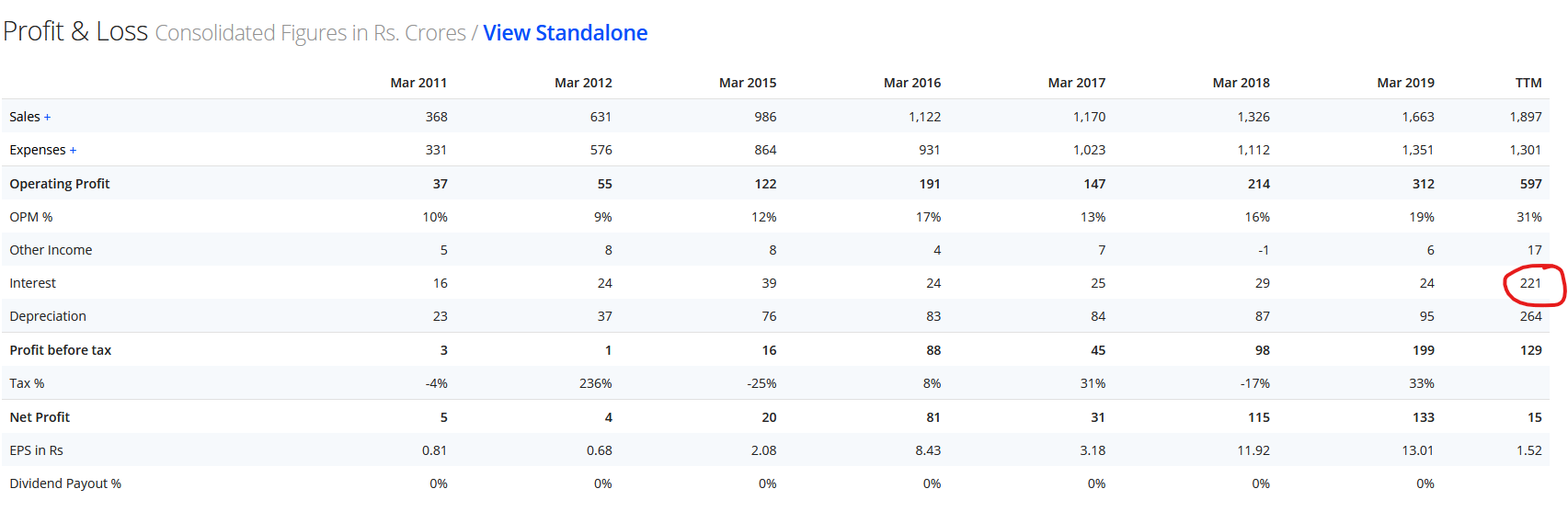

Can someone help me understand why Screener is reporting a very high interest expense of 221 cr in FY2020? I do not see any new borrowings by the company.