Morepen labs was a sensation in the 90s with ambitious growth plans. However the company suffered badly and filed for bankruptcy. (I’m not certain if the bad performance was because of the passing away of the founder, but the timelines do coincide) From a high of about 520 in March 2000 the stock price fell all the way down to 2 in Sep 2013.

Subsequently, the founder’s brother took over, they did corporate debt restructuring and gradually things started to improve.

Today, it’s a global leader in Loratadine API and intermediaries, and claims to have about 80-90% of Loratadine generics market in the US (total $2B market). That sounds right considering their revenues from Loratadine. However, the Loratadine revenues have stablized, so expecting further growth might not be wise. Last couple of years the revenues have been around 108Cr. (As an aside, here’s an interesting article about loratadine -http://www.nytimes.com/2001/03/11/magazine/the-claritin-effect-prescription-for-profit.html )

The company has however managed to introduce new API intermediaries like desloratadine, Montelukast, Atorvastin, Fexofenadine over the last few years and they’ve done exceedingly well.

Atorvastin revenues 620L in 2010-11, 2350L today.

Montelukast 2250 to 5000L (However, note that this is far short of management projections, so I’d beware of wild projections by the management)

Fexofenadine 372 to 1300L.

The home health business is growing steadily from 31Cr to ~45Cr in revenues in the same time period as above. On top of this, it has strong brands in the local market. Dr Morepen (which is a subsidiary company) is doing exceedingly well, revenue growth from 15Cr to 38Cr in the same time period as above.

Stock price? From a high of 17.05 on 23 Sep it’s now down to 8.8 or so. Reason? A ‘stable’ quarter showing no growth. Note that Morepen does not report consolidated quarters so we are not sure how Dr Morepen has performed over the last 6 months. Also, one of their major PE investors has cashed out leading to a dramatic drop in share price.

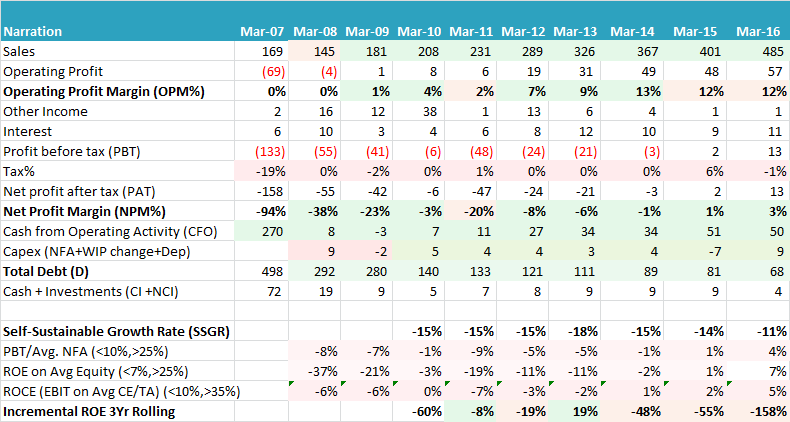

At about 400Cr Mcap and stable but growing diversified revenues of 366Cr, this sounds like a good price compared to other pharma/FMCG plays.While operating cash flows have always been positive, net cash flow too have been positive for the last 4 years.The company is expected to post a net profit for the first time after many many years (at least 8 years).

Gotchas:Contingent liabilities are also a big question mark at this point. Also"Turnarounds seldom turn" - Buffett. The company is not covered widely in the financial media. I could find only one interview by the CEO where he also discusses why the stock is a good investment (WTF?) Also there is no date on the interview and the CEO speaks of EPS around 50 so I’m not sure when this was published -http://www.indiainfoline.com/article/research-leader-speak/mr.-sushil-suri-cmd-morepen-laboratories-ltd-11743270_1.html

However, given the pros and cons and considering a relatively stable business like pharma and also subsidiary strong FMCG/devices business with strong brands, I’m positive on this stock at CMP of about 8.8

Would love to hear people’s thoughts, and also importantly, if someone can scuttlebutt that would be highly appreciated.

Disc: I’m long.