CMP – Rs. 925

Market Cap – Rs. 4808 cr

What does Godfrey Phillips India Limited do?

Godfrey Phillips India Limited (GPIL) is flagship company of Modi Enterprises. The company have two line of businesses. Their main business is Tobacco and the other is Consumer & Retail.

- Tobacco: GPIL manufactures and distributes iconic brand Marlboro in India under a license agreement with Philip Morris USA. They also own and sell their own cigarette brands in India like Four Sqaure, Red & White, Cavanders, Tipper, and North Pole.

- Consumer & Retail: The company sells chewing products pan masala brand like Pan Vilas and Raag. It has 100+ 24Seven convenience stores mainly in Delhi and NCR region. In FY2020, 24x7 stores registered gross sales crossing 400cr mark and its net sales contributing about 13.9% to the total net sales of the company. 24Seven did 42cr of sales in FY2013. Company claims 24Seven to be India’s only organized retail chain in the ‘round-the-clock’ convenience store format. However, this is still not a profitable business.

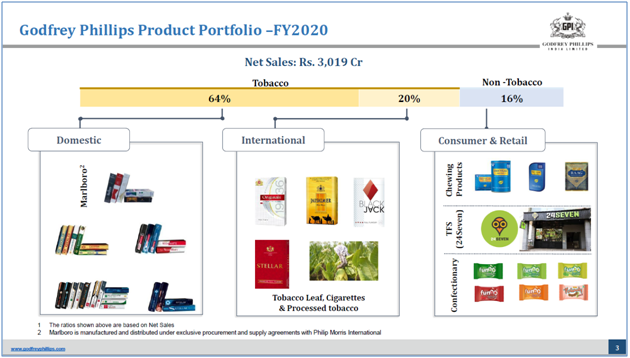

Below is the snapshot from Q4FY20 Company’s earnings presentation which gives breakdown of GPIL’s net sales for FY2020.

For FY20 – EBIT for Tobacco business was 546cr and Retail business was negative 123cr.

Distribution Network: The company has about 800+ distributors, 8+ lac retailers and 6000+ salesmen as part of their network according to their website.

So why does GPIL look interesting?

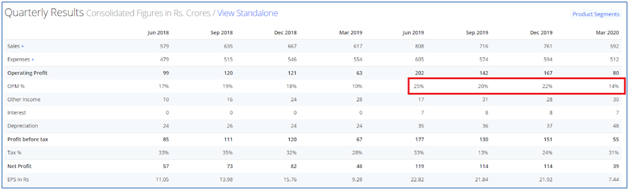

GPIL started reporting big jump in their EBITDA margins starting Q1FY20 as can be seen from below screenshot. EBITDA margins in the range of 20%+ levels were some of the best margins that company reported in last many years.

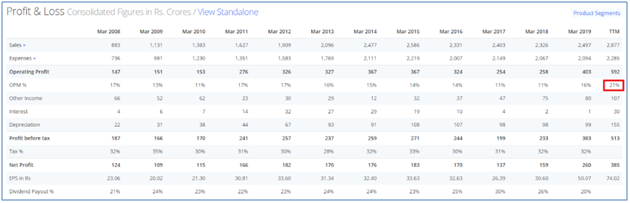

And these quarterly jump in EBITDA margins contributed big jump to annual EBITDA margin for full year FY2020 of 21% which is highest in last 10+ years of company’s history.

So GPIL looks interesting because of impressive increase in EBITDA margins as compared to previous years.

So where did this EBITDA margin expansion come from?

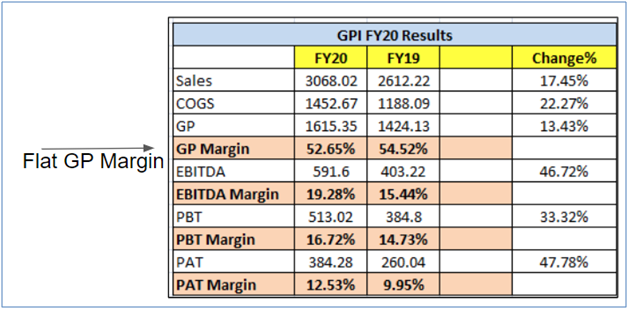

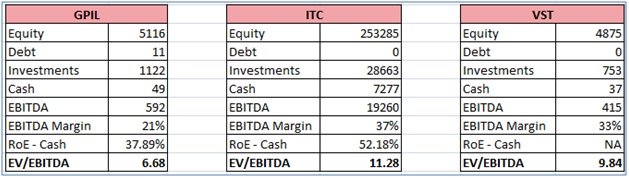

On performing annual results comparison of FY20 and FY19, we get to see that gross margin expansion has not contributed to EBITDA margin expansion. In fact, gross margins declined for the year FY20. So there is good chance that EBITDA margin expansion has happened due to operational efficiencies. The annual report for FY20 is not out yet, so we cannot get detailed breakdown of the operational expenses. But I compared other expenses of GPIL with its peers; ITC and VST Industries for previous years.

Other Expenses Comparison with Peers

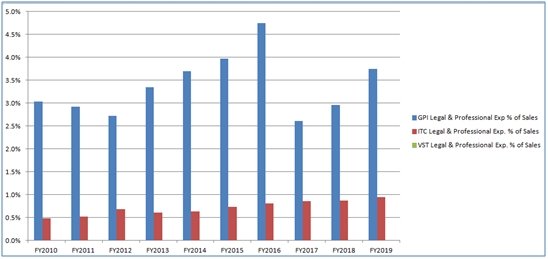

Legal & Professional Expenses:

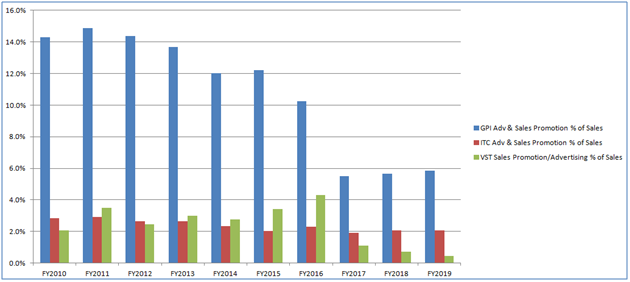

Advertisement & Sales Promotion Expenses:

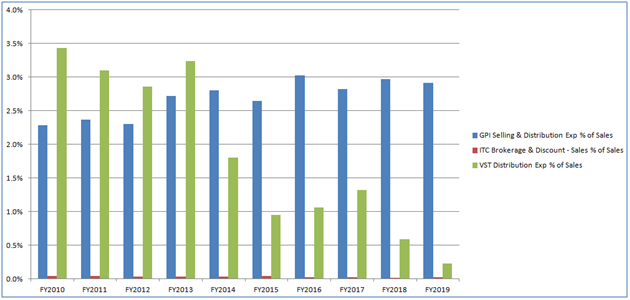

Distribution Expenses:

As can be seen from above charts – GPIL has beaten its peers handsomely by spending way above its peers spending for these line items.

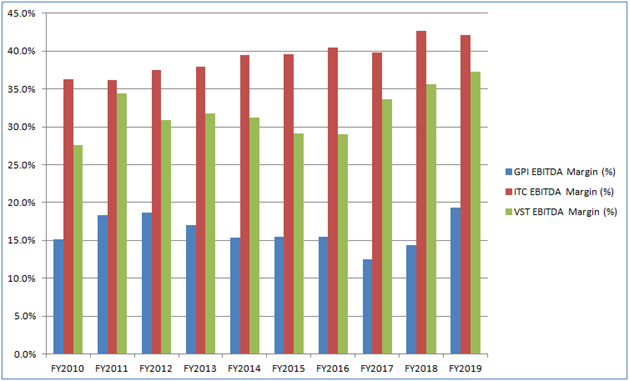

Given their higher than average expenses, GPIL is bound to have lowest EBITDA margins when compared to its peers:

Breakdown of GPIL’s ‘Other Expenses’ line item in its Annual Report for FY2020 should be very interesting and would give us a clue if rationalization of Other Expenses were the main reason for improvement in their EBITDA margins for FY2020.

Future Business Growth Triggers

- Geographical expansion into high potential markets of southern India by developing local sales and distribution infrastructure for cigarette business.

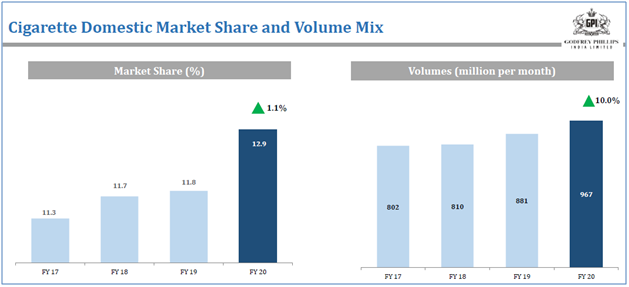

- GPIL’s market share in domestic cigarette jump sharply for FY2020 to 12.9% from 11.8% in FY19. Their cigarette volume also moved up to 987 million per month in FY20 which was 10% growth from the previous FY. This momentum in volume and market share should be closely monitored for its sustenance.

- Possible capitalization on the fast growing retail space through 24Seven

- 24Seven registered a 33.2% growth in FY2020.

Company claims that increase in volume of cigarette sales is mainly driven by new product launches.

Family Feud after passing away of Modi group founder Mr. K.K. Modi.

Late K.K. Modi served as the President and MD of GPIL. He passed away on 2nd November 2019. But a trust deed by KK Modi that he made in 2014 has become the main reason of family dispute between Lalit Modi ( mastermind behind IPL T20 Cricket League), his mother Bina Modi, backed by her two other children, Charu and Samir Modi. The trust deed says that when KK Modi passes away, Bina Modi shall succeed him and within 30 days of her assuming the charge, a meeting of the trustees shall be convened to decide on whether to continue to own and manage all the assets of the trust fund or sell the entire trust fund. If the trustees are unable to take any decision, the entire trust fund including all the family controlled businesses shall be sold.

Family members (trustees) met in Dubai on Nov 30th where Lalit Modi voted to sell all trust assets, but Bina, Charu, and Samir voted to continue to own and manage all the assets of the trust fund.

Lalit contends that after the demise of KK Modi, in view of the lack of unanimity among the trustees regarding the sale of assets, a sale of all assets of the trust has been triggered, and the distribution to beneficiaries has to occur within a year thereof. Other family members state that on true construction of the trust deed, no such sale has been triggered.

In February 2019, Lalit Modi filed for an application for emergency measures before International Chambers of Commerce accusing other family members to not follow the instructions in the trust deed. Other family members have filed a separate plea in Delhi High Court asking for the arbitration to be shifted in India. The Delhi High Court, however, set aside these allegations and ruled that Lalit could go ahead with the arbitration proceedings in Singapore. The arbitrator has set March 7 for physical hearing of Lalit’s application. The order was challenged by the mother and two siblings of Lalit Modi in larger division bench of the High Court which reversed the single judge bench order and stayed the arbitral proceedings at Singapore.

Lalit Modi’s attorney was supposed to present his point of view on 15th July to two judges bench. This is the latest update I have on this family feud matter so far.

So how does this family feud impact investment prospects in GPIL?

In my opinion, this family feud and ongoing legal battle two possible outcomes to it:

-

GPIL is sold off as part of trust asset sale.

-

Family retains control over GPIL and doesn’t sell it.

If GPIL is sold off, then expectation is that a big pocket strategic or financial investor will buyout Modi family’s stake of 47.09% and it will be run professionally with good corporate governance. It has to be seen who the new owner is, but if we go by Warren Buffett’s quote – the lesson is that it is the reputation of the business that remains intact as long as its business economics remains strong. And we know that GPIL is a tremendous cash generating well oiled machine with great business economics. So new ownership under reputed business family name can create pathway for value unlocking of GPIL.

If family retains control over GPIL, then its business as usual. GPIL was always run by professional managers but it was Mr. K.K Modi who was calling the shots. This may continue (by new MD from family) if family retains the business.

Ongoing family feud and how it unfolds is a key item to monitor.

Quick Valuation Comparison

Risks:

- Declining cigarette volume trend in India

- Current EBITDA margins not sustaining and reverses to older/lower levels

- Any sudden increase in taxes on cigarette impacting demand

- Any irrational capital allocation where good money is thrown after bad

- Hostile takeover/sell-off of GPIL due to ongoing family feud which may impact market’s perception of business’ true value.

- Current retail foray continues to burn money at higher rate.

- Any other unknown unknowns.

Disc: Invested and hence biased. In a nutshell this is not a typical buy and hold type of investment for me. There is a catalyst at play here which is change in profitability through margin expansion along with possibly change in management’s stance on value creation for all the shareholders. There has been also decent uptick in volume growth and MS gain in FY2020. I will ride the tide until things keep moving in right direction, but will change my mind if the story turns out to play against the expectations.