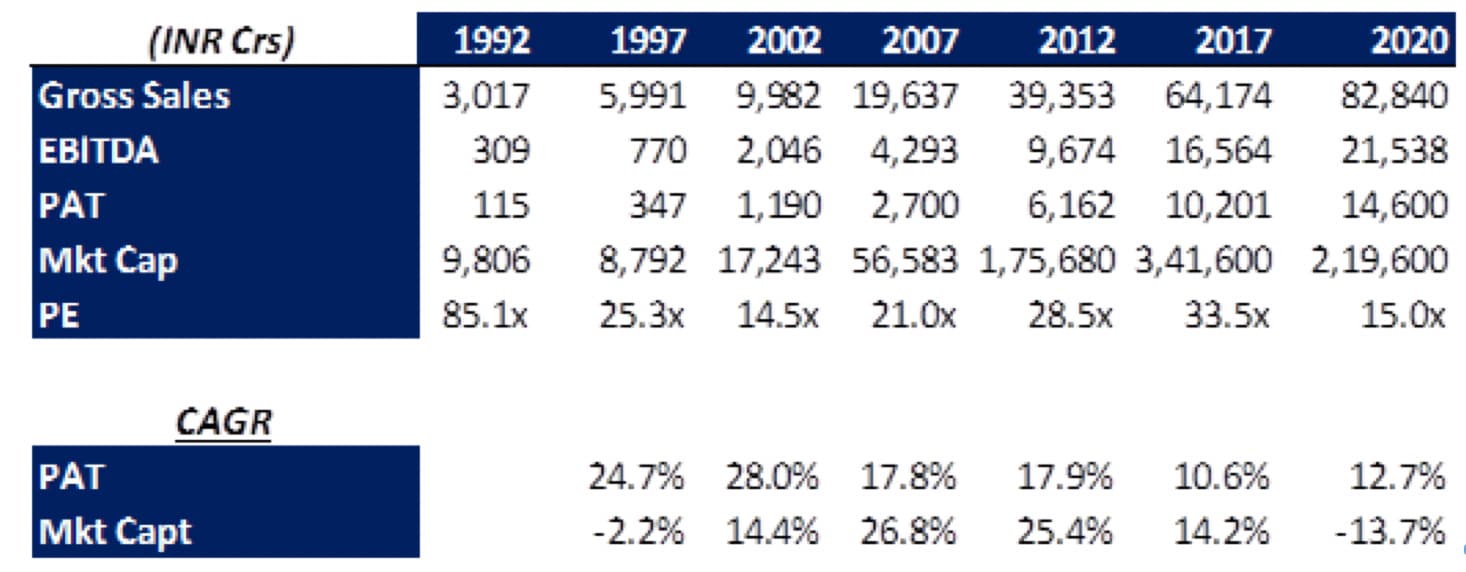

Sharing some past valuations compiled from different sources. Valuations on PE have varied between 12x to 85x (achieved during 1992 bull market). Since 2000, it has been topping out around 35-40x PE. Just for context, current multiples are below median PE of last 15 years.

Disclosure: Invested (position size here, sold shares in last-30 days)