Flattish sales from Avanti with revival in margins. Q4FY23 looks ominous, with 25% decline in shrimp seed sales in the first 45 days of the quarter. Concall notes below.

FY23Q3

- Expect CY23 shrimp production at 8.5 lakh MT (vs 9 lakh MT in CY22)

- Present RM price: 110/kg fish meal (export prices are 150/kg causing hike in domestic pries), 57/kg soyabean, 36/kg wheat (expect price softening)

- Annual fishmeal production is 3.75 – 4 lakh MT and Shrimp Feed Industry consumes 3 lakhs MT

- Until mid-February’23, shrimp seed stocking was 5700 Mn vs 7800 Mn Seed during last year

- Lost 50,000 MT of feed sales due to delay in commissioning of new plant

- Feed Capex: Completed expansion of 175’000 MT in December 2022 which will contribute 25% more sales at full utilization

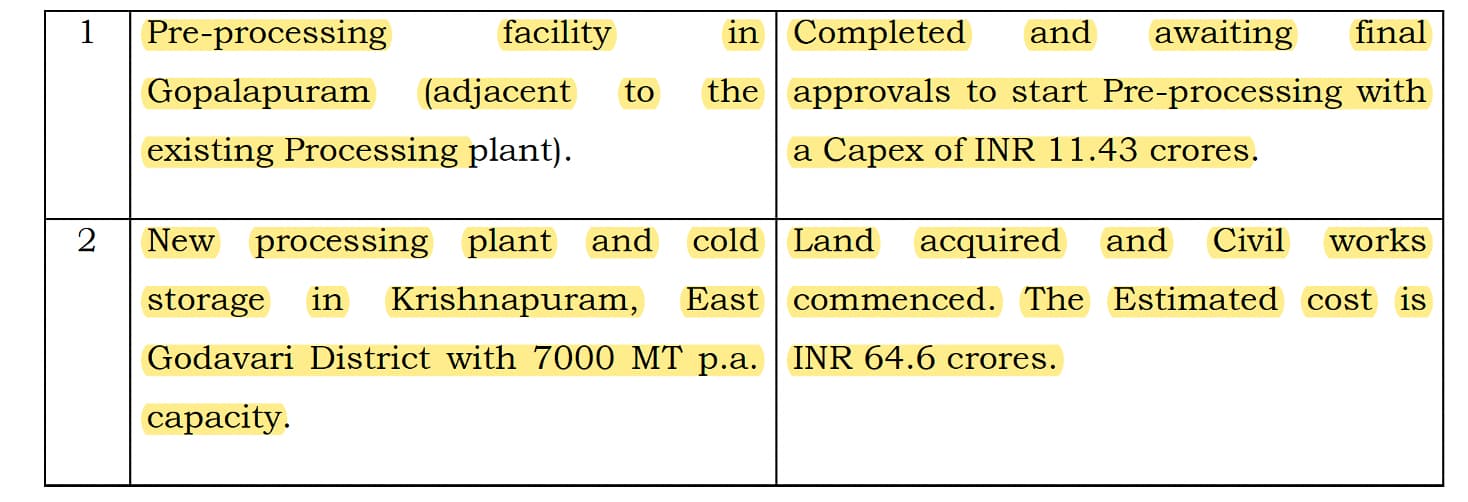

- Shrimp processing capex

- Focusing on value-added products shrimps, where margins are higher. Started 2-3 categories of value-added products (current share of value added products is 25% of sales)

- In value added shrimps, can only operate at 60-65% utilization as it requires more manual work

- Peak season working capital requirement is 800-900 cr. Despite that, they still have 1000 cr.+ cash

Disclosure: Invested (position size here, no transactions in last-30 days)