I will recommend you to first read the financial statement of Indigo before commenting, the borrowing number that you probably saw on screener is not financial borrowing. These are lease liabilities. In the new accounting rules (IND AS 116), companies have to state leases that are more than 12 months on their balance sheet. Its not financial leverage! Company is net debt free (their borrowing is 2’434.3 cr. and their cash balance is 20’376.9 cr. as of FY20).

And thank you the questioning, however I will really appreciate if you do a first level due diligence before making a comment. That way the conversation is useful for both of us.

Lease liabilities are themselves an obligation in long run which they eventually have to pay. And cash reserves they have to maintain to be deployed in difficult times or bad years with higher operating capex. While I am not arguing about its future prospects, its a risky business. Other players are also getting into scene of affordable pricing. I just don’t have a knack for business that compete primarily on pricing.

I don’t have any firm opinions on P/E, the idea for me is to try and understand what growth assumptions are captured in the current market price. If I have a different opinion (eg: higher growth rates or higher longevity), I express it by buying the stock. Thats all there is to investing.

About BLS, I haven’t looked at it and am not qualified to comment on their business model. On the face, it seems to be a capital light business. However, margins are all over the place. I need to understand the underlying business dynamics to better understand their business levers. Thanks for pointing it out.

About your point about float, a low float aggravates stock price on the upside and on the downside. There is nothing more to it.

About alternatives to Indigo, I looked at VIP as an alternative in 2018. The reason for choosing Indigo over VIP was the competitive intensity in bagpack businesses. Also, their prices were clearly capturing future growth.

Now about moats, low cost advantage due to benefits of scale is a big moat. Indigo has that. However, airline business is a pure commodity kind of a business, where growth will go to the lowest ticket price provider. This game goes on for a while until someone goes bankrupt (eg: Jet in 2019), and then the encumbants benefit for a short time. This is a classical commodity cycle. So I try and buy commodities when they are in a downcycle and hope and pray (everyday!!!) that cycle turns. Because when cycle turns, the amount of operating leverage offered by these companies is really awesome and market starts extrapolating it in the future. That’s when I try to sell. Lets see if it works out with Indigo!

Btw P/E ratios do not inherently have high growth assumptions. You can think of P/E as an “area under the curve” where the X-axis is time and Y-axis is some combination of earnings growth and earnings growth derivative.

A company that will grow at 12% pa for 200 years is certainly ok to give a P/E of 70 to. In some cases the “high management quality” or high “industry quality” (retail and FMCG and such) is another way to incorporate the “trust” in the longevity of growth. Think 10% CAGR for 30 years instead of 17% for 10 years.

The difficulty with high P/E companies is that they don’t have much room for messing up. Even if HUL grows at 10% PA for 20 years, I think it can maintain the high PE for the next 10-15 years. The reason the probability of their messing up is low is due to the high quality management as well as the high quality industry (apart from and in addition to high quality of the company). Just my 2 cents.

If something doesn’t make sense to you, don’t do it. There are many ways that work in investing, find yours and stick to it. I am sure your calculations about Asian Paints are correct. I dont have asian paints in my portfolio, maybe you should ask someone who knows more about the business than I. In this business cycle, I have largely stayed away from consumers as I don’t understand their valuations. But then I don’t understand a lot of things, so its fine!

I guess there is some confusion about valuations, honestly its not the hardest part of investing (its probably the simplest part). If you need a lesson 101 of how assets are valued (eg: bonds, stocks, or anything that produces cash), look at this lecture from Samit Vartak. Thinking from a bond perspective gives a lot of insights into valuations and also tells us why P/E is not a useful heuristics. What matters is book value, return on equity, reinvestment rate and cost of capital. These variables capture the science part of valuations, everything else is more related to business understanding and luck!

How is P/E an integral(area under the curve)??? It’s a simple ratio. To get into calculus there is no correlation what so ever between the growth and change in PE all over the world. If there was even after a company stops growing it should have traded at the same PE multiples it traded before at its peak. It’s purely based on investor’s sentiment. While I don’t know if such P/Es will sustain, I might speculate that 10 percent CAGR may be possible. Buy how is that good when you might have some other businesses with predictable economics for next 10-20 years at lower PE multiples?

Oh yes!!! Luck. Couldn’t agree more. One thing that cannot be valued but that will completely define an investment. Daniel Kahneman in his noble prize winning thesis has give it such an importance that ironically, it seems that the sheer success of his thesis has also been based on luck.

Just a thought…how about playing it via travel insurance… although it comes into picture only in international travel and not a significant part of only listed private general insurance company…

Hey Harsh, I have been following this thread for a while now and the insights you provide are very useful

Could you throw some light on how you calculate your yearly returns?

Calculating returns for a portfolio is very easy from say 1st April XXXX to 31st March XXXX if all the transactions have been carried out before the start date,but I wonder how you adjust for incoming cash into the account and transactions carried out just before the Financial Year ends?

Thanks!

I track 2 metric, monthly return (which I call absolute return) and IRR return.

Monthly return: For a given month if my starting portfolio value was 100 and I bought stocks worth 10 and at the of the month, my portfolio value is 90 then the monthly return is (90-100-10)/(100+10) ~ (-18.18%). This is what I call absolute return.

IRR return is computed by putting all transactions on an excel sheet along with their respective dates, and use the XIRR function.

Generally, both these returns are quite close, if there is not a large amount of influx/outflux from the portfolio.

In-line with my previous post, I have sold out Divis Laboratories (1% position) completely and switched it to Cadila Healthcare (1% position). Cash level remains at 3% and I am looking for opportunities to deploy the same. This keeps my broad pharma allocation at the same level, but I get a nice asset at a much cheaper price. Cadila’s biosimilar portfolio is something worth looking at. They have also been growing their generic business well and have focused on de-risking their US business by growing their biosimilar business in emerging markets and in India. Their valuations are below long term average (EV/sales ~ 3 x vs long term EV/sales of 3.5-4x). Updated portfolio is below:

Read ur other post regarding Real Estate cycle.

My question is why you didn’t considered Purvankara vis-a-vis the RE stocks in ur portfolio - Ashiana and Kolte Patil?

As of today, I added 1% position to NALCO increasing its weightage to 2% in the model portfolio. This post clearly summarizes that aluminum and alumina prices have reached pre-COVID level. However, the company share prices are not reflecting it. That’s why the increase in allocation. Updated portfolio is below:

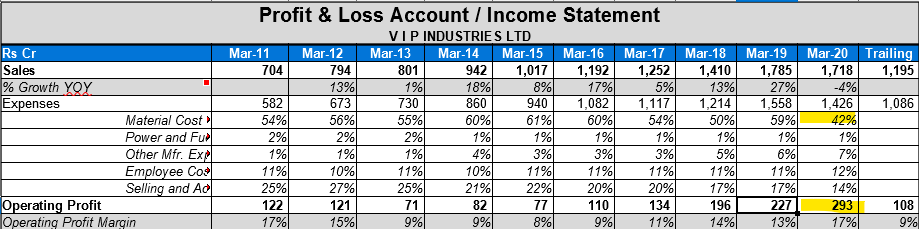

Have you looked at VIP Inds recently? What are your views considering the price has corrected from the 2018 highs? It seems that the company is aggressively moving away from China for its raw materials to its own plant in Bangladesh. This seems to be reflected in the Income Statement as well -

Hey! I have listened to the recent interviews of their management where they mentioned about Bangladesh. Valuations are much more attractive now. Here is very naive projection. Let’s say they are able to get back their peak sales by FY22 and grow at 11% (their long term growth rates) over the next 3 years. That will give a topline of ~2400 cr. When operating leverage kicks in and raw material prices are soft, their net profit margins can easily go upto 10%, i.e. profits of 240 cr. Market generally gets bullish in these scenarios and can easily give a 25x multiple if trailing growth rates look high (Mcap ~ 6000 cr.). The IRR returns (including dividends) will be ~12%, and my assumptions are conservative (i.e. 0% growth until FY22, 11% growth post that). A key monitorable for me would be their market share, there are lots of cheaper bagpacks available, so as long as management can maintain market share this can be interesting.

Another way to look at it is how has market valued them in the past. Here are the EV/sales numbers taken from tikr.

On a FY25 sales number of 2400 cr., an EV/sales of 3x (which will be probably available during a bull market) will translate into a EV of 7200 cr. So, a probable doubler from these levels.

Thanks for the clarification! Yes. I would also assume that they should be able to grow atleast 10% from FY22 onward. I understand that this is not like Indigo as you have rightly pointed out earlier in this thread where there is a clear monopoly that is happening primarily due to debt laden peers in the airline industry. But that being said, it seems there are only a handful of players (VIP, Samsonite, Safari). From the respective threads and other research, I understand that these companies have built a strong network of supply chain management which is very difficult for a new entrant to replicate soon.

That being said, the biggest threat could be Amazon and Mi who have launched bags and travel luggage online. VIP currently operates at various segments (< 3000 Rs, 3000 - 6000 Rs and > 6000 Rs). Now are they going to face a tough competition in all the 3 segments is something that needs to be seen.

In terms of advantages I see that -

They are early movers in terms of setting up sourcing input from outside China. For others, setting this up might take a lot of time

Brand Recall. They seem to have a good brand recall. Any new entrant would have to spend a ton on Advertising

VIP Carlton offers lifetime warranty. Even Samsonite does not provide that. I read somewhere in the VIP thread they cannot change their warranty policy only for India (which makes sense).

These big ticket purchases (both in terms of size and price) will still have a good share of sales in retail stores. People would want to inspect the material before buying.

Since these bags occupy a lot of space, only a few brands can be accommodated in these stores.

Great to see your active interest towards markets.

Do you work at present? Am unsure how you manage time and work together or are you full time investor?

Saw your articles, you do good set of research whereas in my case am always caught in a act of work + learning (technology as am IT professional) + read about stocks (during travel or during lunch hours)

How do you handle and learn in case if you are at work?

I am a hobby investor, I have a full time job as a scientist. Its in the last few months that I have started sharing a lot of my research. I simply like tracking companies and building up my personal knowledge base. About managing work and time, its really personal and varies from person to person. For me, I take short breaks to track companies. Most of my in-depth reading such as annual reports, industry structure, etc. is during weekends or during holidays. Also, given that I live alone I have plenty of time to read. Not sure how long this will persist though.

As of today, I have added 2% position in Suprajit Engineering to the model portfolio, bringing down the cash level back to zero. Its an unusual auto ancilliary company with higher margins (of 14-16%) compared to peers (~10%). Their focus on after market has enabled them to earn higher margins. Management of Suprajit are hungry, CEO is young, and they have managed to compound sales by 20% for a very long period of time. They are still very small in the broader context, being only leader in cables business, and currently trying their hands in lights business. EV doesn’t impact them as quantum of cables are same in an electrical vehicle, and EVs need lights. My naive projections are below.

FY20 sales: 1563 cr., assuming FY21 sales will be 1500 cr., @15% growth FY25 sales: 2623.51 cr.; To sell at 2.5x sales; EV ~ 6559 cr., Debt for FY20 was 391 cr., Debt in FY25 will probably compound at the same level as increase in sales (in sync with past) ~ 391*1.15^5 ~ 786 cr., Mcap ~ 5773 cr. (share price: 413). From current level of 166, the future potential returns are ~20% (+1% dividend yield). If price drops to 100-125 or growth improves, I will increase my position size. The updated portfolio is below.