Date: 16-May-2015 CMP: Rs 410 Mcap: Rs 925 Cr

Some targets

Capital Market:

Mastek’s US-based subsidiary Majesco received the clearance from the NYSE Listing Committee for listing of Majesco shares. This is a major milestone. Majesco will go for listing of its shares on the NYSE on successful completion of the shareholders’ vote approving Cover-All’s Technologies merger with itself. The merger is expected to be completed by June 2015. Majesco acquired Cover-All’s Technologies in December 2014 in an all-share deal. Majesco issued 16.5% of its shares. Majesco offers core insurance technology software and information technology services to around 100 insurance carries that are into property and casualty, life and annuity.

The software solutions and services include policy administration, billing, claims and distribution. The combined entity, Majesco and Cover-All’s Technologies, will have over US$100 million in estimated annual revenue and around 150 insurance customers. Tracking developments at Majesco, software provider Mastek had a decent run-up on the trading floor. The stock reported a five-year high of Rs 513.5 in March 2015. From a 52-week low of Rs 160.2 in May 2014, it has jumped 2.7 times to the present level of Rs 435.6. The stock is likely to remain in the limelight till the listing of Majesco. Interestingly, based on the Majesco and Cover-All’s Technologies deal, Majesco will be worth around Rs 1100 crore. Small-cap Mastek was valued at Rs 873 crore on 30 April 2015.

ICICIDirect:

By end of 2015 : Target of Rs 600 (base case) and Rs 890 (best case)

Anand Rathi:

Target of Rs 620

India Nivesh: (Thanks to Advait Pande. I had seen the old report only which had target of Rs 554)

Target of Rs 724

I frankly do not have a target. At the sametime I do have a very very rough guestimate.

Mastek (Solutions)

FY 2014-15

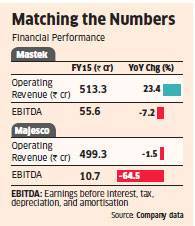

Revenue:Rs 513.3 Cr EBITDA:Rs 55.6 Cr (before exceptional items) [Company provided]

NP: Rs 20-30 Cr [My guess]

Mcap : Rs 300 Cr [Again my guesstimate]

Majesco India (Holding company of Majesco US)

Since Majesco India and Majesco US are product based companies , will use Sales / Mcap

Cover-all Revenue (2014): $20.5 million . Mcap : $28 million

Majesco US Revenue after merger : $106 million. Mcap: $ 212 million (My guesstimate)

Post-merger of the Cover-All entity with Majesco, the Majesco India Limited will hold 69.7% of the Majesco US arm, and Mastek UK Limited will have 13.8% shareholding in Majesco.Remaining 16.5% will be with Cover-All shareholders.The stake which belongs to Majesco India translates to $ 148 million

Since Majesco India will be holding company, we need to discount the above by some %. I will use 40%. Thus Majesco India will have a value of $88 million. This translates into approx Rs 554 Cr.

The above is a worst case scenario and is also just to illustrate the the thought process. Though the current mcap is Rs 925 , my calculations show a combined market cap of Rs 854 Cr. I have not included the 13.8% stake of Majesco US held by Mastek UK in the valuation. Mastek UK is 100% subsidairy of the Mastek solutions division. The management has already said they may monetize this stake in future for the benefit of Mastek (demerged) Services division. The value of the 13.8% amounts to Rs 184 crore (assuming mcap of Majesco US as $ 212 million and no holding discount).

Before we form a opinion please play around with a couple of numbers.

(1). The Mcap/Sales ratio I have used for the above calculation is 2 whereas the No 1 company in the Insurance products is Guidewire has MCap/Sales ratio of 9.36. Guidewire Mcap : $3.46 billion. Sales (ttm) : $ 369.42 million Net Income (ttm) $18.82 million.

Thus the scope for playing with the Mcap/Sales ratio is huge and I think I have taken a very conservative figure by using 2 instead of using 1.35 which is got by extra polating Cover-All current Mcap/sales. (Cover- All current revenues are $20.5 million and the pro forma merged revenue of Majesco US will be $ 106 million)

(2). The holding company discount again is debatable. Anand Rathi is using 35% discount whereas ICICIDirect is using 25%. India Nivesh - 30%. I have used 40%.

Playing with the above 2 points, will vary the vaulations hugely. My valuation excercise was not to discover the target, rather it was to find the downside. IMHO, the stock does not have much downside after the demerger. If you can hold the shares for more than 1 year , the downsides are even more reduced.

Top notch senior mgmt additions (non desis too) in Majesco US and recent insider buying has also strengthened my conviction.

My strategy as of now (it is very fluid now and may/may not change) is to sell the Mastek India shares some time after the demerger, to retrieve some/most of my investments and hold Majesco India shares for a longer time frame

)

)

. However, it is entering into fairly valued territory, as this news is positive for (newly formed and to be listed) Majesco and will not have any significant impact on Mastek IMHO.

. However, it is entering into fairly valued territory, as this news is positive for (newly formed and to be listed) Majesco and will not have any significant impact on Mastek IMHO.