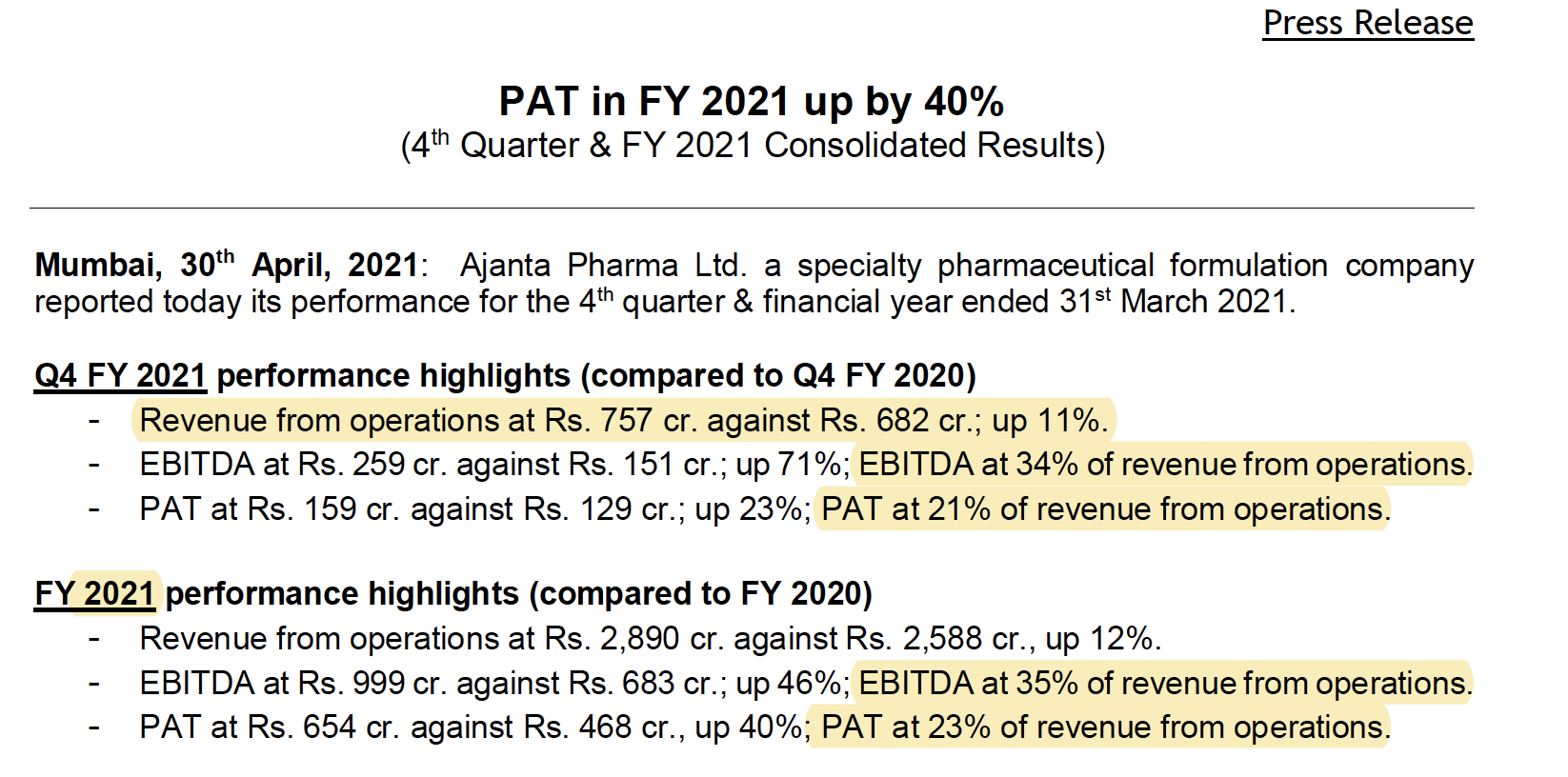

Stable set of numbers from Ajanta.

Here are my notes from the concall

- US:

o API sourcing: Outsourced and do not plan on backward integration. Have strong partnerships and will stay focused on this approach

o Growth: For the next couple of years, comfortable with product pipeline in oral solids to achieve desired growth; Filed only 2 ANDAs in FY21 because of the hard lockdown in the beginning of F21. Currently R&D is not operating at full capacity, but will try to maintain 10-12 ANDA filing in FY22. ANDA approvals are largely in-line with filings, and they have been fairly consistent with both filings and launches in US barring FY21. US strategy is focused on being very calibrated with the filings so that the end products actually get launched

o Pricing: Has been much better post buyer consolidation compared to scenario few years back. Competition will always be there and now it depends on the strategy adopted by individual company; Will not like to give any future guidance on growth

o R&D can go up to 6% of sales - Domestic business

o Reason for superior growth: Introduced very good products in FY20 which yielded results in FY21 (such as new brand launches in rheumatoid arthritis). Had 21 new brand launches in domestic market (5 first time launches) in FY21

o Dermatology: Have four teams in dermatology which held a lot of webinars and group meetings to bring the division back to growth. Expect productivity improvement going forward

o Cardiology: 5-6 lakhs productivity per month by 2 teams and the rest 2 teams are catching up

o Ophthalmology: at optimum MR productivity compared to #1 and #3 player; Not a large market, so productivity will be lower compared to other divisions

o With commissioning of Guwahati facility, a large of outsourcing is discontinued. Margins will be similar to current levels and will get better control on product + income tax benefit

o Takes 4-6 years for building a domestic brand to achieve peak sales

o Invested 25 cr. in ABCD Corp. (bring in more efficiency in domestic pharma chain) - Working capital: Higher inventory in FY21 (98 days vs 71 in FY2) was due a mix of API and formulation; Lower receivable days of 95 in FY21 vs 111 in FY20 should persist going forward

- CAPEX: FY21 capex ~ 150cr. (30cr. on corporate office), FY22 capex will be ~ 200-250cr. (largely maintenance (should be 150-200cr.) + expansion of corporate office which will be 60-80cr.). Fixed asset turns for FY21 ~ 1.75x (on net fixed asset) and should improve going forward. Current gross block ~ 1765cr.

- Africa institutional business: going forward wish to make similar level of sales (outlook is very hard to give)

- Improved gross margins of 78% is due to better product mix and wearing off the impact of FY20 product recall; Should be in the range of 75 ± 2% gross margins going forward

- 176cr. sales in Asia and 97cr. sales in Africa Institution business in Q4FY21

- Seeing disruption in Asia and Africa business but this should stabilize soon, do not see any long term disruption

- 34% EBITDA margins should go down in the future because of exceptionally low costs in H1FY21

Disclosure: Invested (position size here)