Force Motors is a fully, vertically integrated automobile company, with expertise in design, development and manufacture of the full spectrum of automotive components, aggregates and vehicles.

Its range includes:

Multi Utility Vehicles - Force Trax

Light Commercial Vehicles - Force Traveller

Small Commercial Vehicles - Force Trump

Agricultural Tractors - Balwan & Orchard

Personal Vehicles - Force Gurkha and Force One

Apart from these vehicles, FML produces and assembles engines for Mercedes and BMW in India.

The company has manufacturing facilities at Akurdi (Maharashtra), Pithampur (Madhya Pradesh), Urse (Maharashtra), Chengalpattu (Tamil Nadu) and would be inaugurating their fifth plant soon at Chakan (Maharashtra)

Investment Theme:

The only company in the world to produce and assemble engines for both Mercedes and BMW

Market leader in Vans segment in India (~60% of the van sales in India are through Force Traveller according to Mr. Prasun Firodia, Managing Director - FML)

P/E ratio of 21.67 as against industry P/E of 39

Almost debt free company

The sales and net profit have been increasing at higher double digits rate in the past few quarters

Key risks:

New registration of diesel cars above 2000 cc have been banned in Delhi and NGT plans to ban them in another 14 major cities too

Return on equity is a low 7.9% but has been increasing over the quarters

Force One has not received a good response during its 5 year presence and the company plans to exit this segment. This gives an indication that the company would focus on their forte, commercial vehicles rather than spending energy in passenger vehicle segment.

@ Admin: This is my first post at ValuePickr forum, so kindly request you to correct me incase I violate any rules of the forum.

The reason I am bullish on automobile sector is because India has a big catch up to play in automobile.

Vehicles per capita(ie per 1000 inhabitants):

USA = 809

Brazil = 249

China = 128

Indonesia = 69

India = 18

And Force Motors has presence in both commercial and passenger vehicle.

Force Motors has presence in the commercial passenger vehicle and not personal passenger vehicle. It exited the personal passenger vehicle this year (the Force One SUV).

ROE has improved significantly for FY16 (12.1%) compared to 7.8% in FY15, its more than 50% jump. In general ROE appears poor due to huge jump in reserves due to an exceptional item. I feel the company should have distributed some amount as dividend, that would have improved their ROE. Anyways if company continues performing ROE will improved, it has reached double digits in FY16.

for march 2016 EPS stands at 135 , 50% above the EPS of 2015. The current PE stands at 23. Just want to know why the market is assigning so less PE compared to growth .will this gap converge ? ROE of around 12 is less ,is that the reason , seniors please enlighten

Discl: Invested from lower levels

I believe the low valuation of Force Motors wrt to its peers is because of the following reasons:

Low operating profit margin (in the range of 10%)

Low RoE (because of the huge reserves and surplus in FML’s books)

Unresponsive nature of the company to investor and customer queries (I have mailed them a couple of times regarding a query but there was no response. Also I have read reviews about Force Gurkha at TeamBHP, where they have highlighted the lack of response from management regarding service and product delivery)

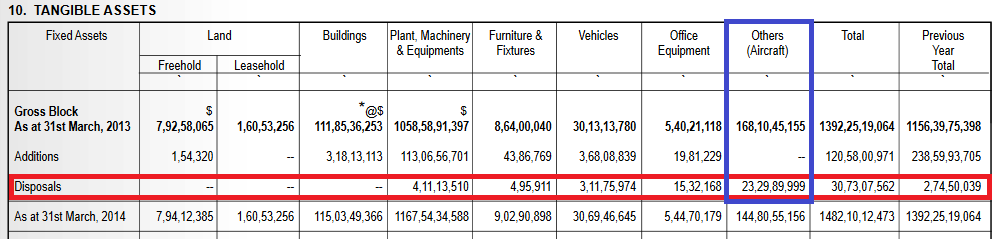

Perusing the latest Annual Report, I see that the management seems to have purchased another aircraft in addition to its existing one. See screenshot below:

Three years ago, the company had purchased another aircraft for approximately 144 crore, which also caused a lot of investor heartburn. Wonder what necessitates the management to purchase a second aircraft? What urgent travel requirements do they have that is not satisfied by having one existing personal aircraft at their beck and call. These are the kind of reasons why Force Motors doesn’t see much interest from institutions and the larger public. I am invested though, so relevant disclosure there.

This is a red flag. Investing in white elephants (expensive to maintain and depreciating assets with no value add) does not reflect well on MQ. I guess some backdoor financial transactions here for purposes other than increasing shareholder value. Better players in the market…

There may not be backdoor financial transactions, I think the management just likes the good life.

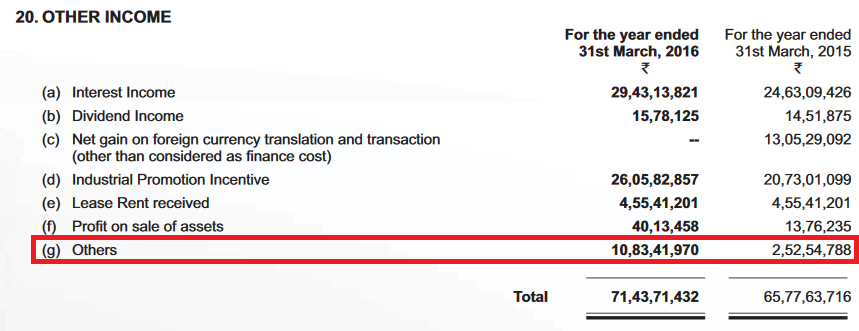

Apart from that, it is possible that while this purchase is extravagance personified, they rationalize the cost by chartering out the planes to third parties. There is a line item in the “other income” head that may account for these kind of activities:

It seems they have been doing this for a while; this is a registration of aircraft from 2006: http://dgca.nic.in/caris/reg-Jan06.PDF

Being > 15% of fixed assets doesn’t seem like great use of capital.

I wrote a detailed email to the compliance officer regarding the purchase of the planes. Surprisingly, I have got a response:

Dear Shareholder,

We have gone through your mail.

In response to your query raised in the mail, we will

like to discuss with you on this. You may please share your contact

details so that we can clarify on your queries, at your

convenience.

Best Regards,

Kishore P. Shah

Company Secretary

& Compliance Officer

FORCE MOTORS LIMITED

CIN L34102PN1958PLC011172

Will be sharing the details of my conversation with the CS as and when it happens.