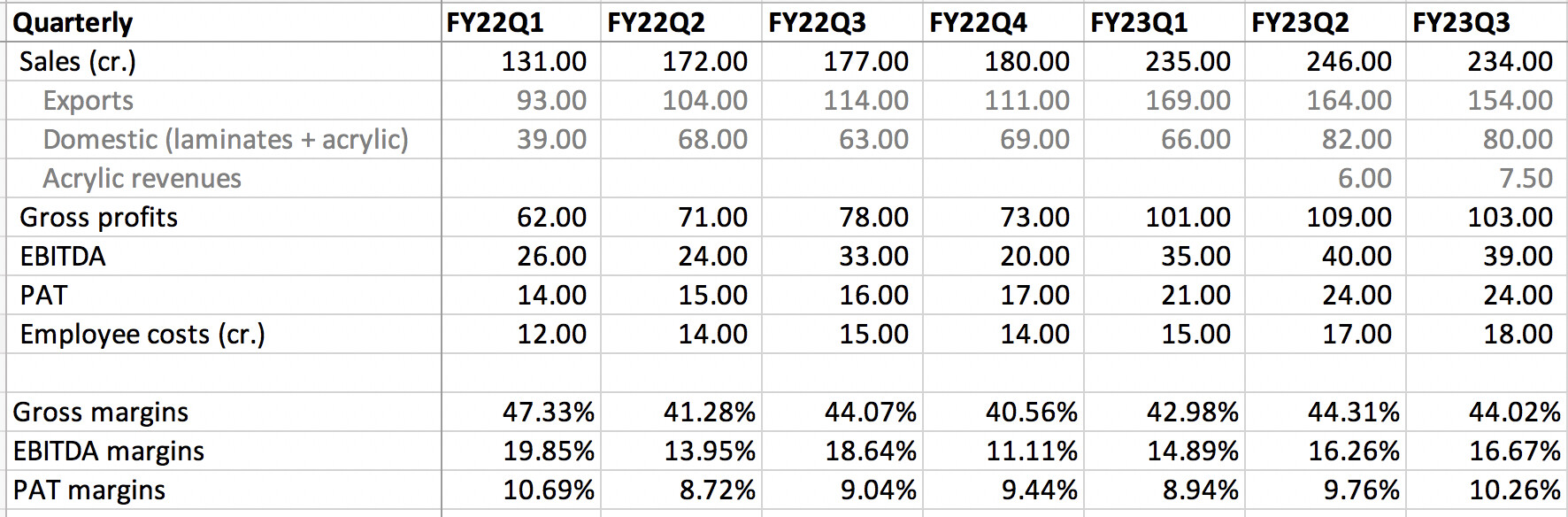

Stylam came out with good Q3 nos, with sales growing by 32% and PAT by 50%. Management has mentioned that with small capacity expansion of 40 cr., they can go upto 2000 cr. in sales. Acrylic revenues have also started ramping up with this quarter sales at 7.5 cr.

FY23Q3 concall

- Exports are growing better than industry due to new customer additions. They are confident growing sales by 15-20% in FY24 over 50% growth in FY23

- Currently operating at 75-80% utilization in laminates division. Even at similar utilization they can make higher revenues by selling more value added products. Currently, 5-10% of sales is coming from value added products

- Gross margins did not show much increase because of higher priced inventory, benefit should start flowing in now

- Higher finance costs were because of Euro debt (and Euro strengthening vs INR)

- Acrylic revenue was 7.5 cr. in Q3FY23. From current capacity, can do peak revenues of 400-500 cr.

- They get advanced payment in domestic acrylic business

- Peers in acrylic: LG, Du pont, Samsung

- Debtor days are high in domestic laminate division, expect reduction in debtor days as brand gets more established

- With a small 40 cr. expansion, their existing capacity can support sales of 2000 cr.

- 60-65% of their products are sold in own brand name, rest are OEM branded

Disclosure: Invested (position size here, bought shares in last-30 days)