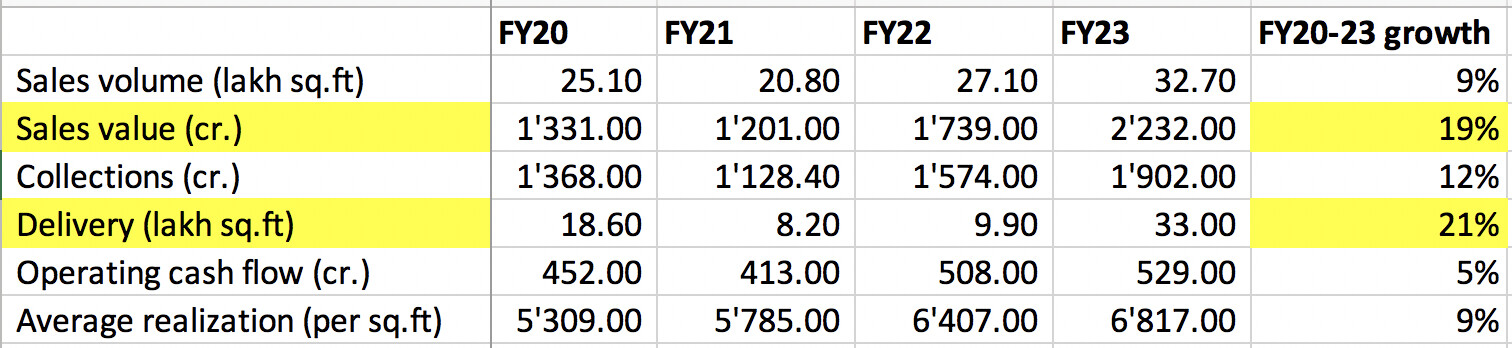

FY23 ended as a very good year with presales growing by 28%. One place where they lacked was in new launches, which was much lower than earlier guided and reported margins (again much lower than previously guided). However, since FY20 company has scaled up very well, with presales growing at 19% and company consistently generating very high cashflows (500 cr.+ in last 2 years). Realizations have also grown at 9% CAGR over this period.

FY23Q4 concall notes

- Pre-sales increased by 28% to 2232 cr. (50% came from new launches), volumes increased by 21% to 3.27 mn sq.ft and collections increased by 21% to 1902 cr.

- Delivered 3.3 mn sq.ft (exceeding guidance of 3mn sq.ft) but EBITDA margins were sharply lower at 13% (vs guidance of 25%). Lower margins are because revenues that are getting recognized are on a 5300-5400 realization (older projects) whereas marketing costs that are reflected in P&L statement are getting incurred on current projects which are being sold at 6800-7000 cr./sq.ft

- Launched 3.05mn sq.ft of projects (2120 cr.) which was much lower than guidance of 4000 cr. in FY23

- FY24 guidance: Pre-sales of 2,800 cr. + deliveries of 3mn+ sq.ft (1500-1700 cr.) + launch 7.39 mn sq.ft (5,265 cr.) + acquire projects with topline potential of 8,000 cr. (5000 in Pune + 2000 in Mumbai + 1000 in Bangalore)

- In May 2023, acquired two projects each in Pune and Mumbai with top-line potential of 2500 cr.

- Sustenance Inventory: 1700-1800 cr.; 30-40% of FY23 sales will come from sustenance inventory (~1000 cr.) and 60-65% from new launches

- Received 206.5 cr. from Marubeni Corporation towards investment in the Pimple Nilakh project in April 2023

- Business development: Net debt is 110 cr., need 500-550 cr. for current business development which they want to fund via internal accruals

- Life Republic contribution in pre-sales was 1.76 mn. sq. ft (1070 cr. sales). Currently RERA launch inventory is ~1000 cr. in township. Price realization has improved to 5700-5800/sq.ft

- Strategy in Life Republic during FY23 was to do high volumes, now with that strategy being successful pivoting to selling at higher realizations in Life Republic

- Have seen 5-10% higher realization across projects

- Margins & IRR: Outright projects (30-40% gross margins, 20-25% EBITDA margins), JV & Redevelopment (focus on IRR of 30%+)

- Have been seeing higher demand in higher value housing rather than low and affordable housing

- Customer profile: IT segment for entry level, beyond 1cr. inventory its spread across industries

Disclosure: Invested (position size here, no transactions in last-30 days)