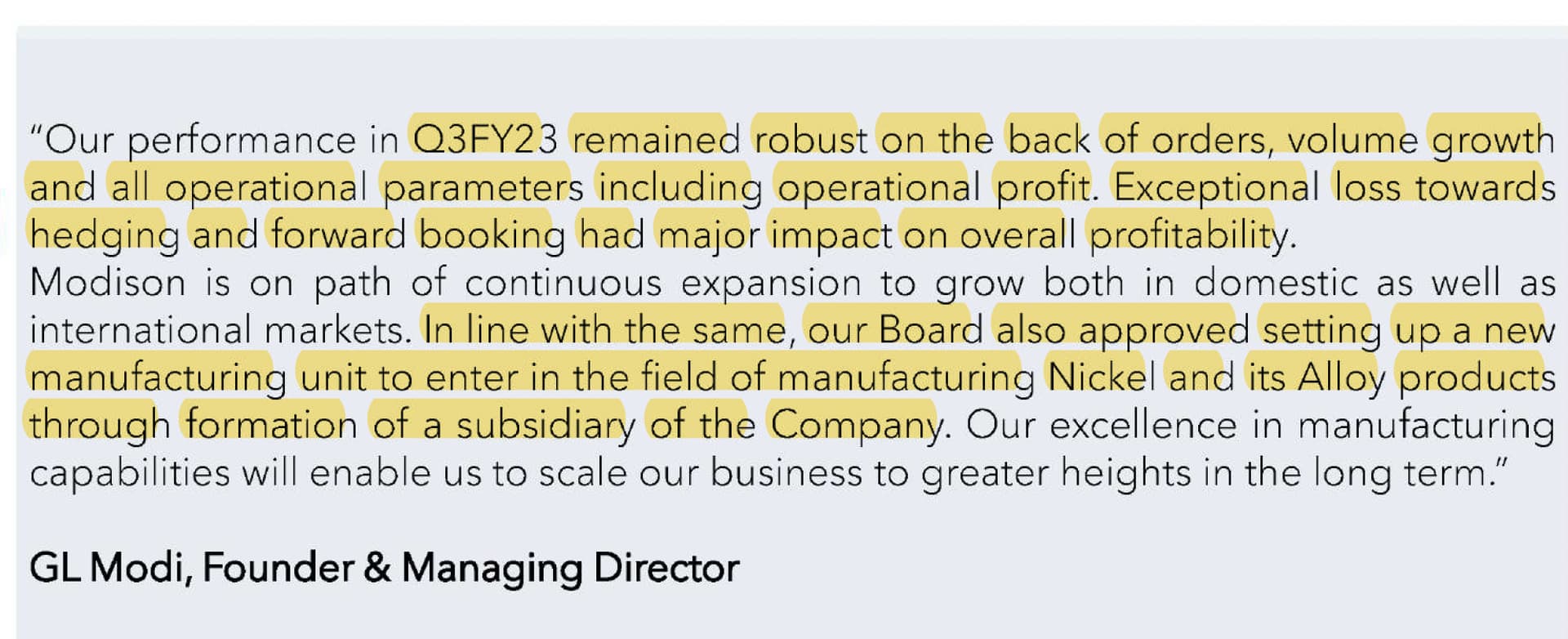

Very interesting announcement from the company, they are setting up a nickel & alloy plant which is a very high margin business.

Disclosure: Invested (position size here, no transactions in last-30 days)

Very interesting announcement from the company, they are setting up a nickel & alloy plant which is a very high margin business.

Disclosure: Invested (position size here, no transactions in last-30 days)