Nippon is a play on ETFs and business revival (in debt funds + international business coming from Nippon relationships). Honestly, I like AMC business where cash is not needed to grow and substantial amount is paid back as dividends. So rather than choosing one, I will like to play both (not UTI because of their higher cost structure). HDFC AMC has a banking parentage, so growth will be much easier.

Both Inox and wonderla are facing similar headwinds. My bet is not really looking at the next 1-year, but more from a larger trend perspective. For Inox, the trend towards multi-screen exhibitions has been established and its only accelerating.

I preferred Inox because of their better balance sheet and more conservative accounting. A couple of bad years doesn’t have much impact on terminal value of such businesses. About OTT, this is an endless debate and I will prefer looking at number of footfalls. I don’t see a lot of other entertainment venues for an urban Indian. There was a recent JM Financial report that showed the economics of OTT vs cinema for movie producers and there is no way OTT can take over theatres unless there is a large change in underlying economics.

As of today, I have sold my 2% position in Infosys, reduced allocation in Indigo from 4% to 2% and invested the money in HDFC bank (at 4% position size).

Assumptions Infosys: FY20 revenue: 90’791 cr., will grow @10% to 146’220 cr., Earnings (28% PBT margins): 146’220*28%*75% ~ 30’706 cr., Sell at 22P/E ~ 675’532 cr. (share price: 1587). Incremental returns are ~6%. HDFC bank: FY21 book value: 210’443 cr. (382/share), share count ~ 551.23 cr. In FY25 book value will grow @18% to ~ 408’000 cr. Long term share dilution ~ 2% i.e. 597 cr., Book value per share: 683 (including impact of dilution). I would like to sell at >4P/B (share price: 2732). Incremental returns are ~19% (adding 1% dividend yield)

Risk reward seems to be more favorable for HDFC bank vs Infy (hence the switch). Updated portfolio is below.

Hi Harsh, Given the severity of the Covid 2nd wave either the Supreme court may have to again reinstate the moratorium on NPAs else I expect tough quarter or two for banks…

IT on the other hand seems to be going strong with revenue growth above the 3 year average…

While I like your valuation approach on selling and buying I am slightly not sure if it’s too early for the switch…

Hey! Yes I evaluated Jubilant Life even before their demerger and couldn’t find much differentiation in their line of pharma business vs other generic players (except the fact that Jubilant was cheap + had more debt). The Jubilant management has failed to reduce leverage since FY14, this despite the fact that pharma business throws out cashflow. They also had a few bad acquisitions. In a nutshell, I preferred my pharma basket (Ajanta, Biocon, Cadila, Divis, Lupin, Natco). This covers almost everything there is in generic pharma (oral solids + biosimilars + custom synthesis + Para IV + inhalers + injectables + vaccines).

Now coming to Ingrevia, I was attracted by cheapness + close to net debt free balance sheet + cost leadership in certain quasi-commodity chemicals. Now lets see how business performs.

These are things which I don’t give much credence to. If you go up in the thread, you can see my general investing thought process. I was buying IT (Hcl + infy) in 2017 when there was pessimism all around it, consumer cyclicals (like indigo, inox, wonderla) when there was a lockdown, metal companies (maithan, nalco) when there was no domestic demand and almost everything had to be exported. So, buying and selling for me is not a function of near term business performance, but a difference between current stock price and my assessment of underlying value. Sometimes, I am right in my assessment and sometimes I am wrong. As long as my (hit rate*average gains/losses > certain threshold), I will do okay.

If we look historically over the last 15 years, HCL has been the fastest growing large IT company. This is because they acquire other assets and capabilities (which reduces free cash generation) thereby reducing net shareholder distribution. However, this strategy has allowed them to grow sales at a higher clip (~6x over last decade vs Infy’s growth of 4x and TCS’s growth of 5x). This is also one of the reason they trade at a cheaper multiple.

In a recent industry seminar, HCL said that they aspire to double sales over 5 years. If they manage to accomplish this feat, they are trading at cheap valuations. That’s why I hold HCL and sold Infy.

Hello Harsh,

Dumb Q to ask but still i will ask : I couldnt follow the Infosys vs HDFC bank logic ? Is there a bit of a layman explanation of your calculations as i am fascinated how you calculated the risk/reward of future value ( Incremental returns ) …i would like to learn this …any source for a beginner like me …? or a more step-wise explanation of how to calculate this …?

Basically, I expect ~19% returns from HDFC bank vs 6% from Infy. I evaluated HDFC bank on the basis of P/B (assuming exit P/B ~ 4x; book value growth ~ 18%; long term share dilution ~ 2%). For Infy, I assumed 10% sales growth, 28% PBT margins and exit P/E of 22. NOTE: These are simply guesses and have no impact on the underlying business or anything for that matter!

I have explained this in an earlier post, my approach in selecting real estate companies was top-down. I wanted exposure to developers which cater to markets with lower inventory (places like Pune, Bangalore, Hyderabad, Jaipur). MMR is one of the highest inventory markets and Sunteck has a very large chunk of sales from Mumbai. Although, there are lots of finer micromarket dynamics which I do not fully appreciate. Also, Kolte has managed the downturn very well (no capital dilution, controlled leverage). Valuation wasn’t the primary lens, although almost all small residential developer is cheap.

As of today, I have reduced allocation in Indigo from 2% to 1% and increased allocation in HDFC from 3% to 4%. Cash continues to be at zero.

Over the past year, I have been testing out a deep value strategy i.e. buying companies which are ridiculously cheap. I have categorized them as:

Net nets (working capital bargains): Mcap below 2/3rd of net working capital

Companies with above average return on capital over a business cycle (20%+) trading close to or below their book value

Companies with moderate return on capital (12-15%) trading below half times their book value

The idea is to buy a bunch of these companies and hope for mean reversion over a 2-year time frame. If it doesn’t happen, sell it. If mean reversion happens, see if the business can find a place in the model portfolio, if not sell it. Last year, a large number of companies started meeting these criterion. As this was still experimental, I bought small positions in a few companies which are stated below.

Time Technoplast (bought it below 0.5x book value, this business should trade atleast at its book value given they make 12-15% ROCE).

RACL geartech (bought it around its book value, a business that has grown during an auto downcycle speaks a lot about their business characteristics).

Atul auto (bought it at ~1.3x book value, this should trade at a large premium to its book because they make >30% ROCEs).

D.B. Corp (this was a recent buy below its book value, DB should trade at a premium to its book value because they make 20%+ ROCEs).

Going forward, deep value bets will start to be part of the model portfolio, given the very attractive risk reward they offer (low downside, potential optionality for large upside). I will initiate their positions at 1% size and see how business develops. The current model portfolio (without deep value bets) are stated below.

I see that you have consciously been fully invested with zero spare cash.

Just wanted to know your thoughts on it since it means that you wont be able to add any meaningful quantity to your portfolio if a correction sets in…

As of today, I have reduced position size in Natco Pharma to 1% from 2%. This generates 1% cash.

In the past few weeks, I have been working on a comprehensive portfolio allocation framework capable of handling different types of stocks (cyclicals, core compounders, special opportunities, Graham net nets, deep value, etc.). The underlying idea is to create a Swiss army knife which can take advantage of different variants of market inefficiencies. I will post the details in the coming weeks, and this will also result in significant churn in the underlying portfolio. Updated portfolio for now is below.

Would you mind sharing your thoughts on reduction in NATCO allocation when Company got approval for a blockbuster drug ? Is it because you think that CMP already factors in potential opportunity ? Or is it because of some other business risk ?

As of today, I have sold my stake in Indigo (fair valuations, slightly hazy future) and reallocated the remaining 2% cash in Amara Raja Batteries. I used to own Amara Raja but sold it in April 2019 when the news of discontinuation of collaboration with Johnson Controls came out. Over time, it became clearer that the true edge of Amara Raja was not superior technology, but a superior distribution and higher brand spends. Sales growth has been subdued over the last few years due to auto slowdown and this seems to be coming back (also reflected in Castrol’s numbers). Additionally, the industrial segment seems to be coming back. Given the giant CAPEX spend by Amara Raja over the last few years, its now time to sweat out the assets and generate free cash. Recently, Exide is growing at very similar rates to Amara Raja and this remains a key monitorable. Lets see what happens going forward! Updated portfolio is below.

Companies

Weightage

HCL Technologies Ltd.

6.00%

I T C Ltd.

6.00%

PI Industries Ltd.

6.00%

Power Grid Corporation of India Ltd.

6.00%

Larsen & Toubro Ltd.

6.00%

Ajanta Pharmaceuticals Ltd.

4.50%

Kolte-Patil Developers Ltd.

4.50%

Ashiana Housing Ltd.

4.50%

NESCO Ltd.

4.50%

Maruti Suzuki India Ltd.

4.00%

Suprajit Engineering Ltd.

4.00%

Manappuram Finance Ltd.

4.00%

HDFC Bank Ltd.

4.00%

Housing Development Finance Corporation Ltd.

4.00%

HDFC Asset Management Company Ltd

3.00%

Reliance Nippon Asset Management Co

3.00%

CARE Ratings Ltd.

3.00%

Lupin Ltd.

2.00%

Avanti Feeds Ltd.

2.00%

Cera Sanitaryware Ltd

2.00%

National Aluminium Co. Ltd.

2.00%

Wonderla Holidays Ltd.

2.00%

Maithan Alloys Ltd.

2.00%

Cadila Healthcare Ltd.

2.00%

Inox Leisure Ltd.

2.00%

Jubilant Ingrevia Ltd

2.00%

Amara Raja Batteries Ltd.

2.00%

NATCO Pharma Ltd.

1.00%

Jamna Auto Industries Ltd.

1.00%

Ashok Leyland Ltd.

1.00%

Cash

0.00%

Valuations + inherent uncertainty in my understanding of future sales growth. Revlimid opportunity has been known for a while now, the approval is simply a confirmation. Natco is an optionality position for me and I scaled it up when prices became very attractive in 2019/20. However, I don’t put more than 2% in an optionality bet. I will hold on to the rest of shares to see how business numbers come out (we have to wait for FY23 for revlimid numbers).

Looking at your value-picks, you must hv anticipated or considered this - Why DB Corp over Jagran Prakashan or not both as a value bet on newspaper stocks?

I took a position in Jagran whn it was avlbl for less than cash + Music Broadcast valuation. M still holding that & whn thr was sm recent news over Google paying news cos. for content, it seemed to be a kicker for these cos. just as it happened in music industry. The news source is shared on VP bt I can share again if u want.

Still it vl be nice to know ur views on the question above.

In this series of posts, I will share my thoughts on position sizing, how I have approached it in the past, how the results were, and what refinements I have brought about it.

The past results

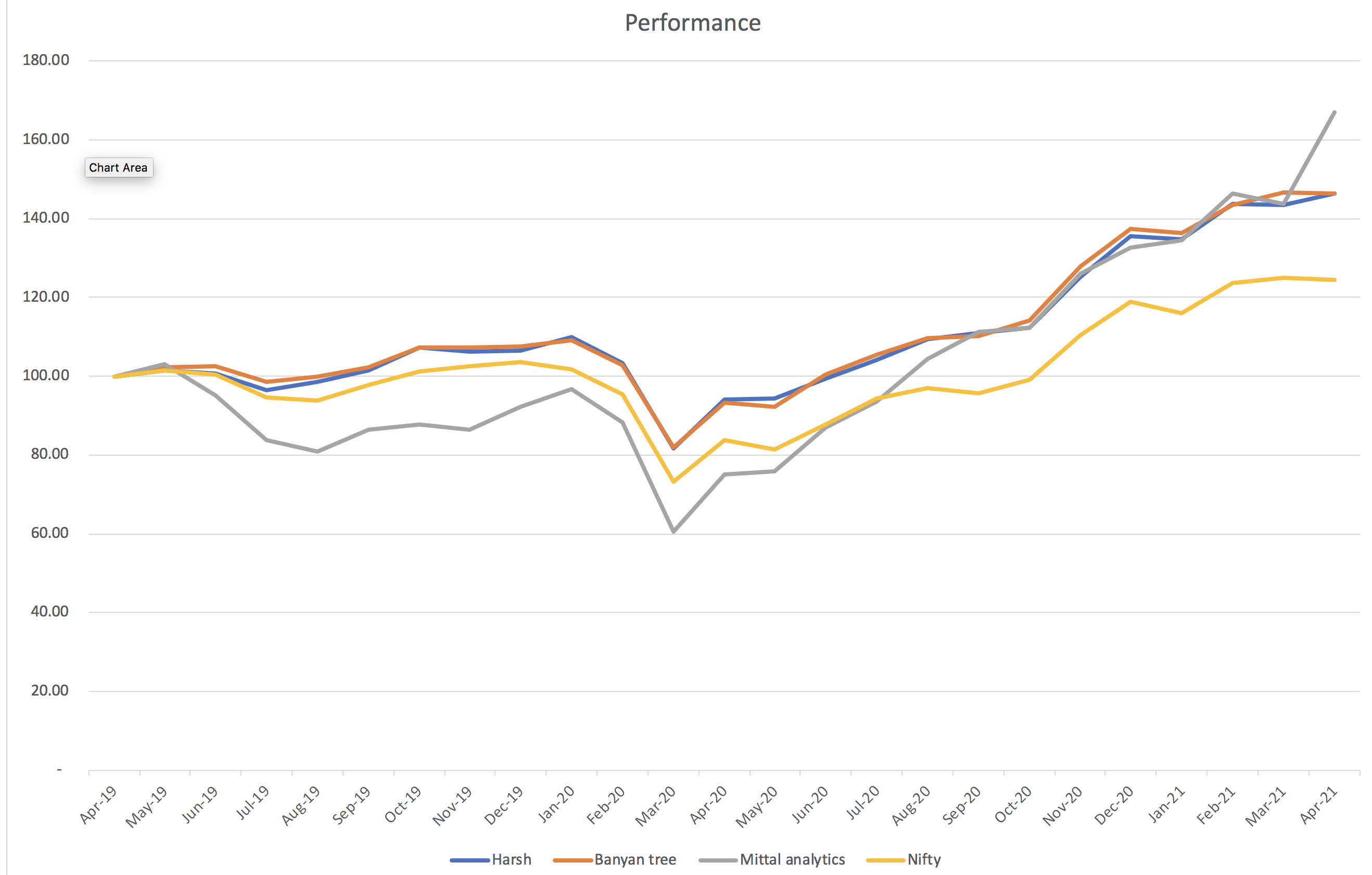

I benchmark myself against three portfolios:

Nifty 50: Reflects opportunity cost

Banyan tree PMS: Quality and valuation driven firm with one of the best publicly available track record across market cycles (including 2008)

A microcap maverick like Mittal Analytics (public track record starts in 2019)

Here is how returns have fared over this 2-year period.

All the 3-strategies has outperformed Nifty. My strategy is much more closer to Banyan Tree (quality + valuation). A more small cap focused strategy creates much higher drawdowns and produces excess returns in good times.

What do I want? Drawdowns like Banyan Tree and outsized returns like Mittal Analytics which is impossible for someone like me.

What can I get? Behaviorally, I want absolute controls on longer term drawdowns by selecting good companies and not overpaying. However, I want to spice up the returns with positions in bombed out cyclicals which can produce excess returns in good times.

Position sizing

I used to size a position anywhere between 1% to 6%. My expected returns were 15% and I used to allocate 6% into companies that were no brainer opportunities to generate 15%+ returns. These were generally large companies with good institutional coverage and whose performance could be studied across cycles. This is how this part of portfolio has done.

6% companies

IRR Returns until 28.05.2021

Ajanta Pharmaceuticals Ltd.

24.20%

Bajaj Auto Ltd.

20.69%

HCL Technologies Ltd.

38.10%

InterGlobe Aviation Ltd.

19.52%

I T C Ltd.

-0.20%

Larsen & Toubro Ltd.

17.60%

Lupin Ltd.

-1.10%

Natco Pharma

20.70%

PI Industries Ltd.

59.60%

Power Grid Corporation of India Ltd.

19.70%

Reliance Industries Ltd.

0.00%

Reliance Nippon Asset Management Co

26.00%

AVERAGE

20.40%

Out of the 12 companies, I was right on 9 i.e. a hit rate of 75%. For me, anything >60% hit rate is good. As its clear that I have been right more often than wrong in large positions, I should ideally increase my %. This is one change which I am bringing about in my portfolio.

In the next post, I will illustrate my thoughts on position sizing and the refinements I have brought into it.