Good set of results from Manappuram (FY21 PAT growth of 16.5%, ROE ~ 26.2%, Book value growth of 27% and standalone capital adequacy of 29%).

-

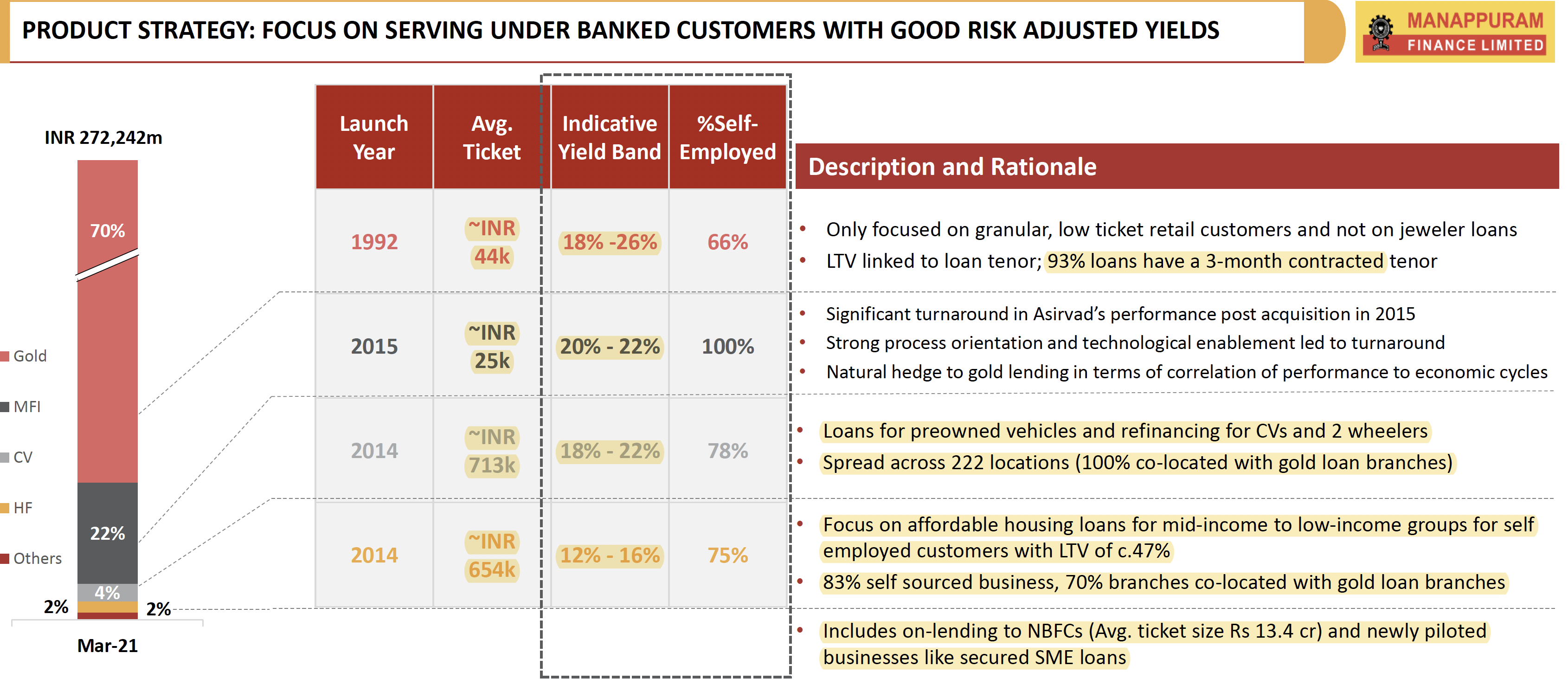

Company is experimenting with a new business of on-lending to NBFCs (current average ticket size is 13.4 cr.) and secured SME loans.

-

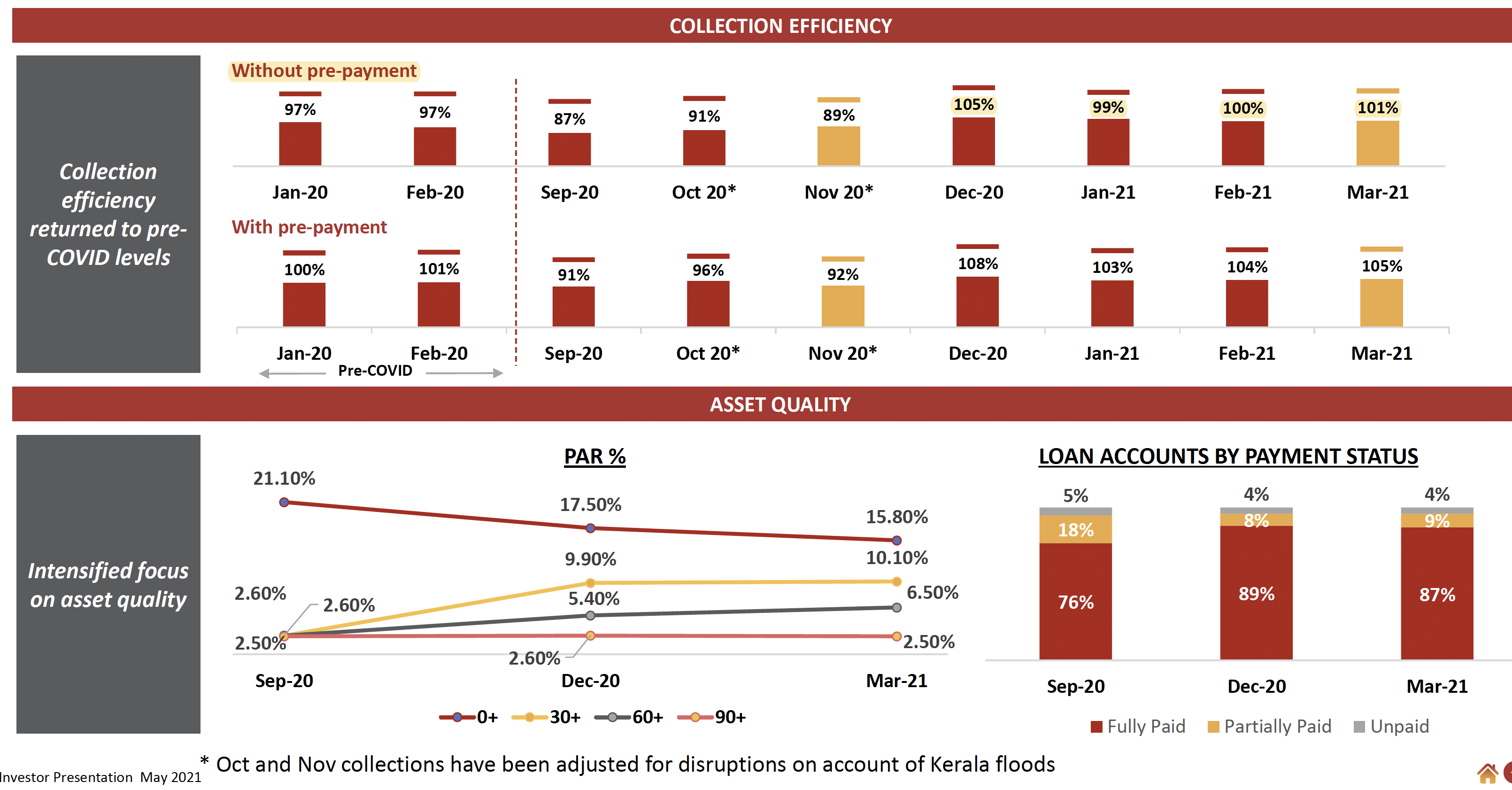

Gold auctions during the quarter was 404 cr. vs 8 cr. during the previous 9MFY21. This was because of increased defaults. Also, there was a lot of foreclosure of loans. The strategy of short term lending with 3-M loans accounting for 93% of outstanding gold loans have produced very good results (ROA: 6.9%, ROE: 27.7%) despite de-growth in gold tonnage (65.3 vs 72.4 in Q4FY20). Also the strategy of keeping LTV at 60% has paid rich dividends, because with gold prices decreasing LTV only increased to 71% which is below RBI’s benchmark of 75%. Current LTV is 63%. Increased competition hasn’t brought down net yields much (FY21 yields: 24.9%)

-

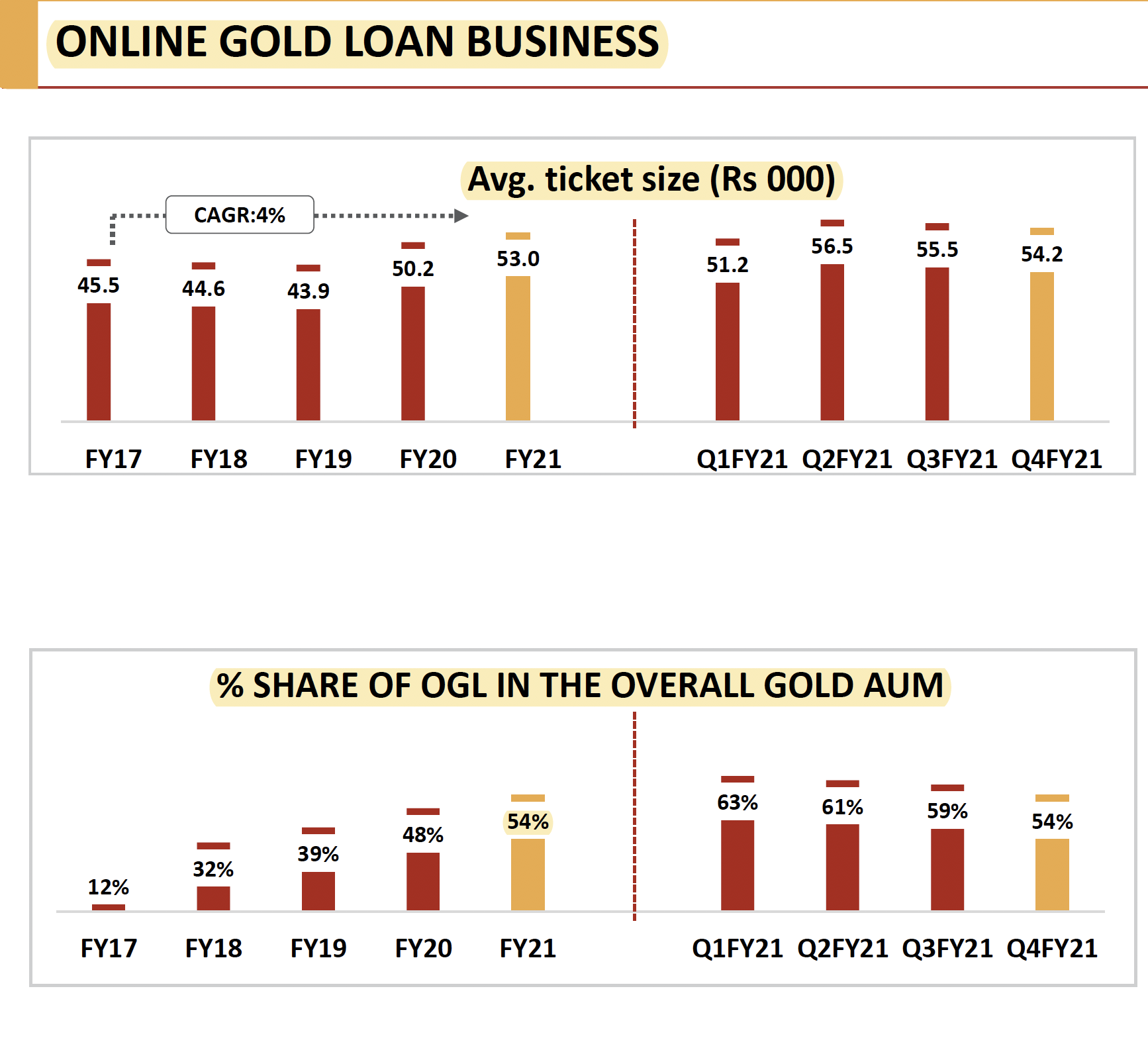

Online gold loan now accounts for 54% of outstanding gold loans (down from 59% in Q3FY21). The sharp decrease from 63% in Q1FY21 suggests online gold lending is more volatile compared to physical lending. Also, the average ticket size is higher in online gold lending (53’000 vs company average of 44’600).

-

The company has a very stable borrowing mix with bonds + ECBs accounting for 51.8% of outstanding borrowings. Cost of borrowings have also come down to 8.8%

-

MFI book is very well provisioned (net NPA ~ 0; provision ~ 5% of book). Collection efficiency improved to 100% (without pre-payment) since December 2020 which suggests their MFI business sprung back very quickly. This is in-line (or slightly better) compared to leaders like Credit Access Grameen. AUM/borrower is below industry standards (at 25’400). Cost of funds have come down to 10.5%. Also they were able to garner 26% of borrowings from NCDs (more stable funding) which is even better than Credit Access.

-

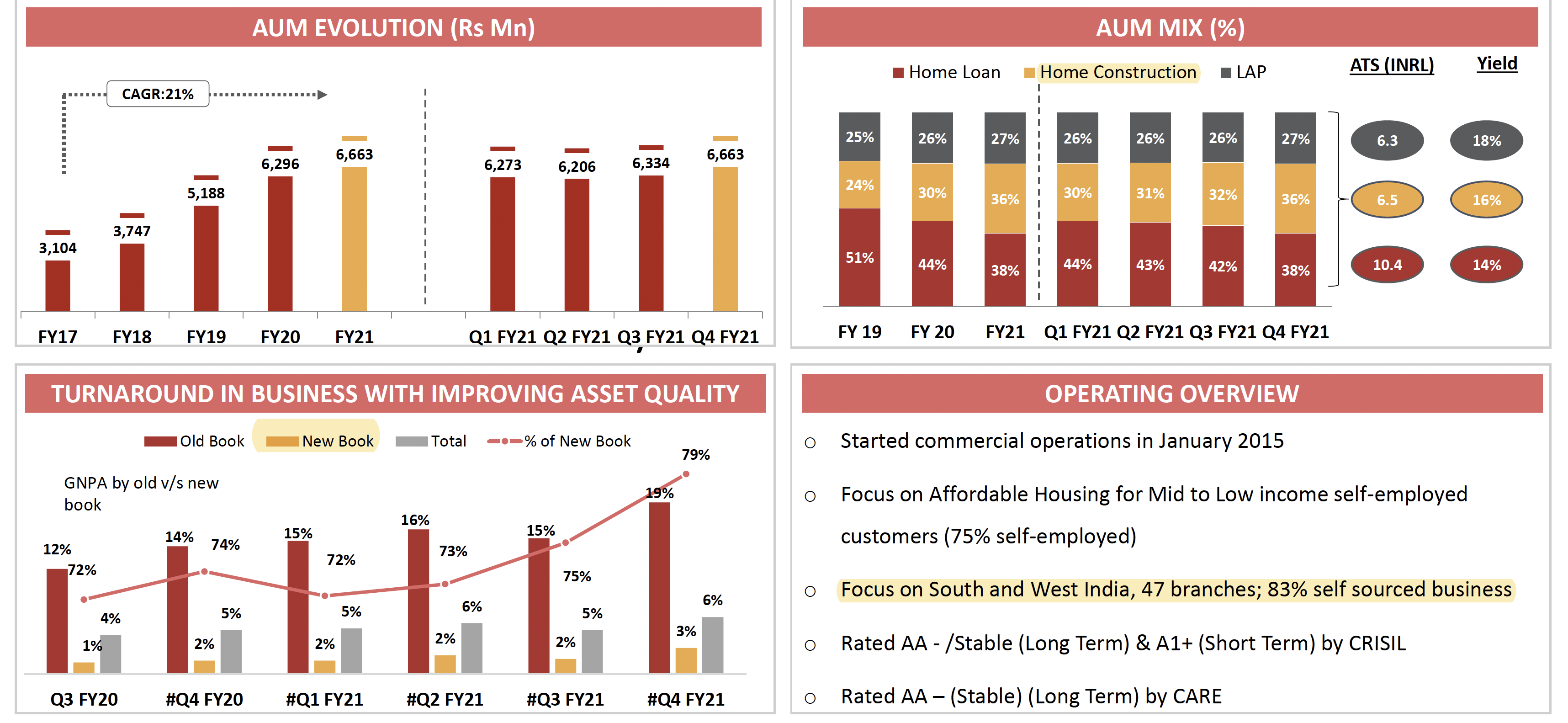

Housing loan business is doing okay with NPAs on the new book at 3% and 6% (including old book). There has been growth in self construction book, LAP has been kept constant.

-

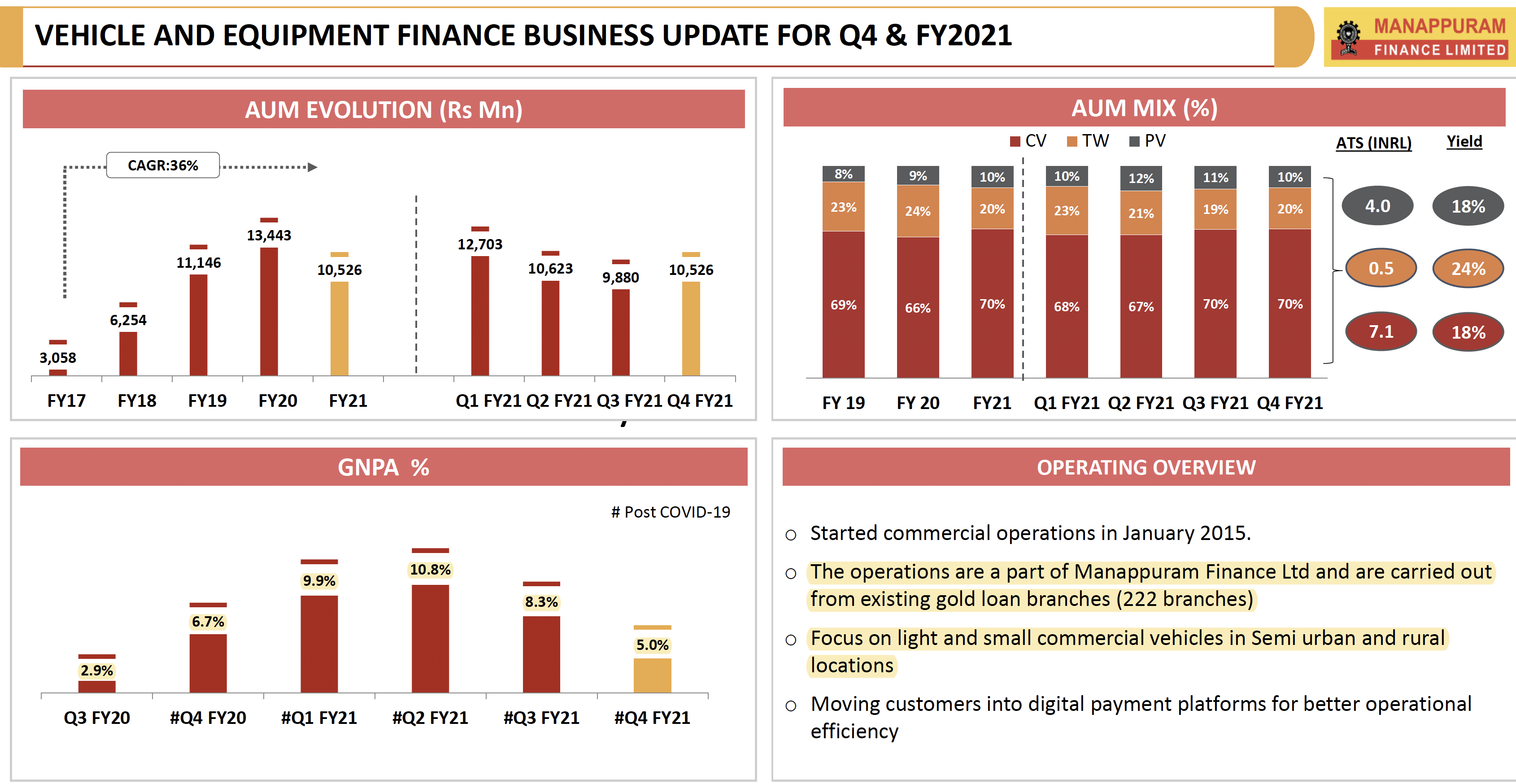

There has been a big improvement in vehicle financing book with GNPAs coming down to 5% from the peak of 10.8%. Is this because of a structural improvement in this business or due to Manappuram’s strategy on focusing on small vehicle owners or due to de-growth in book?

Disclosure: Invested (position size here)