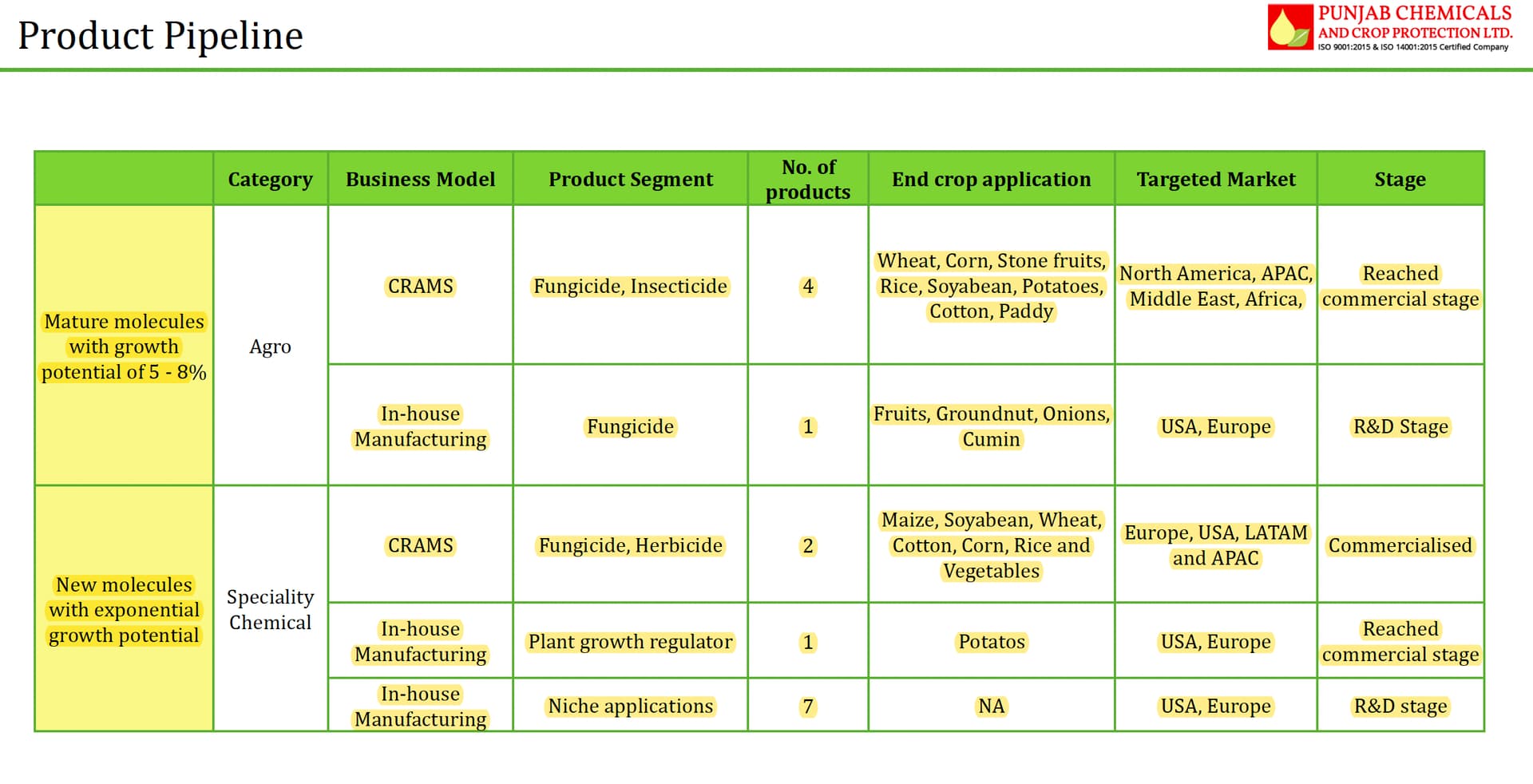

Company came out with a howler. Although nos look really bad, there were some interesting insights in this call and presentation. For the first time, thay talked about their product portfolio in the presentation.

They also talked about their recent hirings and how they are trying to professionalize the company with hires from large agchem cos (have highlighted relevant details).

Another interesting development was installation of MVRE plant this year. Although, this doesn’t add to production capacity, its very important for the kind of business model Punjab is targetting.

Now coming to the reasons behind such a howler in sales and why there were lots of questions around Metamitron: There are 2 companies from India who make Metamitron at scale, Punjab Chemicals and Hemani. Punjab controls 65% of market and Hemani controls the remainder (talking about technical market). The main difference between the two is that Punjab supplies to ADAMA and UPL on a contractual basis (ADAMA/UPL control the end formulation market), whereas Hemani supplies on spot basis. In past few months, it seems Punjab hasn’t been able supply this molecule and people have been worried if Hemani got into some contract relationship and displaced Punjab. Management categorically denied this on the call and attributed low sales to large inventory pileup at UPL/ADAMA’s end which is getting liquidated. Additionally, they guided that Metamitron volumes in FY24 will be equivalent (or maybe more) vs FY23. This molecule is the largest contributor to Punjab and thats why its so important.

If we remove Metamitron, Punjab has done very well in all their other export molecules, which is why exports only showed a 15% decline (vs 35% decline in domestic sales) .

More interestingly, Punjab has been able to gain market share in Diflufenican in LATAM, and are now expanding capacity from 300 tons to 800 tons. This is the molecule where they were facing stiff competition from Chinese peers and had to drop prices to gain market share.

In terms of importance, Metamitron, Metconazole and Diflufenican are the 3 main molecules for Punjab and contribute almost 50% to their sales.

One major negative for me was order book reduction to 1200 cr. In FY23Q2, they had mentioned that order book had increased to 2500 cr, but it seems to have been reduced by half. My concall notes are below:

FY23Q4

- 20% volume growth in FY22 and no volume growth in FY23

- Overall drop in sales is because of lower domestic demand + inventory correction in Europe

- Indian sales will recover in Q1FY24 and Europe will recover by Q2FY24

- Industrial chemical performance has been very steady

- Have seen demand slowdown in pharma business. Pharma intermediate hasn’t been commercialized due to inventory correction at customer end

- Energy prices have been high (high rice husk prices), have started investing in alternative sources of energy

- Herbicide: have got approval for Australia + certain countries in Europe (should get full approval by January 2024) – is this prosulfocarb?

- 4 products: 1 KSM commercialized, 1 agchem for Brazil will be commercialized in September, 1 will take time and 4th one (intermediate) is delayed

- LATAM product (Diflufenican): Have reached 55-60% market share in Argentina. Main competitor is Chinese

- Metconazole: Capacity is fully utilized

- Metamitron: Inventory correction is getting over, similar or higher volumes in FY24

- Added one fungicide (12 step process). Delivered 20 tons to market and it has potential to ramp up to 200-300 tons

- New products have at least 5-7 step process

- Focusing on bromination chemistry (azole range of products)

- Order book tapered down to 1200-1300 cr. but will increase by 1500 cr.

-

Capex:

o Capacity addition is mainly for a herbicide (probably Diflufenican; from 300 tons to 800 tons/year). Hoping to double sales this year

o Capacity addition: Derabassi: 2000 tons/year, Lalru: 1000 tons (for an intermediate) - 18-20% EBITDA margin will be achieved after FY25 with ramp up of newer products, target for FY24 is 14-15% EBITDA margin

- Complete leadership team has been built in last 2-years, EHS processes have been strengthened and investing more in R&D

- Dr. Vijay Kaushik (ex Bayer, Meghmani, PI) has recently joined as head of R&D

- Receivables look high because there was large sales booked in March

Disclosure: Invested (position size here, no transactions in last-30 days)