Manali Petrochemical Ltd (BSE Code: 500268) (CMP: Rs.18.7)

MPL is a leading producer of propylene oxide (PO), propylene Glycols (PG), and polypols in India. These products find application in various industries and are used in products such as pharmaceuticals formulations, food flavors, fragrances, detergents, perfumes, toilet soap, automobile seats, garments, furniture, mattresses, adhesives, refrigeration, coatings,resins, etc.

Anti Dumping duty is planned by India Government against China & Taiwan will be levied so as to support MAKE IN INDIA program.

MPL has completed expansion at ennore port for raw material storage by 3 times.

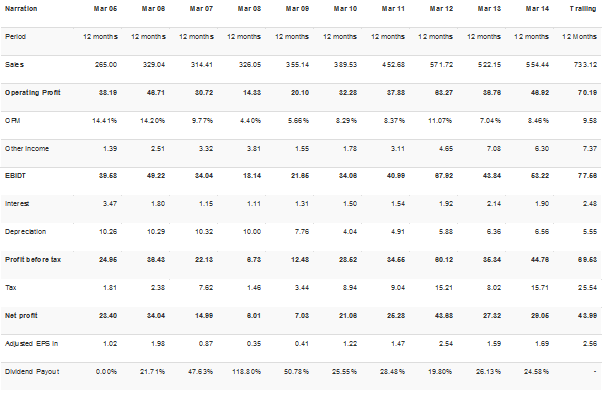

MPL is likely to post NP of Rs.76 cr for FY 16 with EPS of Rs.4.5(fy16). at consistent dividend payout of of 17.5% div yield will be close to 5%.

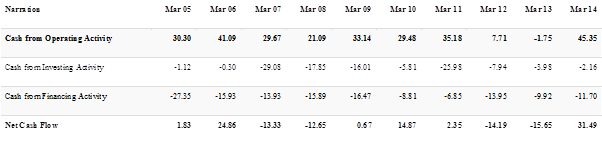

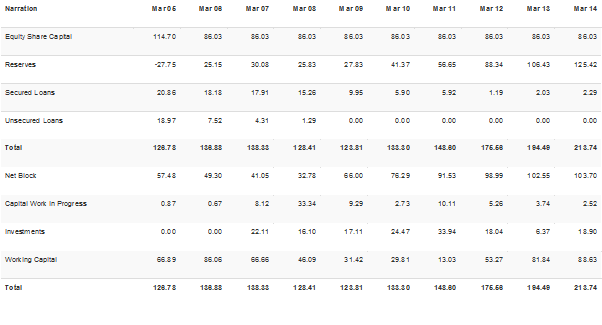

Company has Zeo Debt. AT THE CMP OF Rs.18.75 MPL has mkt cap of just Rs.322.5 cr. With the fall in crude price, margins are likely to improve.

Some links

while the above news was denied, i think that Manali does have strong capability.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=f7492d17-3438-4281-9d10-5ead4f8f5002

Issues

Company is part of SPIC group and they have had entities which went through CDR

in the Q4 Results the company paid 17 crs rent which they clarified as arrears -waiting for annual report to get more clarity.

Price volatility - if anyone hasa clue about specific commodity cycle here … appreciate your views

Great. Please avoid generic optimism/pesimissm…

Great. Please avoid generic optimism/pesimissm…