Ashok Alco-chem is a microcap company listed on BSE is . It is having a market cap of 77cr. (@cmp of 169).

Apart from the manufacture of Chemicals, the Company also commenced trading in some mineral products (Bauxite, Bentonite, Kaolin, Bleaching Earth, Iron ore, Gypsum) mainly for exports from the year 2009 which has given a substantial boost to the top line figures and a ramp-up in revenues as well as profitability.

As per the AR company is focusing on improving margins rather than increasing sales by compromising on margins.

Company has an ROCE of 29.54% and 3yrs ROCE of 32%. Debtor days has been mostly stable at 2 months.

Promoter holding as increased to 54% from 49% through conversion of warrants (@rs 30).

Debt to equity is 0.09 and ROE is 32.05%

Company has been posting good results since last three quarters. Has declared dividend of Rs 1 this quarter. The manufacturing unit posted profit this quarter.

Risk: currency fluctuations

Views invited.

You seem to be a new member and may not have known certain rules of the forum for starting the new thread. So request you to go through the forum guidelines for starting the new thread at the below link and follow the same while starting the new thread.

I have also been tracking Ashok Alco Chem for last 2-3 quarters and have been invested for sometime. I was intrigued by the great set of results the company had been declaring. I tried finding more about the company but very limited information is available. Following are some of my observations:

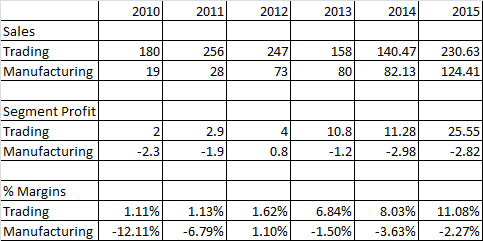

The co was historically into manufacturing of Chemicals (Ethyl Acetate) but the margins were wafer thin and usually they were into losses. They started a trading segment in 2010 which increased the turnover from about 10 Cr to 200 Cr. In the initial 2-3 years trading segment had very low margins but since 2010 the margins started getting better though the turnover fell perhaps due to closure of mines etc in India. Interestingly since last 1 year the trading division is again doing phenomenally well. They are trading mineral like - Bauxite and Betonite. Here is a snapshot of the two segments:

What I also found interesting in the last few annual reports is that the company mentions about the focus on the trading segment and efforts to get better margins, customers rather than just turnover. And as per the numbers the same seems to be playing out.

Its also interesting to see that despite being just a trading company - the co is having negative working capital:

So though the above are the positives based on the numbers but we need to work on the company and understand the business model and how sustainable it is. Following are the negatives and concerns:

Trading business can be very volatile, risky and hence the above nos may be temporary

It may also be the nos are good due to currency gains.

Promoters had done a preferential allotment of warrants at very low price.

Dear Sir, I am new to this site and also a novice investor. Please help me understand how the trading activity can have better margins than a manufacturing activity? Although the numbers speak for themselves, but are there any ways in which any company which is , say just trading, improve upon its margins by almost 1000bp in few yrs…! And please also tell, as to the user industries of these chemicals…!

Ashok Alco Chem is a totally new company with very limited information out there. It caught our attention due to consistently good nos and sheer undervaluation. As the business model seems to be trading, its obvious that there can be wild swings in the earnings and the current earning may or may be sustainable. At the same time there may be a good reason for the good nos and the company might be having some edge. So we are just trying to keep our eyes and ears open and trying to find our more

Thank You Sir. I notice something very peculiar in these chemical companies…they seem to have very high or very low profits…i mean in terms of consistency of eps…wonder y so much variation…?

Eps grows from 6.3 to 6.8 because of higher ewuity base after the promoters converted warrants last quarter.

The manufacturing division for the second consecutive quarter has posted positive net profit from 0.69 cr to 0.72 cr (qoq) .

Eps overall qoq declined due to higher tax out go.

PBT increased from 4.36cr to 4.74 cr (qoq)

PBT increased from 3.87 cr to 4.74 cr (yoy)

Overall things are looking good. The commodity slow down hasn’t affected their trading sales or profits. They are really doing something special in mineral trading division. Waiting for the AR to come out.

Inputs are welcome.

There is a huge demand for minerals such as bauxite and bentonite for export from India.

Depending on the material (eg. calcined bauxite / specially processed bentonite) - It is not unusual for a resourceful trading house - who deals in specialised fractions, ensures quality and exports to medium scale or smaller end users directly - to make upwards of 15 percent or even more.

What is required is direct relationships with the manufacturer and end user.

The results have been decent. Though zero growth Y-o-Y but impressive Q-o-Q.

High ROCE business but markets seems to ignore it as the company is into commodity chemical trading.

I quote from AR page 8 - Results of operations and the state of company affairs

The rise in the profits is due to huge demand for bauxite in the overseas market for the trading division and improved efficiency of the manufacturing vertical. Moreover in addition the chemical division also performed substantially better vis-à-vis compared to previous year 2013-14. The fall in the crude prices didn’t deter the profitability of your Company.

On page 11 - Outlook AR mentions

The global metal industry, to which your Company’s Trading Division caters to, has been experiencing a reasonable growth rates over the last few quarters in terms of capacity addition wherein the existing demand there from is expected to be fairly resilient.

I have not dug deeper but this looks counter intuitive on the face of it. Global metal industry in not at all in good shape. Look at the stock prices of some of the biggest Aluminum producers in the world

Dear friends ! a little information from my side also. Financial parameters are impressive but business outlook may not be so good for comming few quarters. Reason is that some of the products from this company might be in recession. As some chemicals like Bentonite is mainly used in drilling of Oil wells.

Drilling industry prospects look grim so this may dent the profits of this company also. So please do your homework throughly.

How does Ashok Alco even get the Bauxite to export it?

I do not see any mention of mines in the annual reports. Does it own any mines ?

Also the share of export is much greater than the share of selling to domestic consumers. I guess China is the major buyer of Bauxite. Will the change in export duty from 20 to 15% improve margins at least a little bit?

Also since major Bauxite exporters like Australia, Malaysia joining the party and Indian Aluminium producers putting pressure on the government to increase export duty on Bauxite is Ashok Alco - Chem in for a major trouble.