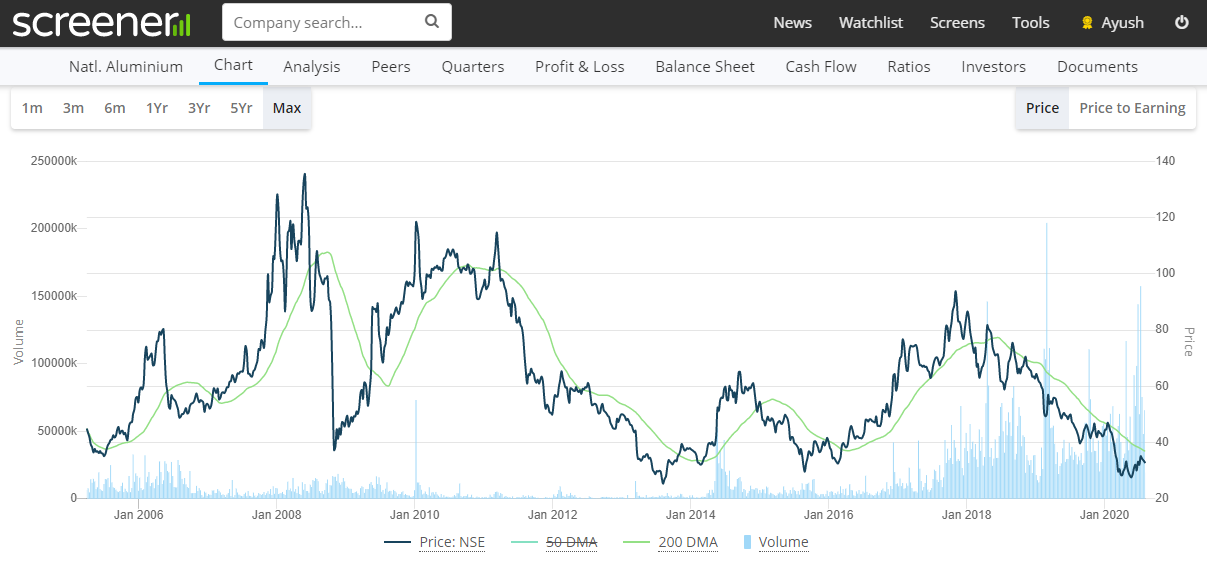

Very nice work @harsh.beria93 on the valuation framework for Nalco and multiple ways of looking at the company. I have been pursuing few companies in the commodity space as a basket and I feel that some of them are very attractive on valuations. Some of these cos seem to be at multiyear low and at substantial discount to replacement cost and BV. For a patient investor for next 2-3 year. For eg - in Nalco, like you mentioned, the stock is at multi-year low from multiple valuations perspectives - like Price to Sales, Price to BV, Div yield etc. From my side I did a very rudimentary analysis of the long term chart of the company and one can observe that the price is at kind of 15 year low despite the company being much bigger in size. The good thing with Nalco is that they are debt free and have a good dividend track record.

Interestingly the international aluminium prices have moved up to pre-covid levels and are up almost 20% from lows:

The recent performance of the company has been really poor in recent quarters as they had some issues in procurement of coal and power (biggest cost) in recent times but the same seems to have been resolved in recent months. They also got mining lease for a coal block recently which is expected to bring substantial saving in a couple of quarters- NALCO Gets Mining Lease For Utkal-D Coal Block

There have been articles about some major capex lined up and possibility of substantial cost savings.

There was a good detailed research report by B&K securities on the company recently. One may look for that to understand more.

Negatives - 1. PSU 2. Some of these are in-efficient - one can see the same as employee costs are very high 3. Company hasn’t grown much in terms of volumes over the years

Disc: Invested in family accounts and PMS.