In this post, I will highlight commercial vehicle (CV) sector which is largely driven by credit and does well during economic expansion and gets butchered during economic contractions. I will illustrate it with a well known CV player Ashok Leyland. Here are the sales numbers, operating margins and net margins from 2004 (taken from tikr).

Strong growth was witnessed between 2003-2008, after which they witnessed growth contraction in FY09. Next phase of growth lasted until FY12, the downcycle then lasted for two years. The most recent phase of growth started in FY14 and ended in FY19. As auto is a business with huge operating leverage, margins expand during an upcycle and contract during a downcycle. For Ashok Leyland, in good times net margins can go upto 7% while in bad times net margins can also go negative.

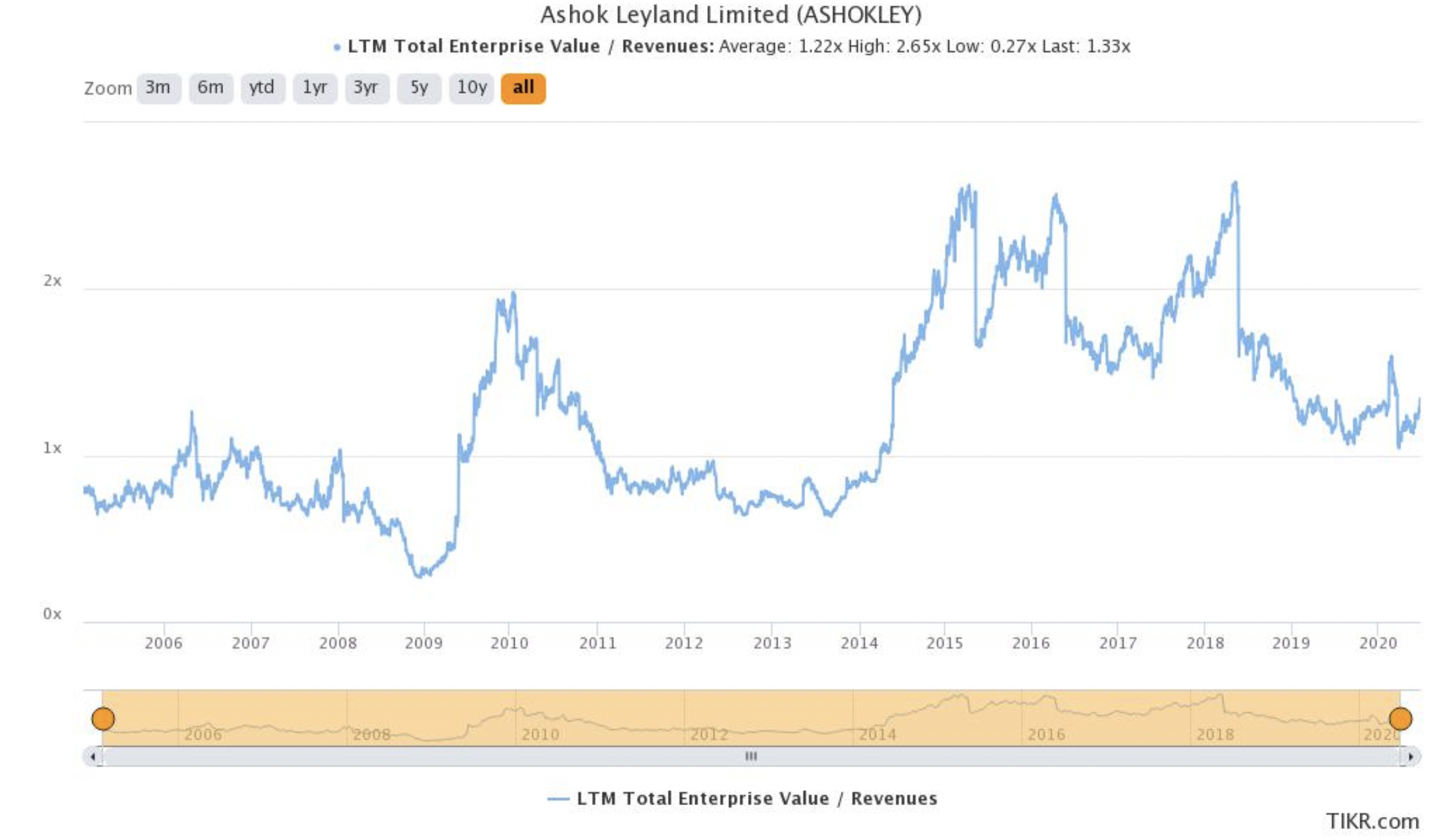

How does Mr. market value this company over time?

In good times, EV/sales can go upto 2x and comes down below 1x in bad times.

I am sharing some really basic stock price data to see how we can benefit from these cycles.

2003 lows ~ 5

2008 highs ~ 28 (5.6 times from previous low)

2008 lows ~ 6.15 (78% low from previous high)

2010 highs ~ 40 (6.5 times from previous low)

2013 lows ~ 11.75 (70% low from previous high)

2018 highs ~ 167.5 (14.3 times from previous low)

2020 lows ~ 33.7 (80% from previous highs)

Next highs ~ ???

Stock price goes up by >5x from cyclical lows and retraces 70-80% during the next downcycle. Its almost predictable! However, please note we are looking at past and future may turn out to be different.

The current downcycle started after ILFS episode (2018), we are currently 1.5 years in the downcycle. These can easily last 2-3 years. However, the long term growth of the CV sector reflects long term economic growth (i.e. GDP growth + inflation ~ 10-12%).

Key risks:

- Before ever investing in Ashok Leyland, everyone should read this post.

- Ashok Leyland grew at a faster pace in the past because it took market share away from Tata motors. Volvo eicher has been trying to take market share away from Tata and Ashok Leyland.

- Ashok Leyland has been trying to increase market share in light to medium segment which is less cyclical than medium and heavy segment where Ashok Leyland is market leader. However, the light to medium segment is much more competitive.

Disclosure: Invested (position size here)