I have made a few changes to the model portfolio which are summarized below. My thought process at this point is to reduce allocations to stocks trading at higher end of their valuation band, and also reduce allocation to very small cos, especially without any clear triggers. Market has been excessively rewarding, and in the past my major mistakes have come in these times. Lets see how many mistakes I make in this cycle.

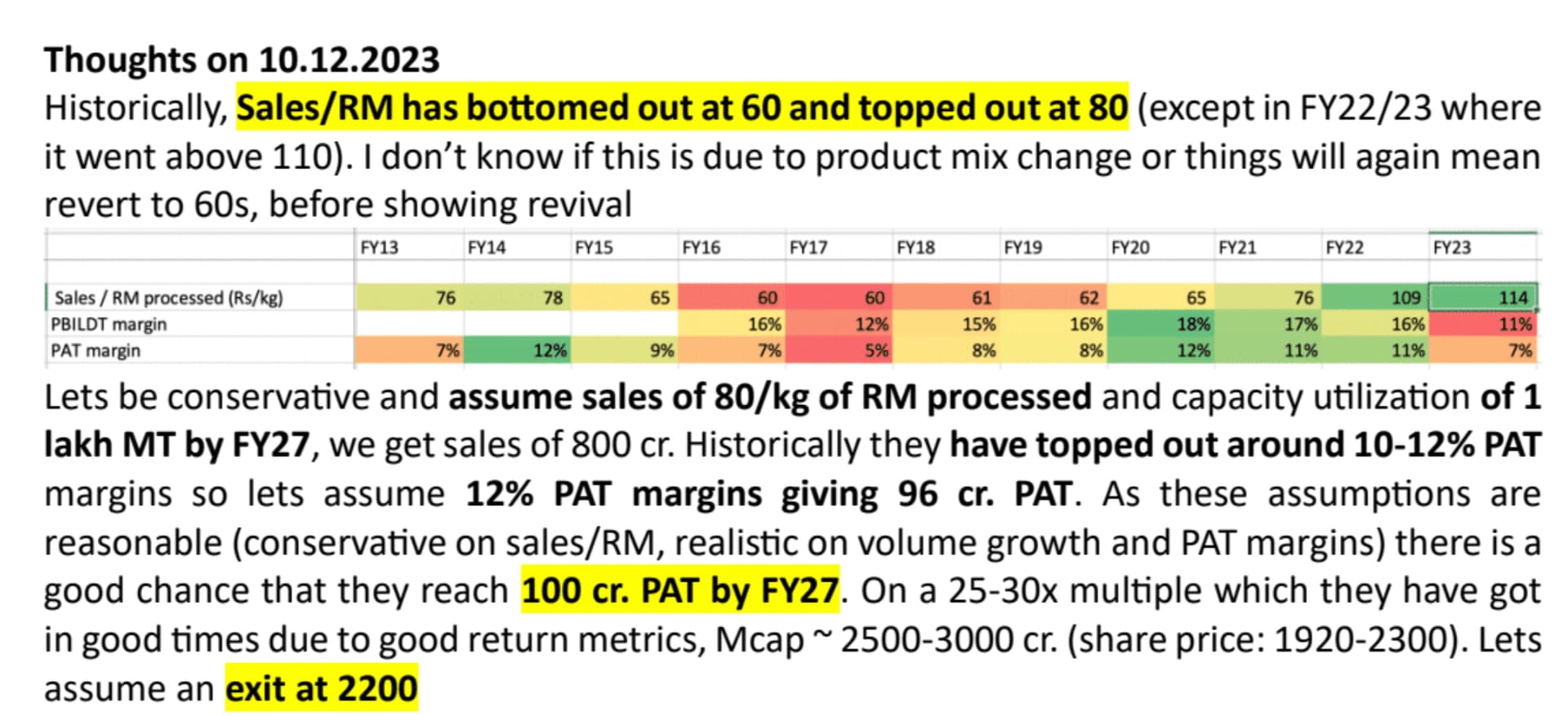

- Added 2% allocation in Fairchem Organics. I am looking to add chemical companies which have done capex, have good unit economics, and whose prices are down a lot. In Fairchem, logic is quite simple. Their new product (stearic and isostearic acids) are 2.5x realizations vs Dimer acid, has limited competition, and a large market size. Fairchem’s margins are at life lows. So there are two clear earning drivers (mean reversion in margins + new product growth). I feel they can reach 100 cr. PAT over the next 3-4 years. My detailed speculation around their future nos are below.

-

Added 2% allocation in Garware hi-tech. Garware’s VP thread is amazing to understand what differentiates them vs other packaging/polymer cos. Their PPF scaleup has been quite good and I feel if they can reach 2,500 cr. sales/ 500 cr. EBITDA by FY27, they will get atleast 10,000 cr. Mcap. I somehow missed buying it last year when their valuations fell to 10x, but I still feel there is good potential from current prices.

-

Increase allocation to Manappuram from 2% to 4%. I should have added to it when price had dipped below 100 but somehow failed to act. Business is clearly recovering and valuations are quite cheap. The Asirvaad IPO should also create some excitement around the stock. I feel its one of the best, yet one of the most misunderstood managements. Their capital allocation and scaleup since 2015 has been spectacular. @maheshkumar does an amazing job in sharing everything there is to know about the co.

-

Reduced allocation to Gufic biosciences, from 4% to 2%. Their stock price has moved up significantly in anticipation of growth from their large capex, as a result Mcap/sales is towards the higher side. I want to reduce my risks here.

-

Exited newspaper companies (DB Corp, Jagran). The idea of mean reversion in valuations is so simple, yet somehow unloved. Since I invested in 2021, DB Corp has returned 20% of my initial capital as dividends, and share price is close to 5x. Jagran has been a bit disappointing vs DB Corp, but it has been reasonable (7% dividend + 2x price). I am unwilling to pay 20x PE for slow growth newspaper cos like they are valued now. But single digit multiples on depressed earnings is something I am happy to bet on, especially because these companies are paying out earnings to shareholders.

-

Exited CV cycle plays (Ashok Leyland, Sundaram Finance). Both have been very rewarding but recent CV sales data suggests some slowdown and I am unwilling to go into a bad market with CV companies at their top.

I find that cyclical and value investing jells very well with my personality, its possible to make 3-5x by buying into a bad cycle and waiting for recovery. CV cycles are really predictable and one can make good returns by just betting on leaders during downcycles. E.g. I started buying Ashok Leyland in 2020 when its price had dipped below 50, since then it has been a decent journey.

Sundaram Finance is a CV lender with an amazing track record, and it got sold in 2022 and reached cyclical low multiples. One could see CV revival in monthly sales data, and it was a 2.5x in quick time, despite being a leader and being well followed. However, valuations now are closer to their upper end, thats why the exit.

Updated folio is below and cash stays low at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| Aegis Logistics Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Godfrey Phillips | 4.00% |

| P.E. Analytics Ltd | 4.00% |

| Gufic Biosciences | 2.00% |

| Ajanta Pharmaceuticals Ltd. | 2.00% |

| NESCO Ltd. | 2.00% |

| I T C Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 2.00% |

| Garware Hi Tech Films Ltd | 2.00% |

Cyclical (45%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| Chaman Lal Setia Exp | 2.00% |

| Fairchem Organics Ltd | 2.00% |

| KSE LTD. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (8%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Worth Peripherals Ltd | 2.00% |

| Sharat Industries | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

Its called Pareto chart, you can find it on excel.

No idea, sorry these are too complicated concepts for me.

Dont know how to think about these things. Promoter selling in isolation doesn’t provide any insights.

There is a lot of buzz that finally the battle will settle this year. For the kind of nos they are reporting, current prices are capturing a lot of downside already. But I dont know how to think of it, its been going on since 2019.