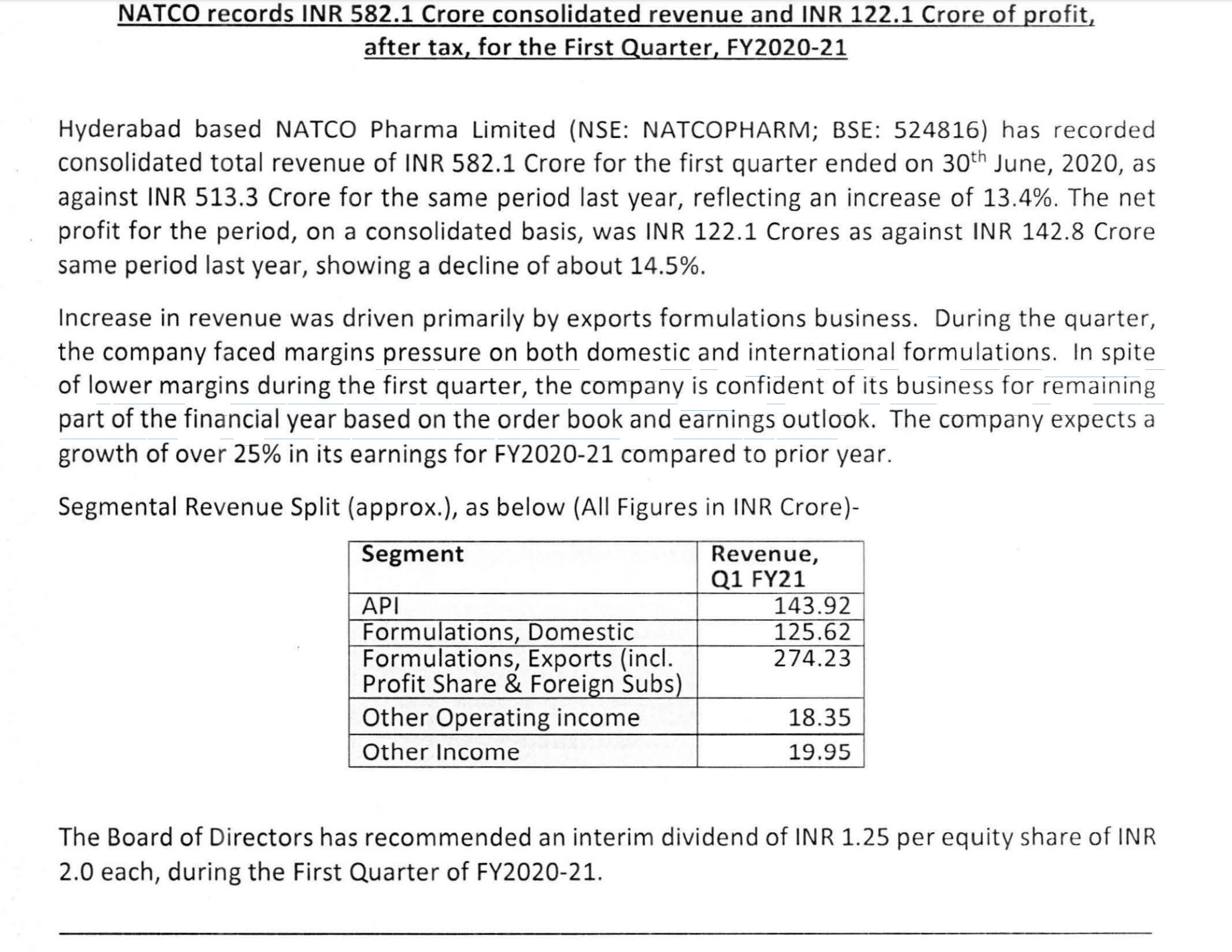

Natco’s result is actually quite reasonable aided by the export formulation business. Management has guided for a 20-25% growth in FY21 earnings, despite Q1 earnings being down by 14.5%. Market probably read this before the actual results came out. Lets see how it plays out.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b9bf9f58-c7b0-4d1d-907b-9b7ebf186090.pdf

Disclosure: Invested (position size here)