Hinduja Global Solutions is a global business process management company. The company has a consolidated topline of 2800 crores with a PAT of around 165 crore. The stock has a EPS of around 80 for FY15 and is currently trading at 6x. I can see a lot of consolidation happening 500 levels in this stock and this looks like a strong buy opportunity at the current levels.

They have acquired 2 business in the past quarter.

Hinduja Global Solutions acquired 89.9% stake in US based health insurance focused cloud tech company Colibrium for an undisclosed amount. Colibrium reported revenues of $12.6 Mn(70-75crores) in the last calendar year.

Mphasis sold a significant portion of its domestic business to Hinduja Global Solutions. All 7,000 Mphasis’ employees will be transferred to HGS. The deal value was Rs 17 crore but HGS is getting Rs 140-160 crore in revenue along with new clients and new processes that they could look to leverage for the international market.

Considering these 2 acquisitions and modest growth of 5% in the existing business it should post a topline of 3100 crores (2800*1.05+75+140) for FY16 with PAT of around 180 crores (margins remain stable).

The stock looks dirt cheap at this price. Would like to hear thoughts from fellow members on this.

You have not disclosed your holding in the stock. Please be informed that the disclosures of holdings is a must for starting a new thread on a company. It is very irritating to mention this everytime. Everyone is requested to follow these guidelines strictly or we may be compelled to put further restrictions.

Two red flags are: high debt and some stupid reason by the management for lower profits last Q (bad weather - really? You’re a frigging call center business!)

However, it’s pretty cheap and it seems that there’s enough margin of safety there. The acquisition of mastek’s biz should be a plus.

Return ratios are poor. If we look at similar sized IT companies which have return ratios north of 25% and trade at PE of 10-12, it does not look cheap. Div yield is also only slightly better than Infy. Unless there are triggers in terms of growth or moving up value chain this may remain cheap. Integrated IT-BPO companies are growing their BPO biz at faster rate due to end-to-end services they can provide compared to pure play BPO units.

The Roe was 13% for fy15, which I believe is decent.

The stock has book value of 780. So, its trading far below its book value.

Debt to equity is .4x not very high. Easily this could turn into a net cash business in 2 years time.

Net Debt/Ebita stands at 0.7x.

Acquisition of cloud player suggests management is focusing on the right things for the future growth.

Overall there seems limited downside from current levels.

Crisil published a buy rating on the stock in Feb 15 with TP 720 and expects the margin to improve going forward.

The delivery % along with volumes have increased in this week which suggests investors are accumulating the stock at current levels.

The stocks is cheap. Seems to be trading ex growth. Why is it cheap?

BPO business is a cash flow gen machine. Surprising to see the weak fcf and debt on books. I understand they have some cash which is kept abroad. Promoter reputation with these red flags are the only reason I could think of why the stock is cheap. At some point if and when Mr market will look beyond this there could be upside but hard to see this as a multi bagger.

Why is it so cheap - I do not understand either. (This is the only stock where I am in loss in my investing career aside from south Indian bank where I booked out suffering only a marginal loss)

Disc: invested at ~600/- (after adjusting for the dividend received)

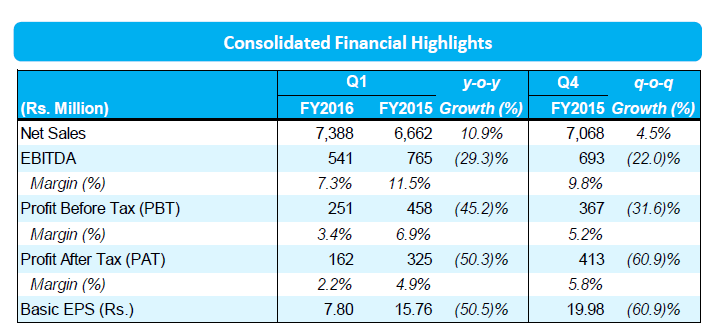

Last quarter they had guided that Q1 bottomline because of canada operations will struggle as has been the case, and after which it would improve.

Today’s comments -

Commenting on the results, Mr. Partha DeSarkar, Chief Executive Officer said:

“Revenues for the first quarter of FY2016 grew by almost 11%. Our profitability has been

below expectations due to lower than anticipated volumes in some geographies and increased

cost of operation.

We believe these volume fluctuations are short-term and expect volumes to improve over the

rest of the year along with increase in profitability. We have introduced cost containment

measures to further strengthen our profitability.”

Margin of single digit is less than some of the manufacturing company also. What these people are doing in IT business to report such a less margin may be a question to ponder over.

Agree. I don’t know why the management is struggling so much. BPM is not a hard business to run. I’m fearing my value buy is turning out to be a value trap, though I’ll probably hold for a year or two until the market in general recovers (hope hope hope

The crux of the reason why the stock has fallen from it’s highs is the issue in Canada.

The results of this quarter makes it appear that Canada operation has been turned around.

Fingers crossed now…let’s see If management can indeed improve profitability as has been the claim over the last 3 months.