Motivation for writing the thread comes after reading this excellent article https://buggyhuman.substack.com/p/are-you-really-sorted-out where he elaborates the two key criteria - (1) Knowing what works, (2) Knowing what works for me. In India, investors buying cheap companies are looked down upon and growth/“quality” is considered the only ‘true’ investing. This is hogwash. Deep value investing is perennial (praying at the altar of Graham). Whether it works for you or not, is the only question and I want to say that it does work for me. Here’s the proof. (This is not to say that growth/“quality” investing doesn’t work, it sure does, so does momentum, so does technical, but if anyone comes to you and says buying cheap companies doesn’t work, show this thread).

At the portfolio level: CAGR 24%+ over 20+ years. On a portfolio level, it’s a 9x bagger (early investments were very small).

Methodology

Contrarian deep value, crisis situations, special situations (heads I win, tails I don’t lose much).

Largely follow a classic Graham/Walter Schloss approach of buying statistically cheap cos, special situations, turnarounds etc.

Book value and dividend yield remain important metrics apart from EV/EBITDA (you can add ROIC or RoE if you like Greenblatt).

NOT a growth investor, NOT a macro, NOT a technical/momentum investor.

Avoid cos with debt, dislike banks and other leveraged cos.

Book part profit on a 40% gain, let the rest ride forever.

Average down if conviction holds.

Lollapalooza returns - when I buy a cigar butt stock which turns out to be high growth eventually.

Investment horizon - 30 years, oldest holding: ~20 years. (Your investment horizon should be your own goals, there’s no point in assuming a 5 year or 10 year investment horizon if you do not need the money at that time)

With such long timelines, the returns will be VC-like, following Pareto, 20% will deliver all the returns, rest 80% will be dead (4 out of 5 stocks will go down to zero, I’m ok with that).

Some choice examples (hits and misses) from my portfolio. ***I am deliberately avoiding recent buys. This is NOT a full list. (CAGR includes dividends, as calculated by valueresearchonline.com portfolio.) ***

Morepen labs

Detailed note

First bought: Dec 2014

Avg price: 8

Price Sep 2021: 61 (5x+)

CAGR returns: 43% p.a.

Learnings

Bought as a statistically cheap company among the sector, though a leader in certain products (see thread above). Took the risk of promoters not having a great reputation. The co has performed brilliantly over time.

Mastek Ltd

VP thread:

First bought: Sep 2014

Avg price: 99 (est)

Price Sep 2021: 2900 (~30x)

CAGR returns: 65% p.a.

Learnings

Bought as a risk arbitrage play during the Mastek-Majesco demerger and simply held on.

Datamatics Global

VP thread:

First bought: Jan 2015

Avg price: 62 (approx)

Price Sep 2021: 312 (~5x+)

CAGR returns: 32% p.a.

Learnings

Bought because it was a statistically cheap IT services company, part profit booked, then held on

Hinduja Global

VP thread:

First bought: Jan 2015

Avg price: 390 (heavily averaged down later)

Price Sep 2021: 3050 (~8x)

CAGR returns: 36% p.a.

Learnings

Statistically cheap services company, part profit booked, then held on. Promoter finally found some time to focus on it and it has given great returns.

Paushak

VP thread:

First bought: Oct 2014

Avg price: 342

Price Sep 2021: 8500 (~25x)

CAGR returns: 86% p.a.

Learnings

Statistically cheap company, good promoter background, high-risk products manufacturing with oligopolistic characteristics and high barriers to entry. Never in my wildest dreams did I think it would be trading at these valuations ever.

Vardhman Acrylics

VP thread:

First bought: Aug 2015

Avg price: 28

Price Sep 2021: 66 (2x+)

CAGR returns: 27% p.a.

Learnings

Statistically cheap company, good promoter background, part profit booked and held on to the rest.

Tata Steel Long Products (Tata Sponge)

VP thread:

First bought: Sep 2014

Avg price: 460 (massively averaged down)

Price Sep 2021: 890 (2x+)

CAGR returns: 13% p.a.

Learnings

Statistically cheap company, good promoter background, part profit booked and held on to the rest. Bought high and continuously averaged down, reaped the benefits as the commodity cycle turned. Averaged down with high confidence only because of promoter confidence.

Seamec

VP thread:

First bought: Jan 2015

Avg price: 70 (upon averaging down)

Price Sep 2021: 1100 (15x+)

CAGR returns: 54% p.a.

Learnings

Statistically cheap company, questionable promoter background, part profit booked and held on to the rest. Never thought it would give such wonderful returns, thanks to the shipping boom going on now.

Manali Petrochemicals

VP thread:

First bought: Jun 2014

Avg price: 14 (upon averaging down)

Price Sep 2021: 92 (6x+)

CAGR returns: 43% p.a.

Learnings

Statistically cheap company, part profit booked and held on to the rest. Never thought it would give such wonderful returns.

Trigyn Technologies

VP thread:

First bought: Feb 2015

Avg price: 29 (upon averaging down)

Price Sep 2021: 116 (4x)

CAGR returns: 27% p.a.

Learnings

Statistically cheap IT services company, part profit booked and held on to the rest.

HDFC Bank

VP thread:

First bought: 2003

Avg price: 104 (adjusted for splits/bonuses)

Price Sep 2021: 1550 (~15x plus dividends)

CAGR returns: 20% p.a.

Learnings

Bought based on a Wall Street Journal article. Then simply held on. I do not buy banks anymore.

Vinyl Chemicals

VP thread:

First bought: Aug 2014

Avg price: 35

Price Sep 2021: 230 (6.5x+)

CAGR returns: 44% p.a.

Learnings

Statistically cheap company, solid promoter background. I never thought it would give such wonderful returns, still dunno why the market values it so highly, but oh well, no complaints.

Prima Plastics

VP thread:

First bought: Nov 2014

Avg price: 52

Price Sep 2021: 128 (2x+)

CAGR returns: 22% p.a.

Learnings

Statistically cheap company, personally I expected more from this co, still do.

BSE

VP thread:

First bought: Nov 2014

Avg price: 363 (massively averaged down)

Price Sep 2021: 1236 (3x+)

CAGR returns: 15% p.a.

Learnings

Statistically cheap company, exceptionally strong business model, oligopolistic nature. Heavily averaged down on every fall, reaped good returns later as it recovered, booked part profit, holding on to the rest.

Voith Paper

VP thread:

First bought: Nov 2014

Avg price: 581

Price Sep 2021: 1300 (2x+)

CAGR returns: 23% p.a.

Learnings

Statistically cheap company, good promoter background.

PNB Gilts

VP thread:

First bought: Jun 2018

Avg price: 26

Price Sep 2021: 66 (2x+ plus high dividends)

CAGR returns: 31% p.a.

Learnings

Statistically cheap company, good promoter background, pretty much a risk-free trade.

Kirloskar Industries

VP thread:

First bought: Apr 2016

Avg price: 613

Price Sep 2021: 1578 (2x+)

CAGR returns: 28% p.a.

Learnings

Holding co discount, statistically cheap, commodity cycle.

Other multi baggers of note

Ashok alco-chem

2x+

Force Motors (29% p.a. CAGR)

2x+

Tainwala Chemicals (26% p.a. CAGR)

2x+

Ambika Cotton (16% p.a. CAGR)

2x+

Coral Labs

2x+

Other healthy returns so far, but not multi baggers (yet :-))

Buying statistically cheap companies works in Indian markets

There will be gut-wrenching ups-and-downs, stay the course. This is not easy, that’s your edge and that is why others can’t do it

Read a lot, wait for the right time then buy and hold on for a long time. Do not follow the herd, ever (fundamentals of being a contrarian)

By and large the only risks with deep value investing are 1. Promoter risk and 2. Leveraged cos. Avoid (2) like a plague and pray that the promoters do not steal from you.

Thanks for sharing this. Coming from a practitioner, this was quite insightful. Just as an aside, if I discount the crazy bull run of 20/21, then how do the results fare?

For instance for 10 years ending 15 Sep 2020 (i.e ending one year ago, starting on 15 Sep 2010) the CAGR is 13.8%. The last 365 days return is 128%.

This is a feature and not a bug. The portfolio is clearly high-beta and is intentionally so. In order to buy low and sell high, you need volatility. Value stocks need to go crazy down for you to enter and need to go at least moderately up so that you can part-exit. That is why I wrote at the end the following two points:

There will be gut-wrenching ups-and-downs, stay the course. This is not easy, that’s your edge and that is why others can’t do it

Read a lot, wait for the right time then buy and hold on for a long time.

With such high beta stocks held for a long time, you will inevitably be ‘seasonal’, or as Howard Marks says, the pendulum will be swinging to extremes. There’s going to be cyclicality, there’s a season to buy and there’s a season to sell. If it gets very hard to find statistically cheap companies then instead of looking harder, it is better to start booking profits and wait for the right moment.

I personally experienced the above in the Covid crash in 2 stocks Shaily Engg. and Intellect Design.

Have these stocks from 2015 till March 2020, instead of buying more in the Crash I exited exactly at the wrong time-only to see and miss a 10+ bagger in both stocks.

Lesson learned: Capacity to Suffer.

so how long u hold or have capacity to hold because in small caps the returns are highly non-linear, u can see how a 18 month period holding/exit have exponential returns and Hugh swing in CAGR returns.

**Thats not too bad return but exceptionally outstanding on account of individual stocks as you had highlighted the investment which works for you i would like to here other part of the story the investment which doesn’t worked for you and how you deals that in your temperament . Secondly could you share how you allocate a part of total portfolio to individual stock or what is your allocation strategy ?

This is my perception i may be wrong but no body know before hand how your investment will roll out in future your rightly pointed out it can even wipe out your capital permanently , what are the key common points of your all multiX return stocks … You had narrate what HAPPEN to your stocks but HOW you control your temperament to NOT to sell the investment you made and How much is a single investment is part of total portfolio weight Thanks again for sharing your experience and wisdom .

regards

There are two parts to this answer. Part 1 is to ensure your capital allocation on a networth level is correct. I have 55-65% of my entire networth invested in equities. I make it go down to 55% in times like these when markets are at a high and I’m a seller in a rising market and I take it up to 65% or so when there’s a crisis. (Remember the basics: buy low, sell high).

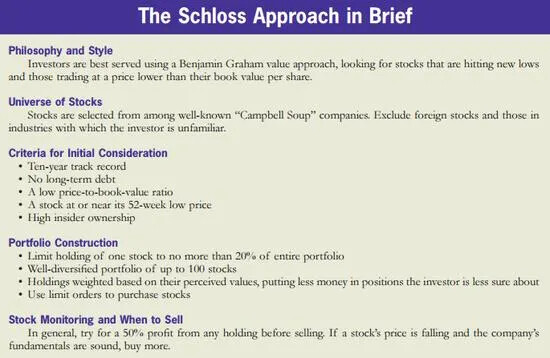

Having decided this part, then part 2 of the answer is to simply follow some time-tested rules. I broadly follow Walter Schloss method with only a few modifications. It’s neatly summed up by some blogger in the graphic below (I have posted this earlier in other threads also).

I look for P/BV but also for Dividend Yield and EV/EBITDA when screening for cheap companies - these are all standard valuation metrics.

At 40-50% rise in stock price, I part-exit (not fully), and hold on the rest with an expected time frame of multiple decades, however, on an ongoing basis I always read the annual report and scan primarily for the two things I mentioned previously: a. Debt (“No company went bankrupt without taking debt”) and cash flows and b. Promoter issues (mostly audit observations, contingent liabilities).

When I average down, I stop buying when the single stock position becomes about 5% of my portfolio (or correspondingly: 3% of my networth). My loss in LEEL was 5% of my portfolio, the biggest sting.

Although the method recommends not having a single stock go above 20%, I am comfortable with higher allocations as the price rises. This is necessary as my holding period is measured in decades. As Nassim Taleb describes in the Black Swan, 80/20 rule and 50/1 rule are the same. 80% x 80% x 80% of the returns will come from 20% x 20% x 20% of the investments. It also means that 4 out of 5 of my stocks go to zero over long term, and I’m comfortable with that.

If i am not mistaken though,Schloss 's returns were about 15 percent annually for 40 year time frame.

Is it really a good strategy vis a vis Graham’s net net strategy.What have your returns been like?

A very good writeup. I started out my investment journey investing in statistically cheap, decent quality companies the results were mixed bag. I gradually moved towards quality business with stable but a lower return.

One of the biggest challenge I faced was guaging the promoter quality. My failures were due to promoter frauds. How do you address this problem?

I could make out - operational issues , setback in product, slowdown in end consumer industry , rising .RM prices etc. Promoter integrity issues led to the losses. How do you mitigate those

@theashworld Just gone through your post & find out all winners & links of VP threads along with your purchase details. But it’s my query you had join the VP forum on last July20 & all of your shared details are pretty old then what is the value of sharing your holding details. Apart from that, I beg to differ that all the cheap companies turned out from ashes which I’m missing in your post.

Admin can delete my post if it’s not aligned with the guidelines of VP forum…

Fully agree with your question? As usual there can be a survivor bias. Not all cheap stocks are Pheonixes and most do bite the dust. We all try to sell the stories of success.

Cash flow as a proportion of PBT (over multiple years)

Taxes paid as a proportion of profits (“Nobody pays real taxes on fake profits”).

In general, I can also argue the other way though - at what point and on what basis can you say that a particular promoter is not fraud? Remember, the fraud ones are masters of delusion, it’s non-trivial to see through it. I am happy to receive suggestions in this regard and improve my learnings further.

Cheap does not always mean undervalued. My aim is to find undervalued companies which can give the earnings to use in one way or the other. But if you have more ideas do share I would love to look into it.

Could you please elaborate more on this? I am curious to understand why it trades at such seemingly cheap valuations. Going by the data on screener its OPM has stayed above 30%, its book value is 182 yet it trades at less than half of this, ROCE is pretty low however. I do not know much about the company so if you could kindly briefly explain about it and why it trades at such seemingly cheap valuations it would be really helpful