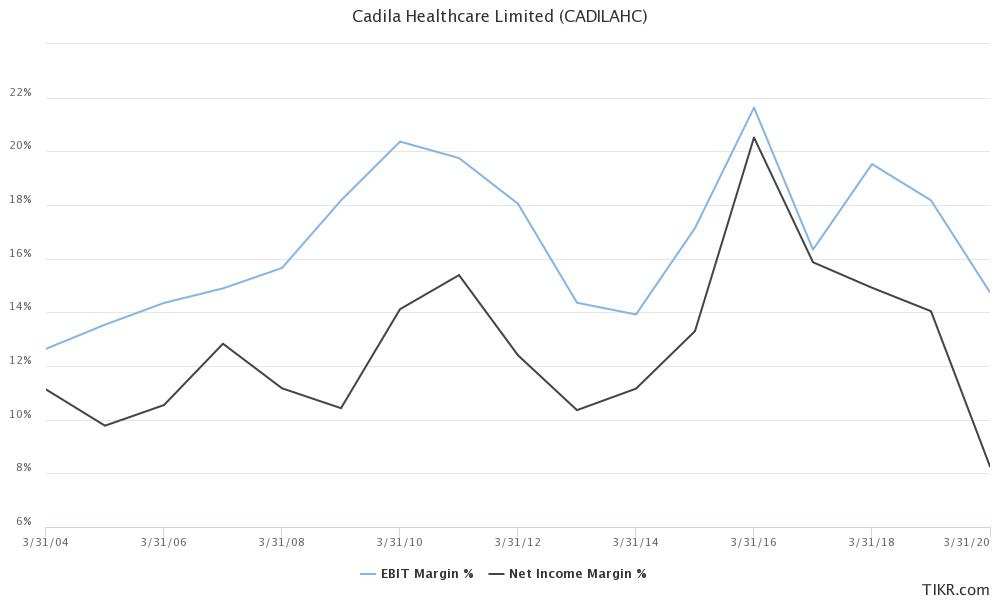

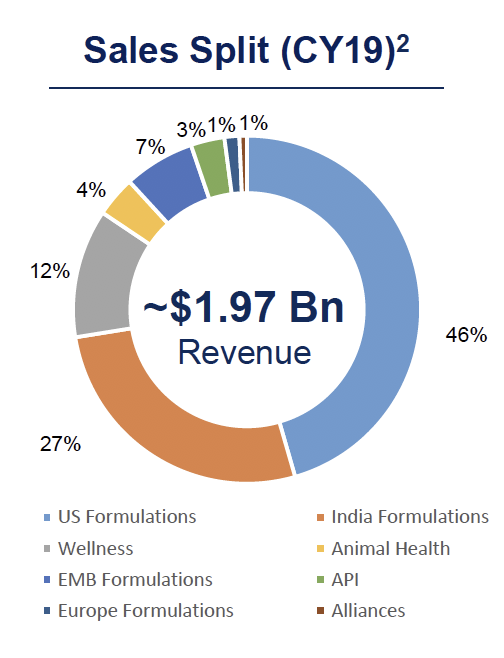

Cadila is one of India’s large pharma companies involved in selling formulations (generic, branded generics, specialty and biosimilars), APIs, and animal healthcare products. They also have a consumer wellness division which is separately listed (Zydus Wellness). The sales split is shown below. Most of the business comes from the US, followed by India.

US business

They have systematically grown their US generic business, improving their rank from 12th in FY11 to 4th in FY20. As of FY20, they have filed 390 ANDAs, out of these 282 have been approved and more than 175 products have been launched. Their US topline has grown from $212 mn in FY11 to $900 mn in FY19. They also have a large API division with 150 DMF filings as on date. They invest 7-8% of revenues into R&D, with 60% of R&D spent on the generic pipeline while 40% is spent on novel drugs and vaccines.

Their complex generics portfolio is focused on injectables while their specialty business in mostly focused on pain management. They plan to launch 45 injectables in the next 3 years, 30 of these are currently under development. The current contribution of injectables is ~$15 mn which the management expects should scale to $150-200 mn by FY24. Launches are planned from FY22 with meaningful revenues expected to flow in FY23. The company got into pain management through acquisition of Sentynl Therapeutics. It seems they overpaid for this because they later had to impair intangibles acquired through levorphanol which faced stiff competition from other generic launches.

India

This has been a consistent growth driver, growing from ~1200 cr. in FY09 to ~3700 cr. in FY20. Growth has been slower as their majority of Indian portfolio is acute. They recently regrouped their India business into Mass (55%) and Specialty (45%). Mass is akin to acute and speciality akin to chronic (that’s my interpretation). They seem to be now paying more attention on their domestic business, with a large restructuring which happened recently.

Consumer wellness

This division grew very fast from FY08 (~152 cr) to FY13 (~452 cr.). After this, growth slowed down significantly and reached 490 cr. in FY18. They then acquired certain products from Heinz (Glucon-D, Complan, Nycil, Sampriti Ghee). This portfolio had revenues of 1130 cr. and EBITDA of 225 cr. in TTM June 2018 and was acquired at 4595 cr. for which the promoter entity (Cadila) infused 1356 cr. at a share price of 1273.6. Current share price of Zydus is ~1690. The managment mentioned that Heinz acquisiton has gone better than expected. Adjusted for COVID and Heinz acquistion, base business growth was 10% in FY20.

Biosimilars, vaccine and new drugs business

Cadila started investing in their biosimilar portfolio before 2010, currently they have 21 biosimilars in their pipeline along with 6 novel products (new drugs). Their biosimilar strategy has been to focus on emerging markets and India, instead of US.

Cadila is one of the largest vaccine makers in India. They have initiated Phase I/II human trial for its own vaccine ZyCoV-D and also initiated clinical trials for COFEPRIS in Mexico.

Cadila’s investment into novel drugs have started paying dividends. Saroglitazar became world’s first drug to be approved by DCGI for treatment of Non Alcoholic Steato Hepatitis (NASH). It has successfully completed Phase II clinical trials in US. Saroglitazar Magnesium was also approved by DCGI in treatment of Type II Diabetes Mellitus as an add-on therapy with Metformin. They developed Exemptia (FY15Q3) which was the first ever biosimilar for adalimumab. They have developed Lipaglyn (FY14Q2), the first NCE discovered and developed by an Indian company. They had launched Zypitamag (Pitavastatin Magnesium tablets) through 505 (b) (2) route in FY18.

Animal healthcare

Cadila is the 2nd largest animal healthcare company (as per management). This division has grown from a topline of ~194 cr. in FY12 to ~515 cr. in FY20.

Their overall strategy can be summarized by the figure below

Key risks

- Management has systematically missed guidance. They had guided for $3bn revenues by FY15 which is still far away! They had earlier guided for 500 cr. topline in consumer business by 2013, however the number was 490 cr. in FY18. So, I will take their injectable revenue guidance of $150-200 mn by FY24 with a pinch of salt.

- Recently, their injectable facility in Moraiya got a warning letter from FDA. They have initiated site transfer of all injectable products from Moraiya to the injectable facility in Liva near Baroda. They have also launched the first site transfer injectable product from Liva. However, the warning letter needs to be lifted!

- They have been unable to penetrate the LATAM market (Mexico + Brazil), with revenues kind of stabilizing around 250 cr. since FY12.

- Their Indian performance is not great, mostly because of their large exposure to acute portfolio. Indian market share has been around 4.2-4.3% since FY14.

Disclosure: Invested (latest position size here)